Should You Buy ZS Right Now? Analyzing the Zscaler Stock Sell-Off

Zscaler stock dropped 31.52% after a guidance cut. We break down the bull and bear cases for investors weighing a position in the cybersecurity leader.

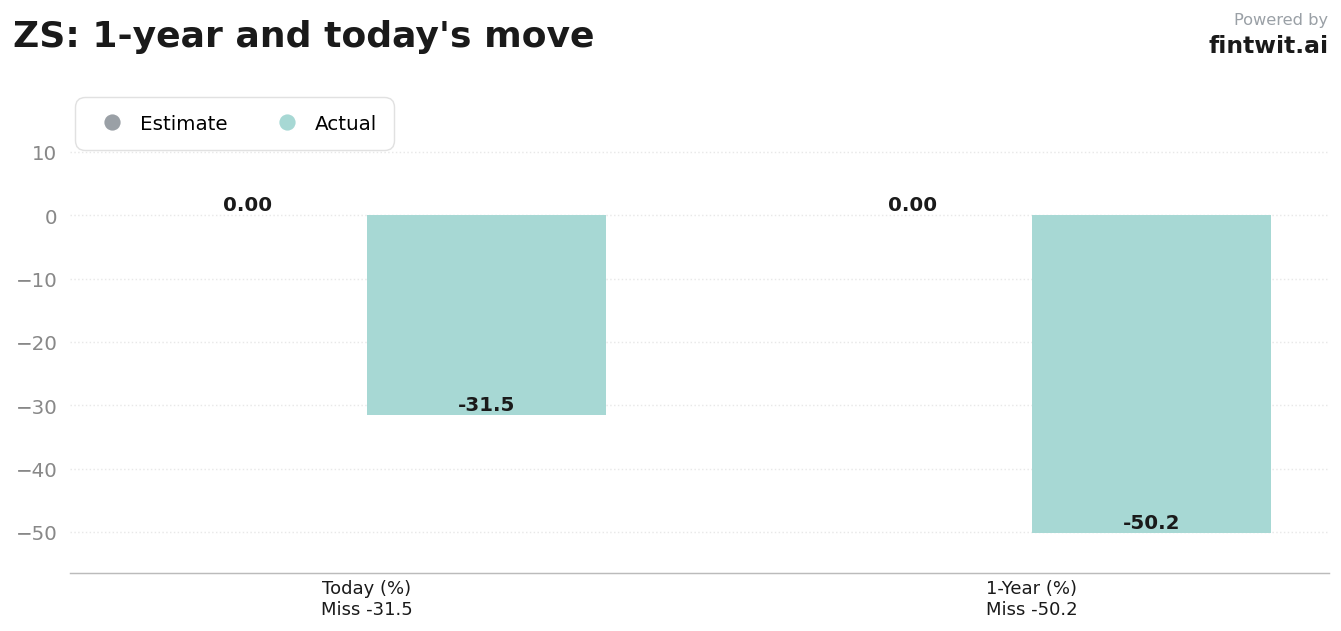

What just happened

The sharp sell-off was triggered by management lowering its fiscal 2026 free cash flow margin guidance to a range of 22.8% to 23.3%, down from the previous 26.5% to 27% target. This margin compression is driven by increased capital expenditures as the company scales its infrastructure.

Investors also reacted poorly to a cautious preliminary fiscal 2027 revenue growth outlook of 16% to 17%. The departure of two senior sales leaders added further uncertainty to the company's near-term execution capabilities.

Despite these headwinds, Zscaler reported record operating margins and strong demand for its AI-security products in the third quarter of fiscal 2026. The market is currently prioritizing the deceleration of growth expectations over these operational successes.

Bull case

- Jonathan Ruykhaver of Cantor Fitzgerald maintains a Buy rating with a $300 price target, suggesting a potential 136.2% upside.

- The Z-Flex program is successfully driving longer-term customer commitments and improving revenue visibility for the platform.

- Zscaler continues to see strong demand for its AI-security product suite, which remains a core differentiator in the infrastructure software space.

- The company achieved record operating margins in the most recent quarter, demonstrating underlying profitability despite the current capital-intensive phase.

Bear case

- Meta Marshall of Morgan Stanley holds a Hold rating with a $145 target, noting the stock will remain in a penalty box until there is evidence of traction with SecOps products.

- Gabriela Borges of Goldman Sachs maintains a Neutral rating with a $179 target, citing business maturity and a slowing SASE cycle.

- Elevated capital expenditures are expected to continue pressuring free cash flow margins through fiscal 2026.

- The departure of two senior sales leaders creates execution risk within the enterprise sales organization.

Fintwit's AI verdict

The quantitative models are currently processing the divergence between the company's fundamental growth metrics and the recent market-driven valuation reset. While the technical indicators show significant downward momentum, the underlying platform demand suggests a potential disconnect between price and long-term value.

Investors are weighing whether the current price level accounts for the leadership transition and the margin compression or if further downside is required to reach a bottom. The model output suggests a specific stance based on the current risk-reward profile of the security infrastructure sector.