Should You Buy ASTS Right Now? Analyzing the SpaceMobile Sell-off

ASTS shares fell 15.53% today. We break down the technicals, analyst sentiment, and the core arguments for and against buying the dip.

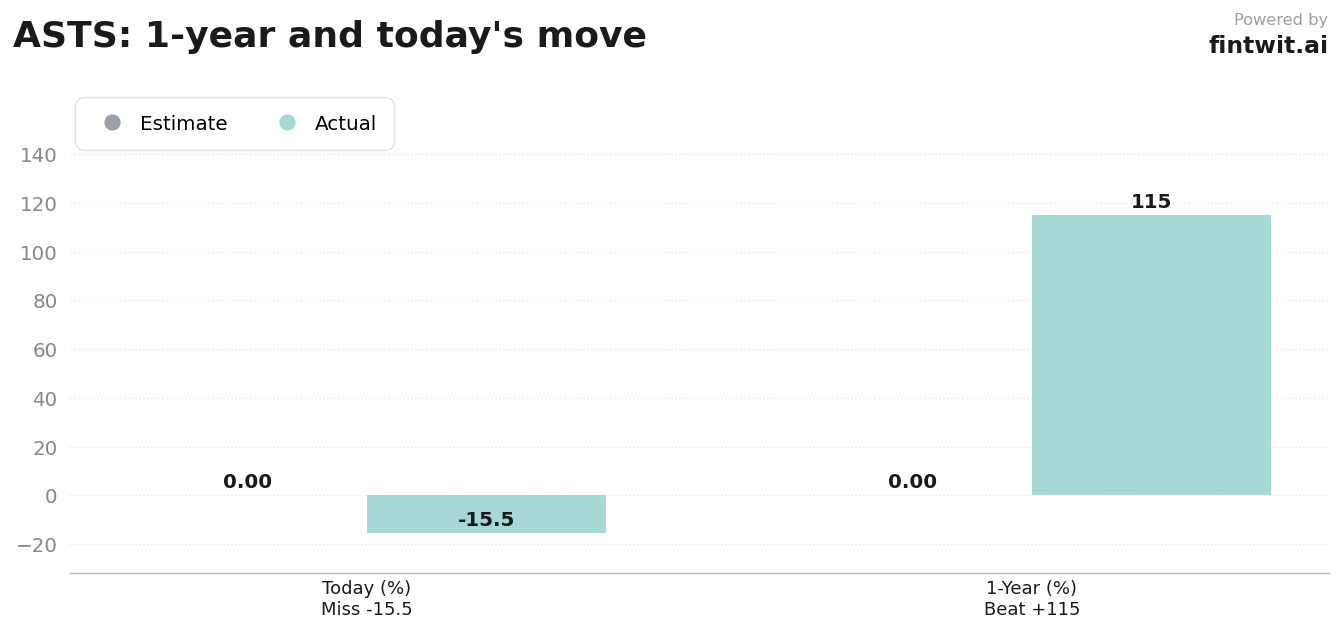

What just happened

The sharp decline in ASTS reflects a combination of profit-taking and sector-wide capital rotation. Investors are weighing the company's transition from a conceptual phase to a commercial execution phase.

Technical indicators suggest high volatility. The MACD histogram turned negative on June 5, 2026, and the momentum indicator has dipped below the zero level, signaling potential short-term downward pressure.

Bull case

- The company is targeting a production capacity of six fully assembled satellites per month to scale its constellation.

- Revenue guidance for 2026 is set between $150 million and $200 million, contingent on commercial and government milestones.

- Expansion of commercial service agreements with global mobile network operators provides a pathway to monetize the direct-to-device network.

- The stock has delivered a 114.78% return over the past 12 months, demonstrating strong historical growth potential.

Bear case

- Deutsche Bank analyst Bryan Kraft downgraded the stock to Hold with a $106 target, citing the difficult transition from concept to execution.

- Barclays analyst Mathieu Robilliard maintains an Underweight rating with a $65 target due to capital-intensive buildout concerns and potential launch delays.

- UBS analyst Christopher Schoell holds a Neutral rating with an $80 target, adopting a wait-and-see approach regarding constellation scaling.

- The company is currently pre-profit with significant cash burn, making it unsuitable for value or income-focused investors.

Fintwit's AI verdict

The algorithmic assessment of ASTS balances the aggressive growth narrative against the reality of its current cash burn and technical volatility. While the market is currently digesting a significant correction, the underlying infrastructure milestones remain the primary variable for future valuation.

Our proprietary model evaluates the risk-adjusted potential of the company's direct-to-device technology against the current analyst consensus. The resulting outlook suggests that the current price levels may present a specific opportunity for those comfortable with high-beta assets.