Should You Buy ROKU Right Now? Analyzing the 20% Surge

Roku shares jumped 20% on M&A rumors. We break down the bull and bear cases for the streaming platform and look at the path ahead for investors.

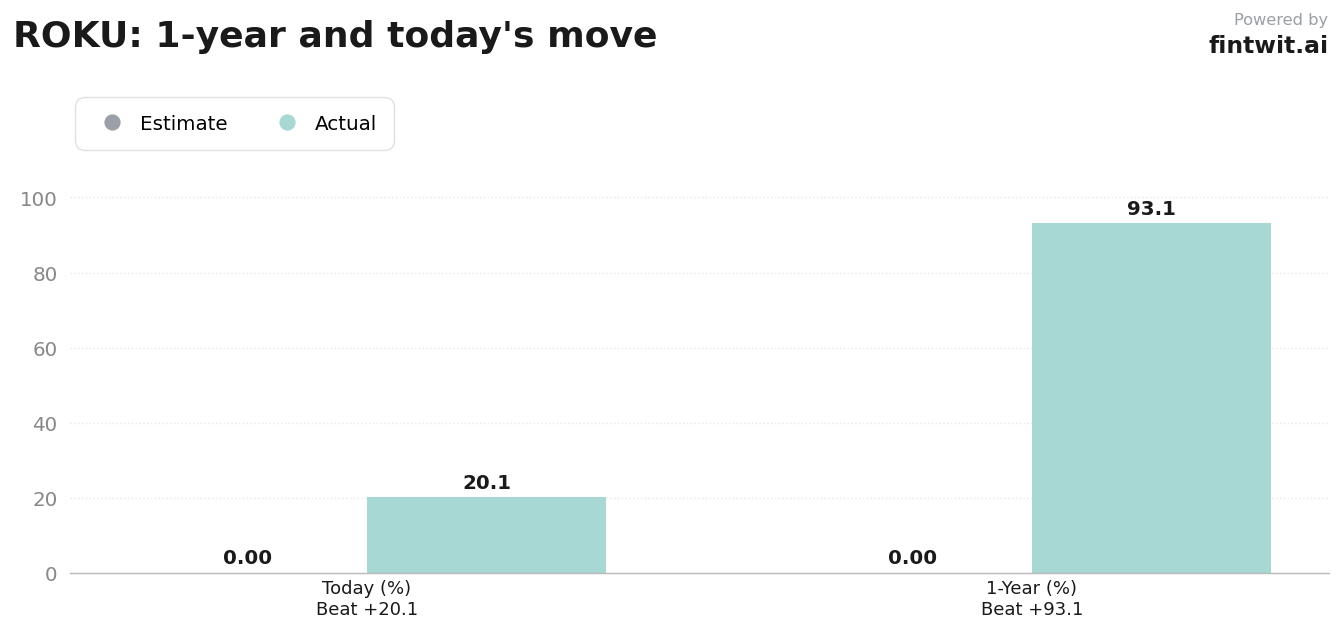

What just happened

Roku shares closed at $143.66 following the news of potential acquisition talks. The market reaction reflects high sensitivity to consolidation rumors within the streaming sector.

The company reported a strong Q1 2026 earnings beat, with revenue growing 22% year-over-year to $1.2 billion. Advertising revenue specifically drove this growth, climbing 27% during the same period.

Bull case

- Morgan Stanley analyst Thomas Yeh maintains an Overweight rating with a $170 price target, citing improved monetization from a more personalized home screen.

- Guggenheim analyst Michael Morris holds a Buy rating and a $145 target, noting that Wall Street underestimates platform revenue potential beyond 2026.

- The company is set to join the S&P MidCap 400 index effective June 22, 2026, which typically triggers institutional buying.

- Platform revenue remains a high-margin growth engine with a clear path toward $1 billion in annual free cash flow.

Bear case

- The stock currently trades at a P/E ratio of 158.08, representing a significant valuation premium compared to legacy media peers.

- Citigroup maintains a Neutral stance, highlighting the difficulty in balancing strong operational fundamentals against high valuation sensitivity.

- The company does not pay a dividend, meaning investors are entirely dependent on capital appreciation for returns.

- Future growth is contingent on ad-tech scaling and successful integration of new platform initiatives, which face intense competition from larger tech incumbents.

Fintwit's AI verdict

The algorithmic assessment of Roku's current market position weighs the recent 20% price spike against the underlying fundamental growth in ad-tech and platform engagement. While the valuation remains elevated, the potential for M&A activity creates a unique risk-reward profile that differs from traditional growth models.

Our proprietary model evaluates the confluence of institutional analyst sentiment and the upcoming index inclusion to determine the probability of further upside. The data suggests that the current momentum may be supported by more than just speculative acquisition rumors.