Should You Buy FUTU Right Now? Analyzing the Regulatory Fallout

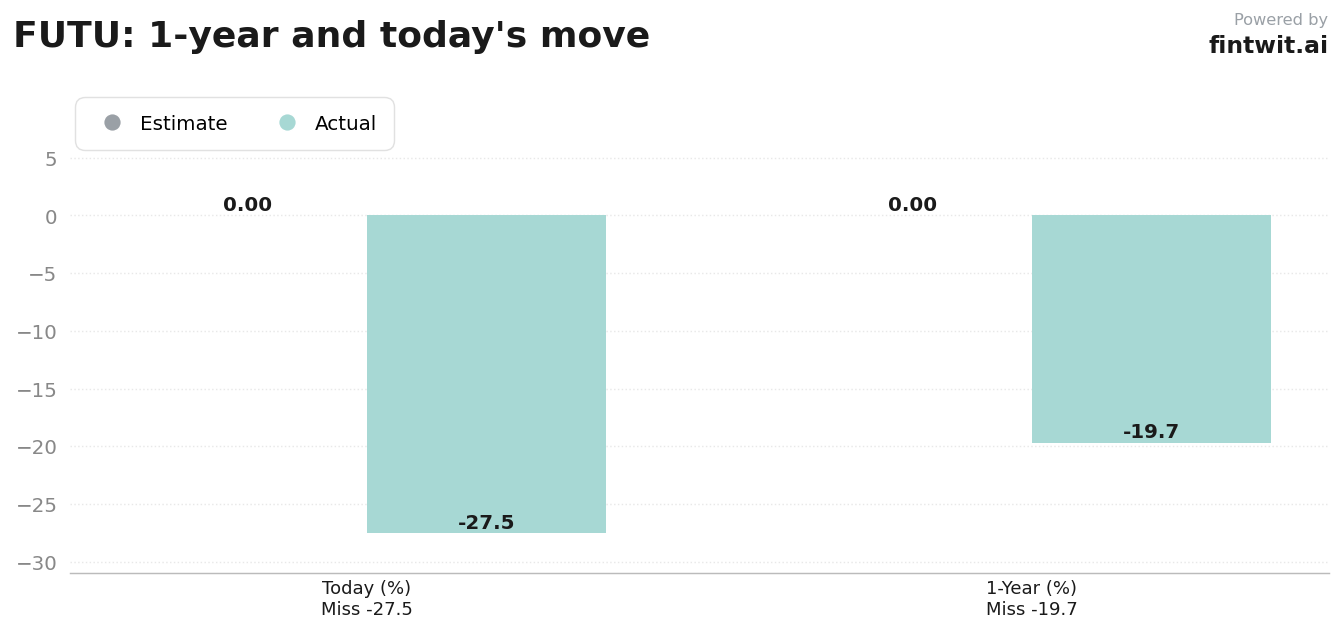

Futu Holdings shares plummeted 27.53% after a CSRC probe. Is the sell-off an overreaction or a fundamental shift in the firm's growth trajectory?

What just happened

The CSRC investigation centers on Futu's cross-border operations, which regulators claim bypassed local licensing requirements. The agency intends to confiscate illegal gains and impose significant financial penalties on the firm.

Futu is now subject to a two-year wind-down period for its mainland business. During this window, the company is strictly prohibited from onboarding new mainland clients or accepting additional fund inflows.

The market reaction reflects a sharp pivot from the company's previous high-growth narrative. Investors are now pricing in both the immediate financial hit and the long-term loss of the mainland Chinese market.

Bull case

- Citigroup analyst Judy Zhang maintains a Buy rating with a $201.00 price target, citing strong underlying fundamentals.

- Barclays analyst Jiong Shao maintains an Overweight rating and a $201.00 target, emphasizing the firm's successful expansion into Singapore, the U.S., Malaysia, and Japan.

- Q4 2025 revenue grew 45.3% year-over-year, demonstrating the company's ability to scale operations outside of its core legacy market.

- Net income surged 80.2% year-over-year in the most recent quarter, highlighting high operating margins that persist despite regional headwinds.

- The company's international client base provides a diversified revenue stream that may offset the forced exit from the mainland Chinese market over the next two years.

Bear case

- JPMorgan analyst Katherine Lei downgraded the stock to Hold from Buy and slashed the price target to $87.00 from $300.00.

- The CSRC probe creates a significant regulatory overhang that obscures the company's future earnings visibility.

- The exact amount of the 'illegal gains' confiscation remains unknown, creating a valuation floor that is difficult for analysts to quantify.

- Mainland China has historically been a critical source of client acquisition and asset inflows for the brokerage.

- The two-year wind-down mandate forces a structural change to the business model that could lead to increased client churn and higher compliance costs.

Fintwit's AI verdict

The quantitative model evaluates the current price action against the backdrop of the regulatory enforcement. While the fundamental growth metrics remain strong, the uncertainty regarding the final penalty size and the long-term impact on the client base creates a volatile environment for retail investors.

The consensus among institutional analysts has shifted toward a more cautious stance as they await further clarity on the financial impact of the CSRC mandate. The model suggests that investors should monitor the upcoming earnings call for management's specific guidance on asset migration and regional growth targets before committing capital.