Is The Allstate Corporation (ALL) Undervalued? A Valuation Analysis

Allstate (ALL) trades at a 5.40 P/E ratio, significantly below industry peers. We analyze the underwriting margins, AI initiatives, and potential upside.

The headline number

Allstate currently commands a market capitalization of $53.37 billion. The stock's P/E ratio of 5.40 stands in stark contrast to the broader financial services sector.

Analysts at Alpha Spread estimate a fair value of $399.82, while Simply Wall St provides a more aggressive estimate of $649.33. Sahm Capital offers a more conservative fair value target of $236.00.

The company reported Q1 2026 adjusted EPS of $10.65, demonstrating a recovery in earnings power. This performance highlights the potential for sustained high return on equity.

- Current Price: $208.85

- P/E Ratio: 5.40

- Dividend Yield: 1.96%

- Alpha Spread Fair Value: $399.82

- Simply Wall St Fair Value: $649.33

- Sahm Capital Fair Value: $236.00

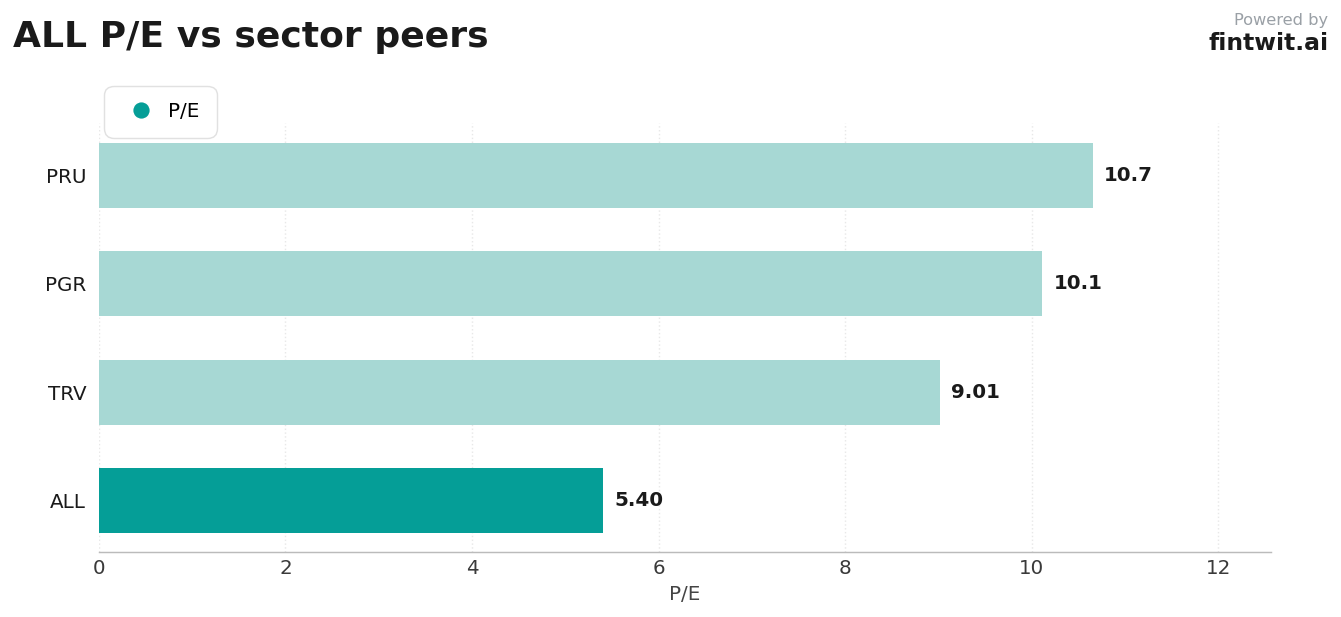

Peer comparison

Allstate's valuation multiple is compressed compared to its primary competitors in the property and casualty insurance space. This discount persists despite the company's aggressive integration of the ALLIE AI ecosystem.

The following data illustrates the valuation gap between Allstate and its peers. Investors should note the premium multiples assigned to companies with similar business models.

- Progressive (PGR): 10.11 P/E ratio; reflects premium growth and underwriting consistency.

- Travelers (TRV): 9.01 P/E ratio; trades at a significant premium to Allstate.

- Prudential (PRU): 10.65 P/E ratio; reflects the broader diversified financial services baseline.

Bull vs bear

The bull case for Allstate rests on the successful deployment of proprietary technology to improve actuarial accuracy. Conversely, the bear case focuses on external volatility factors that remain outside of management's direct control.

Investors must weigh the potential for margin expansion against the inherent risks of the property and casualty insurance industry.

- Bull: Structural improvement in underwriting margins via the ALLIE AI ecosystem, compressing actuarial latency.

- Bull: Strong policy-in-force growth in core auto and homeowners segments, supported by effective marketing.

- Bull: Significant earnings power recovery with Q1 2026 adjusted EPS of $10.65.

- Bear: High catastrophe exposure in homeowners insurance remains a persistent volatility risk.

- Bear: Regulatory constraints in states like California and New York limit necessary rate hikes.

- Bear: Potential float dilution from shifting toward price-sensitive, lower-retention customer segments.

Fintwit's AI verdict

The quantitative analysis suggests that the current market price fails to account for the efficiency gains derived from the company's recent digital transformation. The valuation gap relative to peers like Progressive and Travelers appears to be a result of market overreaction to catastrophe risk rather than fundamental operational failure.

Management's focus on personal property-liability market share, combined with a disciplined capital return program, provides a floor for the stock price. The current entry point offers a favorable risk-reward profile for long-term investors seeking exposure to the insurance sector.