Should You Buy TSEM Right Now? Tower Semiconductor Analysis

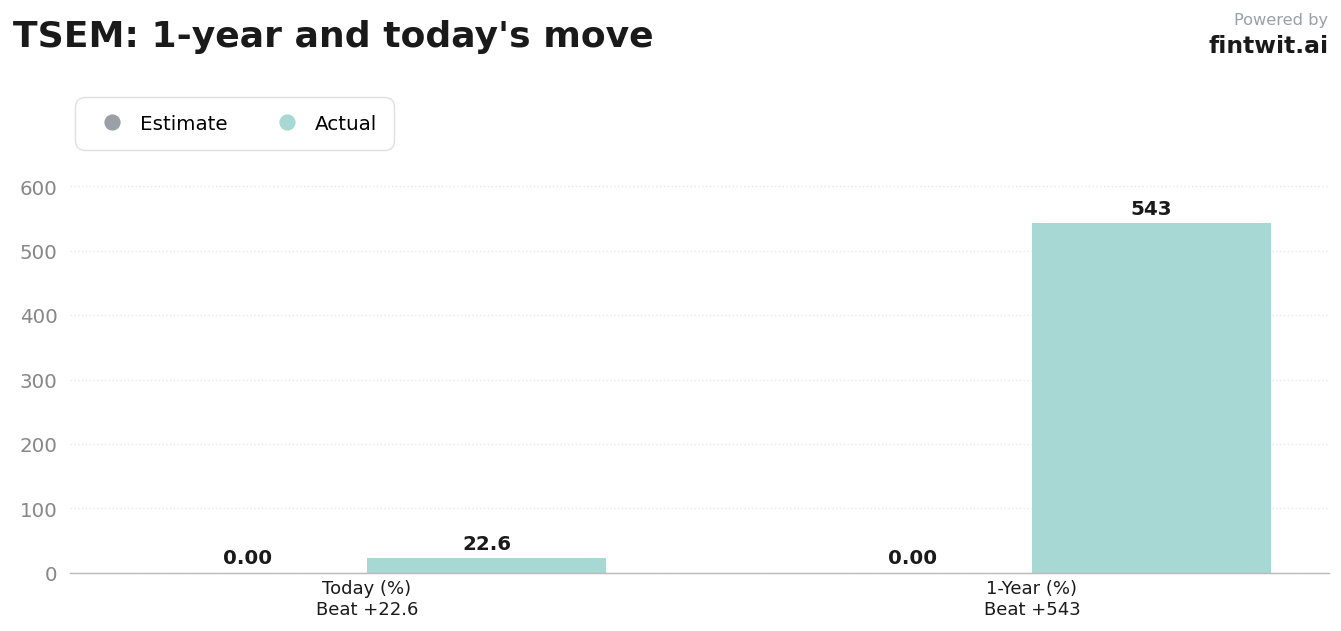

Tower Semiconductor (TSEM) shares jumped 22.61% on strong Q1 earnings. Is the rally sustainable or is the stock priced for perfection?

What just happened

The rally follows a record-breaking Q2 revenue guidance of $455 million. Management also announced $1.3 billion in contracted silicon photonics revenue scheduled for 2027.

TSEM has rallied from $199 in late April to current levels above $270. This momentum is driven by a combination of AI infrastructure demand and defense radar production wins.

Bull case

- Benchmark raised its price target to $230 from $165, citing a 2028 financial model targeting $2.84 billion in revenue.

- The company projects a 50.5% net profit CAGR through 2028.

- Silicon photonics demand is accelerating, with $1.3 billion in long-term contracts already secured for 2027.

- Capacity expansion plans include a $920 million CapEx investment for SiGe and SiPho manufacturing throughout 2026.

- Restructuring of the Fab 7 facility is expected to scale 300mm manufacturing capacity in Japan.

Bear case

- The stock currently trades at a P/E ratio of 84.78, suggesting it is priced for perfection.

- Wedbush maintains a Neutral rating with a $140 price target, significantly below the current market price.

- Barclays holds a Neutral rating and a $142 target, reflecting a cautious consensus among analysts.

- Current market price of $270.77 sits well above the average analyst price target, indicating potential overvaluation.

- Management is prioritizing aggressive capital reinvestment over dividend distributions, offering no yield to shareholders.

Fintwit's AI verdict

The quantitative model evaluates TSEM based on its recent earnings surprise and the strength of its long-term contract backlog. While the valuation metrics appear stretched relative to historical averages, the growth trajectory in the silicon photonics segment provides a unique tailwind.

Investors must weigh the high P/E ratio against the company's ability to execute its $920 million capacity expansion plan. The following verdict reflects the model's assessment of the current risk-reward profile.