Should You Buy Planet Labs (PL) After the 26% Sell-Off?

Planet Labs shares fell 26% on margin concerns despite record revenue. Is the dip a buying opportunity or a warning sign for investors?

What just happened

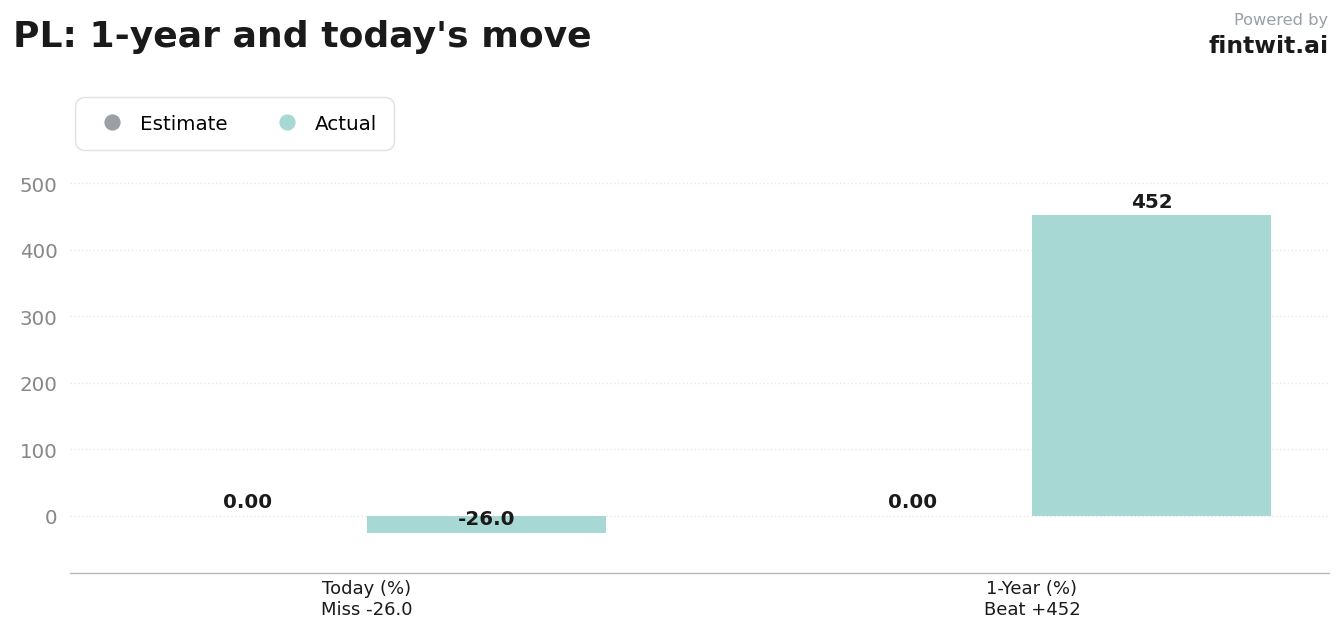

The market reacted sharply to the company's fiscal 2027 first-quarter results, prioritizing margin compression over top-line growth. While revenue beat expectations, concerns regarding near-term profitability and potential equity dilution triggered a significant valuation reassessment.

The stock is currently trading at $32.22, a sharp reversal from its 451.71% gain over the past 12 months. This volatility reflects the tension between the company's aggressive expansion and its current status as a loss-making entity.

Bull case

Proponents of the stock point to the company's dominant position in Earth imaging and its growing backlog as evidence of long-term viability. The firm is increasingly integrated into global defense and intelligence workflows.

Analysts remain optimistic about the company's ability to scale recurring revenue through AI-enabled services.

- Ryan Koontz of Needham maintains a Buy rating with a $53.00 price target, citing confidence in the company's data analytics potential.

- Dan Ives of Wedbush rates the stock as Outperform with a $50.00 target, highlighting mission-critical demand in the geopolitical sector.

- The company reported a record backlog of $906 million, a 72% increase year-over-year.

- The upcoming launch and commissioning of the Owl satellite constellation is scheduled for later this year.

Bear case

Skeptics emphasize that Planet Labs remains unprofitable, with adjusted EBITDA losses expected to persist as the company funds strategic investments. The high price-to-sales multiple makes the stock sensitive to any guidance misses or macro-economic shifts.

Valuation models suggest the current share price may be disconnected from near-term cash flow realities.

- Goldman Sachs maintains a Neutral stance, citing broader sector volatility and the need for valuation reassessments.

- The company's margin guidance for the remainder of the fiscal year indicates continued pressure on profitability.

- Investors have expressed concerns regarding potential equity dilution to fund future satellite deployments.

- The firm does not pay a dividend, offering no income protection for shareholders during periods of high volatility.

Fintwit's AI verdict

The algorithmic consensus currently suggests a cautious approach for those evaluating the stock at current levels. While the fundamental growth narrative remains intact, the technical setup and margin profile necessitate a wait-and-see strategy until further clarity on profitability emerges.

Market participants are closely monitoring the company's ability to convert its record backlog into tangible cash flow. The following indicator provides a summary of the current sentiment regarding the stock's immediate outlook.