Take-Two Interactive Software Inc (TTWO) Q4 Earnings Preview: What to Watch

Take-Two Interactive (TTWO) reports Q4 earnings on May 21. Investors are focused on fiscal 2027 guidance and the upcoming Grand Theft Auto VI launch cycle.

The setup

Take-Two enters this earnings cycle in a transition phase, balancing the maintenance of its live-service portfolio against the massive capital requirements of its next flagship release. Management has previously guided for net revenues between $1.57 billion and $1.62 billion for the quarter.

The primary investor focus is the initial fiscal 2027 net bookings guidance. A figure exceeding $9 billion is widely viewed as the threshold for market confidence in the Grand Theft Auto VI launch trajectory.

Analysts remain divided on the near-term execution risks versus long-term upside. Wells Fargo analyst Alec Brondolo maintains a constructive outlook with a $293 price target, while Morgan Stanley's Brian Nowak emphasizes the challenge of managing rising AAA development costs.

- Alicia Reese (Wedbush) maintains a $300 price target, citing long-term potential.

- Brian Nowak (Morgan Stanley) holds a $280 price target, focusing on live-service margins.

- Alec Brondolo (Wells Fargo) holds a $293 price target, highlighting the GTA VI catalyst.

- Macro headwinds include inflationary pressure on consumer discretionary spending.

- Rising development budgets for AAA titles continue to pressure operating margins.

Consensus numbers

Consensus estimates reflect a period of moderated growth as the company manages its development pipeline. The market is pricing in a challenging year-over-year comparison for the quarter ending March 31, 2026.

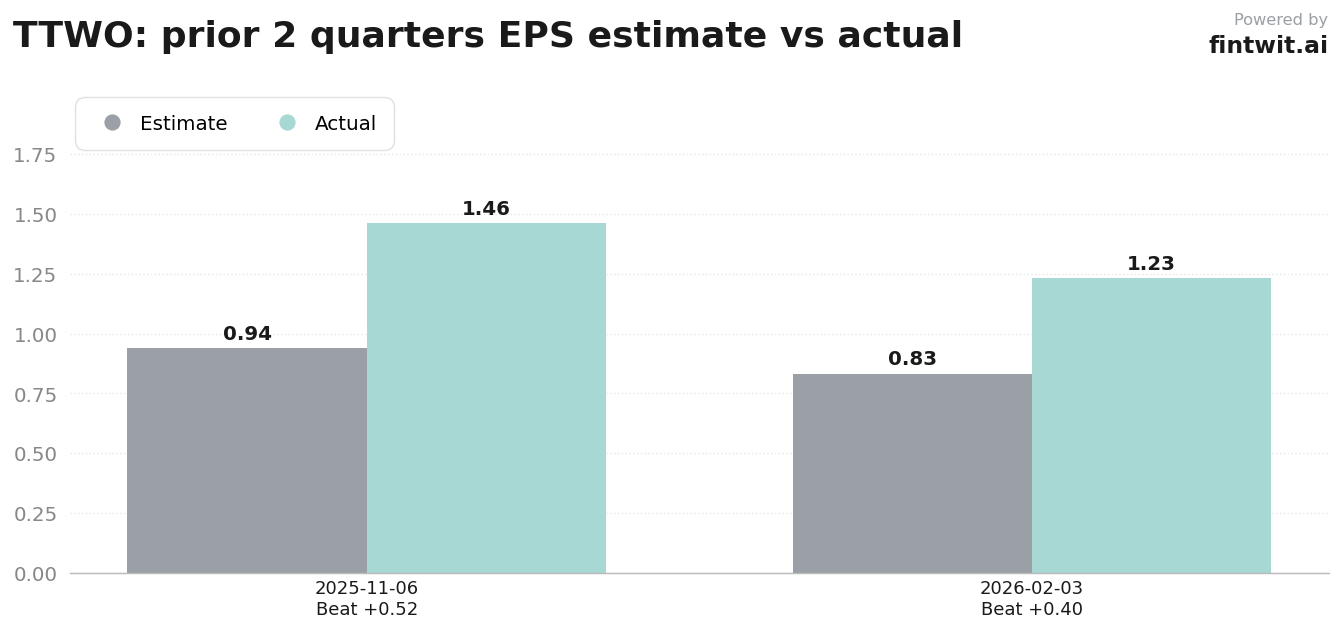

Historical performance shows a tendency for the company to outperform conservative EPS estimates. Investors will compare the reported figures against the following consensus benchmarks.

- EPS Estimate: $0.58

- Revenue Estimate: $1.547 billion

- Beat Probability: 45% chance of an earnings beat

- Miss Probability: 35% chance of an earnings miss

- Inline Probability: 20% chance of meeting expectations

- NBA 2K Franchise: Targeting high-20% growth in recurrent consumer spending

What we'll watch on the call

Management's commentary on the Grand Theft Auto VI development timeline will be the most scrutinized aspect of the call. Any deviation from the November 19, 2026, release date would likely trigger significant volatility.

The health of the live-service ecosystem remains a critical indicator of cash flow stability. Analysts are looking for evidence that the company can sustain engagement across its mobile and console segments while ramping up marketing spend.

- Initial net bookings guidance for fiscal 2027.

- Impact of AAA development cost inflation on operating margins.

- Technical risk assessment for the GTA VI launch cycle.

- Sustainability of mobile revenue from titles like Toon Blast and Match Factory!.

- Performance of GTA Online as a bridge to the next franchise iteration.

- Marketing spend efficiency relative to upcoming title releases.

Fintwit's AI verdict

The quantitative model suggests that the current valuation reflects a significant discount relative to the potential revenue surge expected in late 2026. While near-term margin compression is a known risk, the market appears to be underestimating the long-tail monetization potential of the upcoming release cycle.

Sentiment analysis indicates that institutional positioning is shifting toward a more aggressive stance as the release date approaches. The combination of strong historical earnings surprises and the massive addressable market for the next GTA installment creates a compelling risk-reward profile for long-term holders.