Should You Buy CRCL Right Now? Analyzing Circle Internet Group

Circle Internet Group (CRCL) shares fell 10.63% Tuesday. We break down the market catalysts, analyst sentiment, and the path forward for the stablecoin leader.

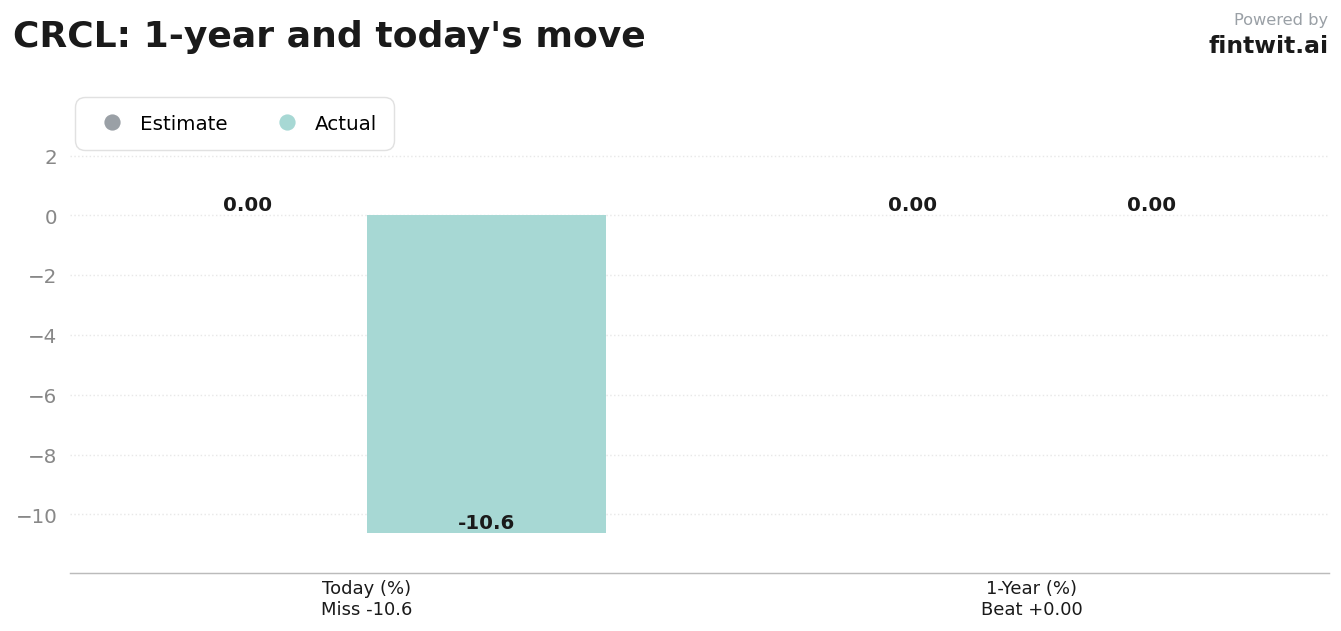

What just happened

The $33.46 billion market cap company saw shares slide as Bitcoin price volatility triggered widespread risk-off sentiment in the digital asset sector. Investors are reacting to heavy insider selling, including a $164,534 sale by director M. Michele Burns.

Margin concerns remain the primary overhang for the stock as the market digests the impact of USDC distribution economics. The following chart illustrates the recent price volatility and the current technical positioning of the stock.

The company reported its first quarter 2026 results recently, highlighting a 51% year-over-year revenue growth rate despite the current market headwinds.

Bull case

Proponents of the stock point to the firm's aggressive expansion into AI-integrated financial infrastructure and high interest income growth.

The following factors support a long-term bullish outlook for the company:

- Aletheia Capital maintains a Buy rating with a $160 price target, citing strategic growth in interest income.

- Morgan Stanley adjusted its outlook upward to $106, citing higher yield expectations and revenue from the Arc token presale.

- The company has successfully launched the Agent Stack platform to facilitate AI-driven payments.

- The firm reported a 51% year-over-year revenue growth rate in its Q1 2026 earnings report.

- The $222 million Arc token presale provides a significant capital injection for network development.

Bear case

Skeptics highlight the lack of a positive P/E ratio and the ongoing dilution risks associated with net reserve margin pressures.

The following risks currently weigh on the stock's valuation:

- KeyBanc initiated coverage with a Sector Weight rating, citing concerns over net reserve margin dilution.

- Increased competition in the stablecoin sector continues to pressure monetization strategies.

- Heavy insider selling activity has signaled potential caution among company leadership.

- The company currently lacks a positive P/E ratio, making it unattractive to traditional value investors.

- Broader crypto market volatility and ETF outflows create a high-risk environment for the stock.

Fintwit's AI verdict

The quantitative model evaluates the current market sentiment against the fundamental growth metrics provided in the Q1 2026 report. While margin compression remains a tangible threat, the aggressive expansion into AI-driven payment stacks offers a unique growth vector that traditional financial firms currently lack.

Investors should weigh the potential for long-term infrastructure adoption against the immediate volatility of the crypto markets. The following assessment reflects the current algorithmic outlook for the ticker.