NVIDIA Corporation vs Advanced Micro Devices Inc: Which Is the Better Buy in 2026?

NVIDIA and AMD are battling for AI dominance. We break down the financials, analyst sentiment, and growth catalysts to find the better buy.

The matchup

NVIDIA currently commands a market capitalization of $4.2 trillion, driven by its dominant CUDA software ecosystem and rapid architectural cadence with Blackwell and Rubin platforms. The company maintains a near-monopoly on high-end AI training infrastructure, which has forced hyperscalers to prioritize its hardware for their data centers.

AMD is positioning itself as the primary alternative, leveraging its EPYC server CPU share gains and the Instinct MI400 series GPU roadmap. While NVIDIA focuses on the high-end software moat, AMD is capturing market share through a 'second-source' strategy, appealing to hyperscalers seeking to mitigate supply chain concentration risks.

- NVIDIA revenue growth: 85% YoY (Q1 2026).

- AMD revenue growth: 38% YoY (Q1 2026).

- NVIDIA non-GAAP gross margin: 75.0%.

- AMD non-GAAP gross margin: 55.0% with guidance for 56% in Q2.

- NVIDIA analyst targets: Evercore ISI ($413), Benchmark ($335), Keybanc ($310).

- AMD analyst targets: Evercore ISI ($579), RBC Capital ($400), Citigroup ($248).

Numbers side by side

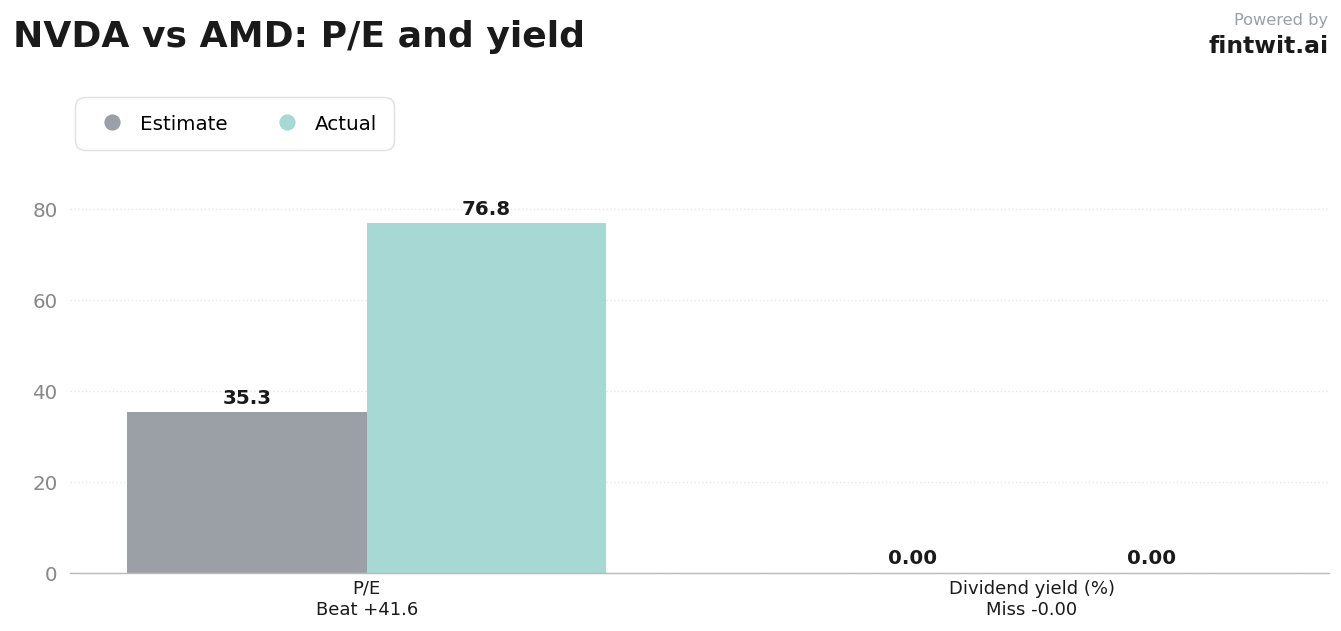

Valuation metrics highlight the premium the market assigns to NVIDIA's software-integrated hardware versus AMD's hardware-focused growth strategy. NVIDIA trades at a P/E ratio of 35.29, while AMD commands a higher P/E of 76.84, reflecting market expectations for rapid earnings acceleration in its data center segment.

Return profiles over the last year show AMD's volatility and growth potential, with a 323.81% return compared to NVIDIA's 64.01%. However, NVIDIA's 90-day performance of 10.11% suggests a more stable, albeit slower, appreciation compared to AMD's 121.72% surge in the same period.

- NVIDIA P/E Ratio: 35.29.

- AMD P/E Ratio: 76.84.

- NVIDIA 1-Year Return: 64.01%.

- AMD 1-Year Return: 323.81%.

- NVIDIA Dividend Yield: 0.0002%.

- AMD Dividend Yield: 0.0000%.

Bull and bear on each

NVIDIA's bull case rests on its unmatched scale in AI infrastructure and an aggressive $80 billion buyback program. Conversely, the bear case highlights high customer concentration and the long-term threat of hyperscalers developing in-house custom silicon.

AMD's bull case is centered on the successful execution of its rack-scale Helios systems and server CPU market share expansion. The bear case for AMD focuses on the intense competitive pressure from NVIDIA's ecosystem and potential supply chain bottlenecks at TSMC.

- NVIDIA Bull: Dominant software moat and architectural innovation.

- NVIDIA Bear: High valuation leaves little room for execution errors.

- AMD Bull: Accelerating Data Center segment growth.

- AMD Bear: Weakness in the Gaming segment and high valuation multiples.

The verdict

NVIDIA remains the primary beneficiary of the AI infrastructure buildout, maintaining an insurmountable lead through its superior software ecosystem. Its ability to sustain 75% gross margins while scaling production suggests a level of pricing power that remains unmatched in the semiconductor industry.

AMD represents a high-beta play on the semiconductor cycle, offering significant upside if it can successfully capture market share from NVIDIA's supply-constrained customers. The decision between the two depends on an investor's tolerance for the premium valuation of the market leader versus the execution risk of the challenger.