Should You Buy DELL Right Now? Analyzing the AI Infrastructure Play

Dell Technologies is rallying on AI server demand. Is the 163% annual gain sustainable or is the valuation stretched?

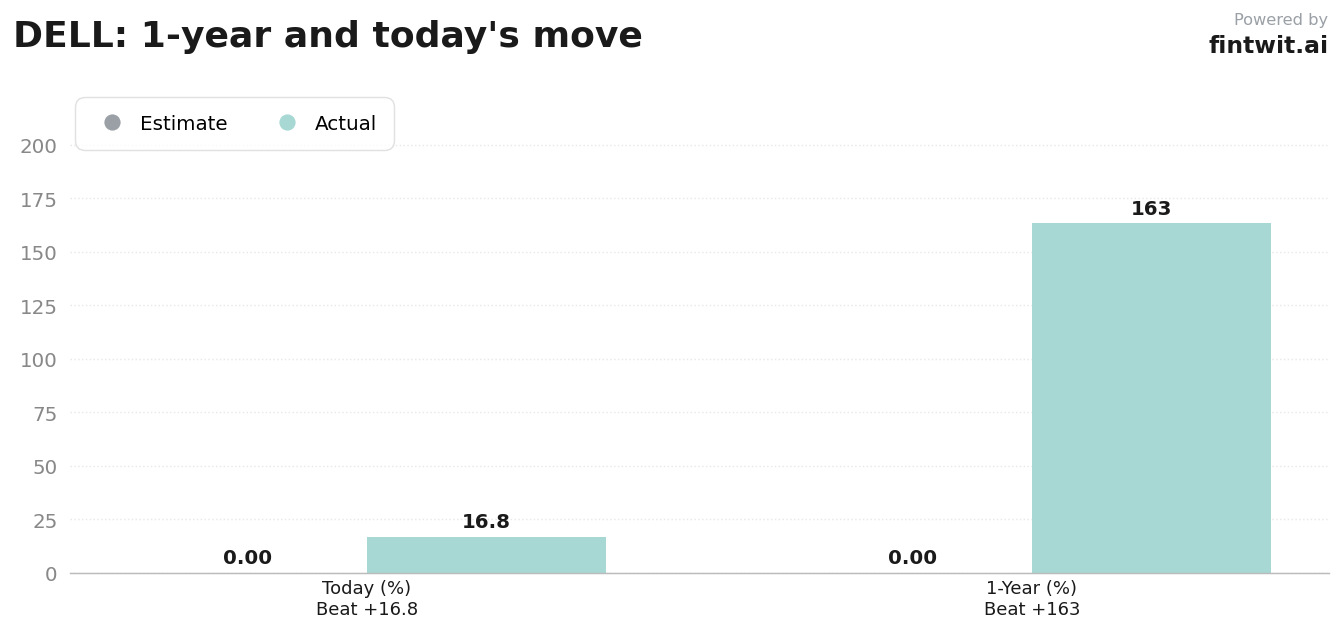

What just happened

The 16.77% single-day rally follows a series of aggressive price target revisions from major financial institutions. Market participants are reacting to the company's pivot from traditional PC manufacturing to becoming a critical provider of AI-ready infrastructure.

Dell is currently trading at a P/E ratio of 18.14, reflecting a significant valuation expansion over the last twelve months. The stock has gained 163.30% over the past year, outperforming most hardware peers as it captures enterprise spending on generative AI hardware.

Bull case

The primary driver for the bullish outlook is the company's ability to convert its massive server backlog into recognized revenue. Analysts point to the following factors supporting the current momentum:

- Dell currently holds a $43 billion AI server backlog entering fiscal 2027.

- Wells Fargo analyst Aaron Rakers maintains an Overweight rating, citing strong AI infrastructure momentum.

- Citi analyst Asiya Merchant issued a Buy rating, highlighting agentic AI workloads as a primary growth driver.

- The company is projected to achieve approximately 50% year-over-year revenue growth in the upcoming fiscal quarter.

- Enterprise demand for high-performance computing remains elevated as firms build out internal AI clusters.

Bear case

Despite the rapid growth, some analysts are signaling caution regarding the stock's current valuation. The following risks are central to the bearish or neutral perspective:

- UBS analyst David Vogt downgraded the stock to Neutral, arguing that the AI-driven growth is already fully priced into the current share price.

- The dividend yield remains low at 1.34%, as the firm prioritizes capital reinvestment over shareholder distributions.

- Market expectations for the May 28 earnings report are extremely high, leaving little room for error in a 'beat-and-raise' scenario.

- The 163% one-year rally suggests the stock may be overextended in the short term, increasing the risk of a technical pullback.

- Supply chain constraints for high-end GPUs could potentially limit the speed at which the $43 billion backlog is cleared.

Fintwit's AI verdict

The consensus among social sentiment trackers and quantitative models remains focused on the company's transition into a high-growth AI infrastructure provider. While valuation concerns persist, the sheer scale of the order backlog continues to drive aggressive positioning.

Investors are weighing the potential for further multiple expansion against the risk of a post-earnings correction. The following indicator provides a synthesized view of the current market sentiment for the ticker.