JPMorgan Chase & Co (JPM) vs Bank of America (BAC): Which Is the Better Buy in 2026?

JPMorgan Chase and Bank of America are both financial titans, but their 2026 outlooks differ. We break down the numbers to find the superior investment.

The matchup

JPMorgan Chase operates as the dominant global financial institution, leveraging its fortress balance sheet to maintain a 23% Return on Tangible Common Equity (ROTCE). Its scale in investment banking and payments provides a diversified revenue stream that shields it from localized economic downturns.

Bank of America focuses on a high-tech, high-touch consumer banking model that prioritizes operating leverage. With a massive, low-cost deposit base, it aims to drive efficiency through branch optimization and AI-driven automation.

- JPM market cap: $772.86 billion.

- BAC market cap: $344.39 billion.

- JPM 1-year return: 17.55%.

- BAC 1-year return: 19.70%.

- JPM industry position: Diversified banking leader.

- BAC industry position: Consumer-focused banking giant.

Numbers side by side

Valuation metrics reveal a clear divergence in how the market prices these two institutions. JPMorgan trades at a higher premium, reflecting its consistent ability to generate superior margins despite its massive scale.

Bank of America offers a lower entry point, which may appeal to value-oriented investors looking for potential multiple expansion if regulatory capital requirements ease.

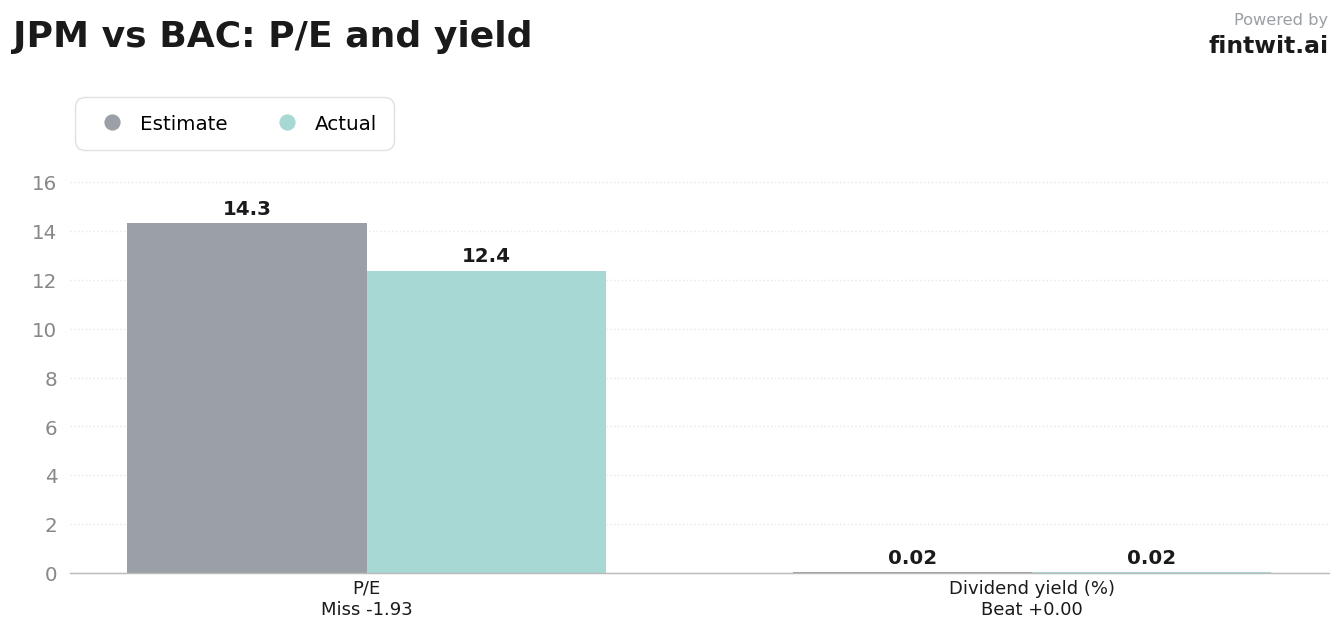

- JPM P/E Ratio: 14.31.

- BAC P/E Ratio: 12.38.

- JPM Dividend Yield: 2.01%.

- BAC Dividend Yield: 2.30%.

- JPM Revenue Growth (Q1 2026): 10% YoY.

- BAC Revenue Growth (Q1 2026): 7% YoY.

- JPM Net Margin: ~31%.

- BAC Efficiency Ratio: ~61%.

Bull and bear on each

Investors must weigh the specific risks and catalysts associated with each bank's unique business model. JPMorgan faces regulatory scrutiny regarding capital surcharges, while Bank of America navigates exposure to commercial real estate office space.

- JPM Bull: Dominance in investment banking and trading fee capture.

- JPM Bull: Successful integration of AI to drive long-term productivity.

- JPM Bear: Peaking Net Interest Income as rate tailwinds fade.

- JPM Bear: Regulatory headwinds from Basel III Endgame capital requirements.

- BAC Bull: Potential for significant capital returns via buybacks if capital rules relax.

- BAC Bull: Strong operating leverage from digital transformation.

- BAC Bear: Sensitivity to CFPB junk fee regulations.

- BAC Bear: Credit risks associated with commercial real estate portfolios.

The verdict

JPMorgan Chase stands out as the superior all-weather financial machine, justifying its premium valuation through higher profitability and unmatched scale. Its ability to maintain a 23% ROTCE while investing heavily in technology makes it a core holding for long-term investors.

Bank of America remains a compelling alternative for those seeking value, particularly if regulatory shifts allow for aggressive share repurchases. The choice depends on whether an investor prioritizes the stability of a fortress balance sheet or the potential for multiple expansion in a lower-valuation peer.