Should You Buy MRVL Right Now? Analyzing the Semiconductor Sell-Off

Marvell Technology (MRVL) shares dropped 16.74% following a sector-wide sell-off. We analyze the bull and bear cases for this AI infrastructure leader.

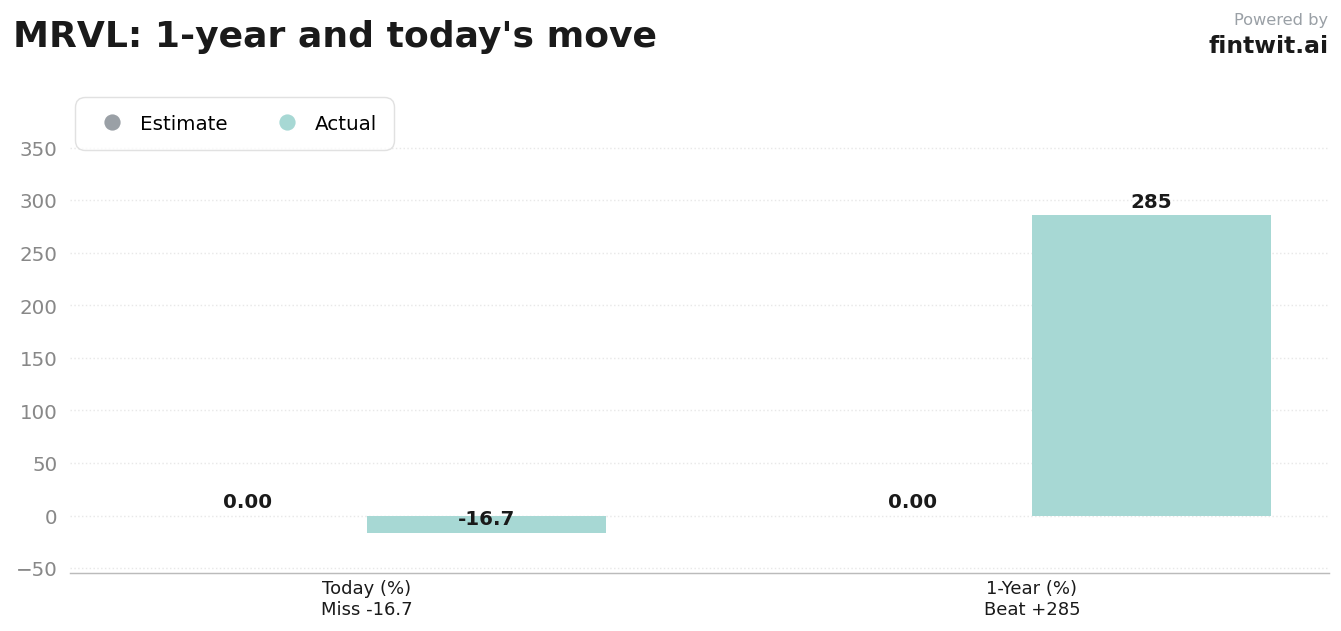

What just happened

The sharp decline in MRVL follows Broadcom's decision to maintain, rather than raise, its long-term AI revenue outlook. This shift caused investors to aggressively reassess the growth trajectory for companies with heavy exposure to custom ASICs and data center networking.

Marvell's high valuation, which reached a 285.47% gain over the last 12 months, made it particularly vulnerable to this sentiment shift. The market is now pricing in a more cautious outlook for the second half of 2026 as hyperscalers evaluate their capital expenditure efficiency.

Bull case

Despite the recent volatility, institutional support remains firm, with analysts highlighting the company's long-term positioning in the AI ecosystem.

The following factors support the long-term growth thesis for Marvell:

- Stifel analyst Tore Svanberg maintains a Buy rating with a $321 price target, citing strong market acceptance at Computex 2026.

- Oppenheimer analyst Rick Schafer maintains an Outperform rating with a $250 target, noting that Q1 and Q2 revenue outlooks remain a floor for the company.

- Evercore ISI analyst Mark Lipacis maintains a Buy rating with a $251 target, citing confidence in Marvell's AI infrastructure leadership.

- Marvell is scheduled to join the S&P 500 index on June 22, 2026, which is expected to drive significant institutional inflows.

- The company continues to see a ramp-up in its Teralynx T100 switch and custom ASIC design wins with major cloud providers.

Bear case

The primary risk to the bull thesis is the current valuation, which remains elevated despite the recent price correction.

Investors should consider the following headwinds:

- The stock trades at a forward P/E ratio between 46x and 58x, leaving little room for error if growth slows.

- Broadcom's recent commentary suggests a potential 'digestion phase' for AI spending, which could lead to lumpy revenue growth for Marvell.

- The dividend yield is negligible at approximately 0.09%, offering no meaningful income protection during periods of market volatility.

- High dependence on a small number of hyperscale customers creates concentration risk if those firms reduce their custom silicon orders.

Fintwit's AI verdict

The sentiment across financial social media remains polarized, with many traders focusing on the technical breakdown while long-term investors look for entry points near support levels. The debate centers on whether the current pullback is a temporary consolidation or the beginning of a larger trend reversal in the semiconductor sector.

Our proprietary analysis evaluates the intersection of fundamental growth, institutional positioning, and the recent price action to determine if the risk-reward profile is currently favorable for new capital. The data suggests that while the short-term technicals are damaged, the underlying business fundamentals remain intact.