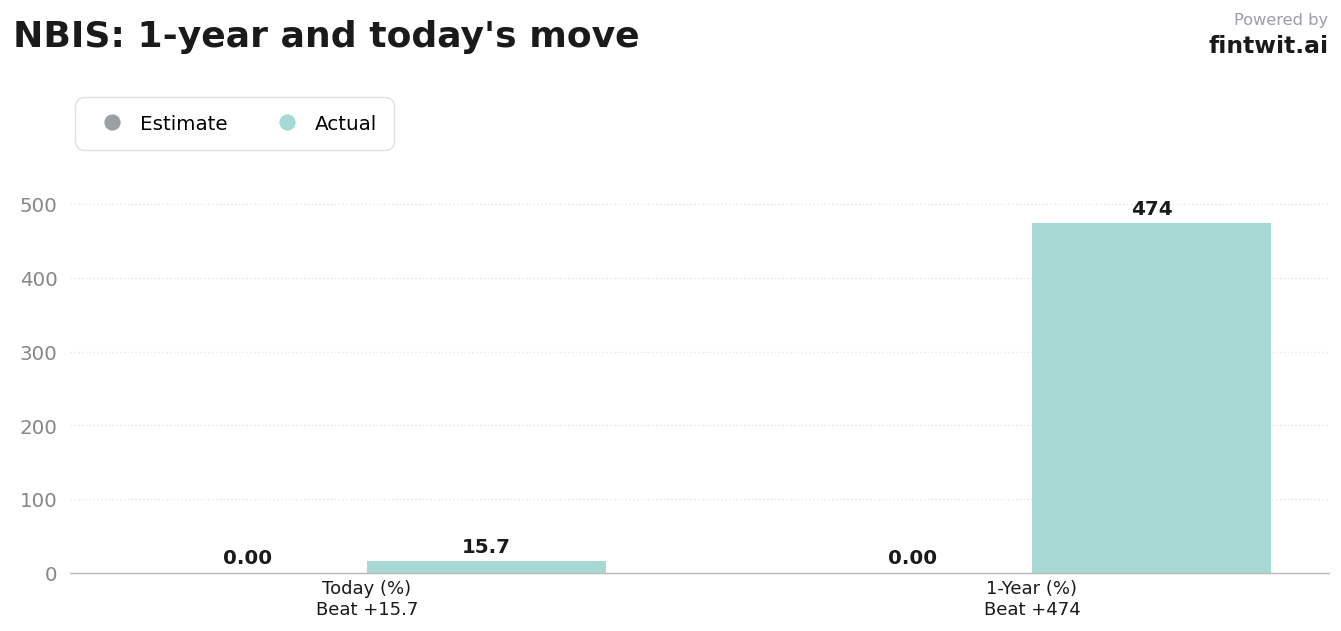

Should You Buy Nebius Group (NBIS) After the 15.72% Surge?

Nebius Group (NBIS) shares surged 15.72% following a blowout Q1 2026 earnings report. Is the AI infrastructure play still a buy at these levels?

What just happened

Nebius Group reported $399 million in revenue for the first quarter of 2026, representing a 684% increase year-over-year. The company achieved a surprise swing to positive adjusted EBITDA of $129.5 million, signaling that its massive capital expenditure in GPU clusters is beginning to yield operating leverage.

Management announced a major expansion plan to secure 1.2 GW of power and land for a new AI factory in Pennsylvania. This infrastructure build-out is designed to support the company's multi-billion dollar backlog with hyperscalers like Meta and Microsoft.

Bull case

- Annual recurring revenue (ARR) reached $1.92 billion, keeping the company on track for its $7-9 billion year-end target.

- DA Davidson raised its price target to $250.00, citing strong Q1 earnings and continued demand signals across customer demographics.

- Goldman Sachs reiterated a Buy rating, highlighting strong revenue growth driven by capacity scaling, pricing, and utilization.

- The company is successfully transitioning from a heavy investment phase to generating positive adjusted EBITDA.

- The 1.2 GW Pennsylvania expansion provides a clear runway for long-term capacity growth to meet hyperscaler demand.

Bear case

- The stock trades at a high valuation multiple of approximately 16x forward revenue, leaving little room for execution errors.

- Wolfe Research initiated coverage at Peerperform with a fair value range of $80 to $170, citing significant financing and execution risks.

- The company's P/E ratio stands at 980.17, indicating that the current share price is heavily dependent on future growth expectations.

- Heavy capital expenditure requirements for GPU clusters and data centers mean no dividend payments are expected in the near term.

- The reliance on a small number of major hyperscalers for the majority of the revenue backlog creates concentration risk.

Fintwit's AI verdict

The market is currently pricing Nebius for perfection, reflecting the extreme growth momentum seen in the latest quarterly results. Investors must weigh the rapid revenue scaling against the significant capital intensity required to maintain this trajectory.

Our proprietary sentiment analysis and quantitative model have processed the recent earnings beat and analyst revisions to determine if the current valuation remains justified. The data suggests a specific outlook for the coming quarters.