Should You Buy DY Right Now? Dycom Industries (DY) Analysis

Dycom Industries (DY) shares jumped 25.84% after a massive earnings beat. Is the stock a buy at current levels?

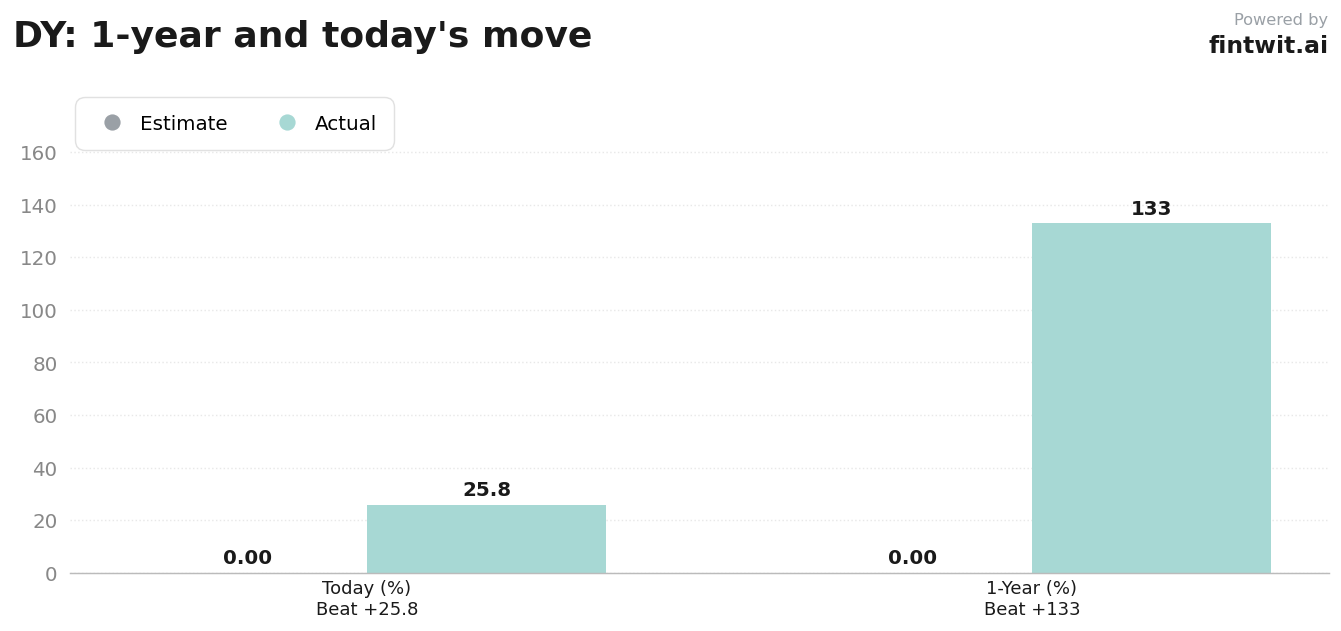

What just happened

The stock price hit $529.13 following the release of the quarterly report. This move extends a massive rally that has seen the shares return 132.85% over the past twelve months.

Management raised its full-year outlook, citing a record backlog of $11.9 billion. This backlog provides significant visibility into future revenue streams as the company scales its digital infrastructure operations.

Bull case

- Joseph Osha of Guggenheim maintains a Buy rating with a $510.00 price target, citing Dycom's critical role in digital infrastructure.

- Liam Burke of B. Riley Securities holds a Buy rating and a $485.00 target, emphasizing the company's multi-year growth trajectory.

- The federal BEAD program is expected to provide substantial tailwinds as funding flows into broadband deployment projects.

- Hyperscale data center demand remains a primary driver for long-term revenue growth through 2028.

- The integration of National Technology Integrators expands Dycom's capabilities in the high-growth data center market.

Bear case

- Richard Choe of JP Morgan maintains a Buy rating but notes valuation concerns, with the stock trading at a P/E of approximately 35.22x.

- The current P/E ratio sits at a significant premium compared to historical averages for the engineering and construction sector.

- Dycom does not pay a dividend, as the company prioritizes capital reinvestment and strategic acquisitions over shareholder payouts.

- Execution risk remains high as the company attempts to manage its record $11.9 billion backlog in a tight labor market.

- Market volatility could compress valuation multiples if infrastructure spending growth slows from current elevated levels.

Fintwit's AI verdict

The quantitative model evaluates Dycom based on its recent earnings momentum, backlog growth, and sector-specific tailwinds. While valuation metrics suggest the stock is priced for perfection, the underlying fundamentals remain strong.

Investors must weigh the high growth potential against the current premium valuation. The model output provides a specific outlook based on these variables.