Is Renaissancere Holdings Ltd (RNR) Undervalued? A Valuation Analysis

Renaissancere Holdings Ltd (RNR) trades at a 5.19x P/E ratio. We analyze the reinsurance giant's valuation, peer comparisons, and the bull versus bear case.

The headline number

Renaissancere Holdings Ltd (RNR) currently trades at $290.01 per share. Its valuation metrics suggest a significant discount compared to broader financial sector averages.

The current P/E ratio of 5.19x is notably low for a company with its market position in the reinsurance industry. This valuation gap persists despite the firm's consistent capital return strategy.

- Market Capitalization: $12.66 billion.

- Dividend Yield: 0.0055 (0.55%).

- 180-Day Price Performance: +10.03%.

- Cantor Fitzgerald Fair Value Estimate: $282.

- Wells Fargo Fair Value Estimate: $281.

- Simply Wall St Fair Value Estimate: $326.47 - $329.60.

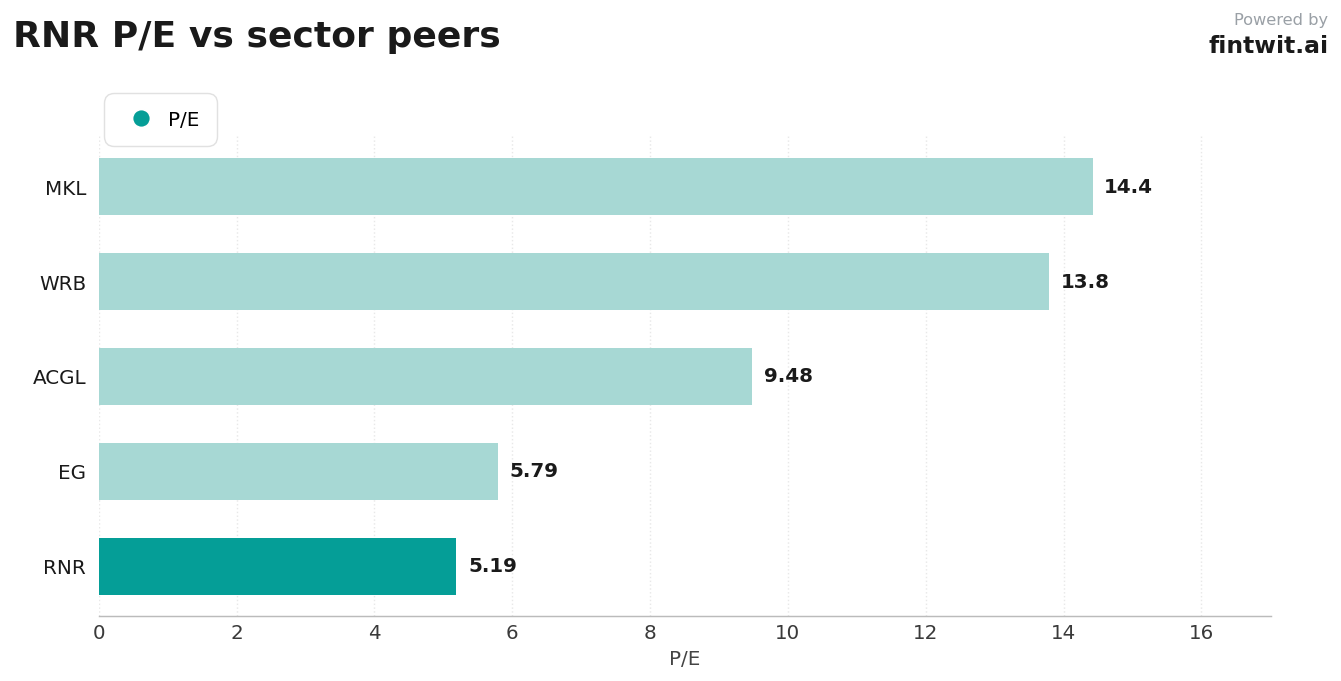

Peer comparison

Comparing RNR to its direct competitors reveals a valuation discrepancy that warrants further investigation. While peers trade at higher multiples, RNR maintains a lower entry point relative to its earnings power.

The following data highlights the P/E ratio divergence between RNR and its industry peers.

- RNR: 5.19x P/E ratio.

- Everest Group (EG): 5.79x P/E ratio; direct reinsurance peer with similar cyclical exposure.

- Arch Capital (ACGL): 9.48x P/E ratio; diversified specialty insurer/reinsurer.

- W.R. Berkley (WRB): 13.79x P/E ratio; higher multiple reflects broader specialty insurance focus.

- Markel Group (MKL): 14.42x P/E ratio; diversified financial holding company.

Bull vs bear

The investment thesis for RNR hinges on the balance between underwriting discipline and the inherent volatility of the reinsurance market. Investors must weigh the potential for capital returns against the risk of catastrophic loss events.

Bull and bear arguments provide a framework for assessing the company's long-term viability.

- Bull Case: Strong underwriting discipline and proprietary risk modeling allow for superior margin retention despite industry-wide rate pressure.

- Bull Case: Aggressive capital management, including retiring >5% of shares in recent periods, enhances EPS growth.

- Bull Case: Growing fee income from Capital Partners provides a stable, non-volatile revenue stream.

- Bear Case: Projected annual revenue decline of 6-11% over the next three years due to softening reinsurance pricing cycles.

- Bear Case: High sensitivity to U.S. catastrophe events like hurricanes and wildfires can lead to significant earnings volatility.

- Bear Case: Increased competition from alternative capital sources may cause margin compression in casualty and specialty segments.

Fintwit's AI verdict

The quantitative assessment of RNR suggests that the current market pricing does not fully capture the firm's operational efficiency or its ability to generate fee-based income. While the reinsurance cycle presents headwinds, the company's aggressive share buyback program and disciplined risk management provide a buffer for shareholders.

Market participants are closely monitoring the firm's ability to maintain its expense ratio targets of 5%-5.5% through 2026. The combination of valuation support and capital return initiatives positions the stock favorably for those with a long-term horizon.