Ross Stores Inc (ROST) Q1 2026 Earnings Preview: What to Watch

Ross Stores reports Q1 2026 earnings on May 21. Analysts watch comparable store sales and margin resilience amid tariff risks and consumer spending shifts.

The setup

Ross Stores enters the Q1 2026 print with strong momentum following a series of positive analyst revisions. The company's off-price model continues to attract value-conscious consumers facing elevated costs for everyday goods and gasoline.

Management has set expectations for comparable store sales growth of 7% to 8% for the quarter. This guidance serves as the primary benchmark for the company's ability to sustain its current traffic and transaction volume.

- Deutsche Bank analyst Krisztina Katai maintains a Buy rating with a $253 price target, citing improved merchandising.

- UBS holds a Neutral rating with a $227 price target, noting potential for a 9-cent EPS beat.

- Wells Fargo raised its price target to $235, highlighting high confidence in the company's growth trajectory.

- Macro headwinds include potential tariff-related costs on apparel sourcing from Asia and ongoing labor cost pressures.

Consensus numbers

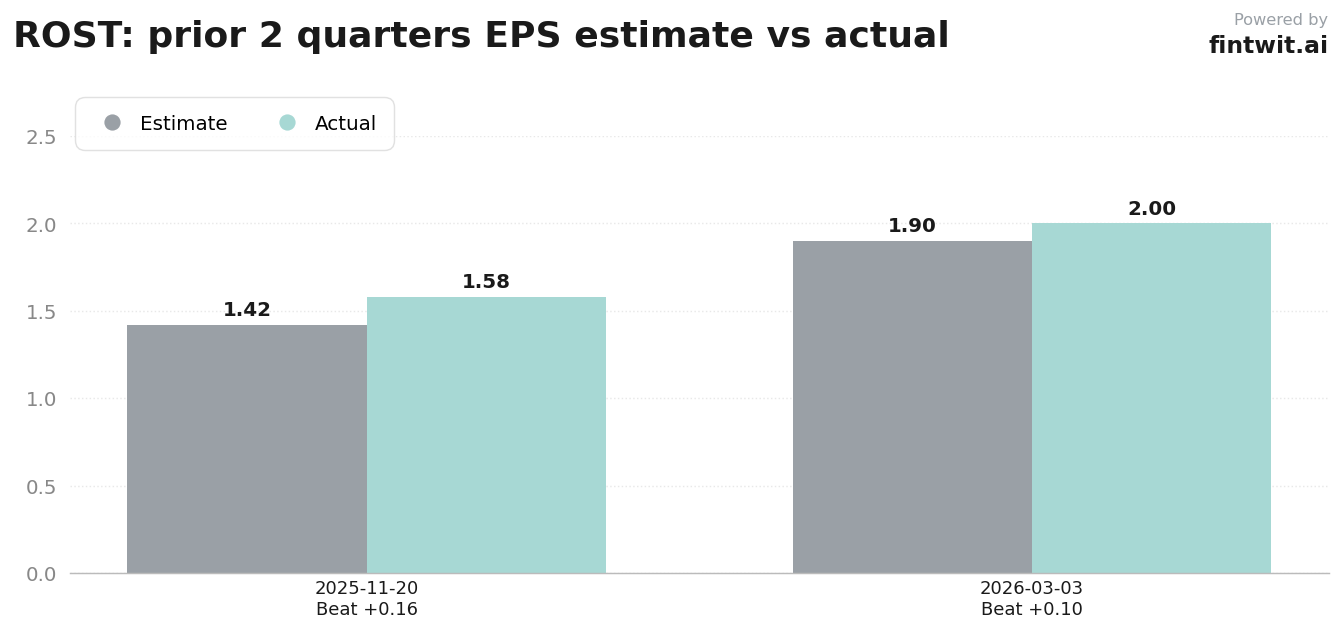

Wall Street consensus estimates for the quarter reflect solid year-over-year growth expectations. The company has a history of outperforming these estimates, as seen in the previous two quarterly reports.

Investors are looking for EPS to land in the $1.60 to $1.67 range, with a consensus estimate of $1.71 for the broader period. Revenue estimates currently sit at approximately $5.61 billion.

- EPS Estimate: $1.71

- Revenue Estimate: $5.61 billion

- Comparable Store Sales Guidance: 7% to 8% growth

- Full Fiscal Year 2026 EPS Guidance: $7.02 to $7.36

- Beat Probability: 65% beat, 15% miss, 20% inline

What we'll watch on the call

Management's commentary on operating margins will be the most critical line item for institutional investors. The company has guided for margins between 11.8% and 12.1%, but analysts are questioning if distribution costs and tariff impacts will force a revision.

Inventory management remains a focal point as the company navigates lower packaway levels compared to the prior year. This strategy affects the retailer's flexibility to chase in-season trends and maintain fresh assortments.

- Impact of potential trade policy changes on merchandise margins and pricing strategies.

- Sustainability of current transaction-driven traffic growth throughout the remainder of the fiscal year.

- Outlook for dd's DISCOUNTS expansion and its role in capturing price-sensitive consumer segments.

- Sensitivity to minimum wage increases across the company's large store footprint.

Fintwit's AI verdict

The quantitative model suggests that the current market pricing does not fully account for the resilience of the off-price retail sector. While macro risks regarding tariffs are present, the company's historical ability to manage inventory and capture market share from traditional department stores remains a significant tailwind.

Investors should monitor the post-earnings reaction relative to the $235 price target set by Wells Fargo. The combination of strong traffic data and disciplined cost management suggests a favorable outlook for the coming quarter.