G-III Apparel Group Ltd (GIII) Q1 Earnings Preview: What to Watch

G-III Apparel Group faces a critical Q1 report on June 5. We analyze the shift toward owned brands and the impact of license losses on margins.

The setup

G-III Apparel Group is currently navigating a significant structural transition. The company is moving away from its historical reliance on Calvin Klein and Tommy Hilfiger licenses, which previously anchored its revenue base.

Management has initiated a $25 million cost-savings program to protect margins during this transition. Investors are looking for evidence that owned brands like DKNY and Karl Lagerfeld can scale sufficiently to replace the lost licensing volume.

The retail environment remains challenging, with discretionary spending volatility impacting demand across the apparel sector. Supply chain costs and potential tariff pressures continue to weigh on the company's gross margin outlook for the remainder of fiscal 2027.

- Fiscal 2027 guidance targets earnings of $2.00 to $2.10 per share.

- Full-year revenue guidance is set at approximately $2.71 billion.

- The company maintains a cash position exceeding $400 million to provide strategic flexibility.

- Historical patterns indicate Q1 is typically the weakest quarter due to seasonal lulls between winter and back-to-school periods.

Consensus numbers

Wall Street sentiment has deteriorated significantly over the last 90 days, with earnings expectations for the first quarter falling by 1400%. Analysts are now modeling a loss, reflecting deep caution regarding the company's ability to maintain profitability during this transition.

The revenue estimate for the quarter sits at $529.9 million. This figure is being closely scrutinized against the backdrop of the company's recent history of earnings surprises.

MarketBeat highlights that the sharp downward revision in estimates reflects persistent concerns regarding margin compression. The consensus price target currently stands at $32.67, though volatility remains high.

- Q1 Fiscal 2027 EPS estimate: -$0.30.

- Q1 Fiscal 2027 Revenue estimate: $529.9 million.

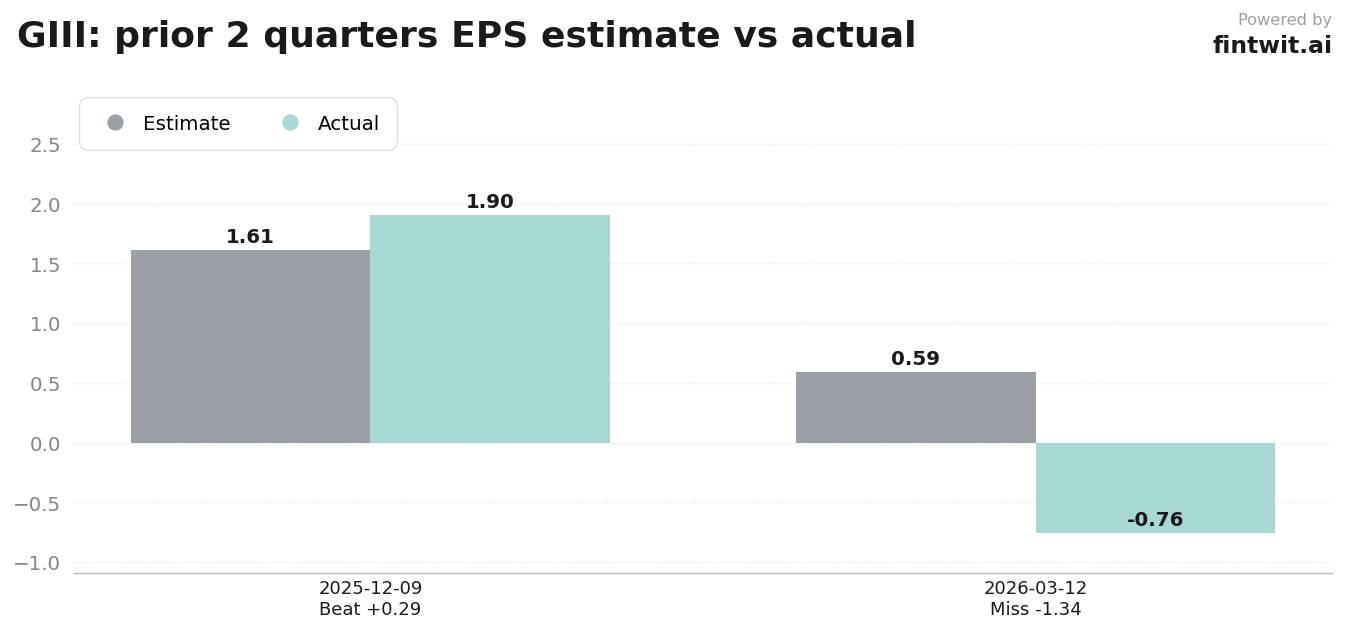

- Q4 Fiscal 2026 EPS result: $1.90 vs $1.61 estimated.

- Q4 Fiscal 2026 Revenue result: $988.6 million vs $1.01 billion estimated.

- Q1 Fiscal 2026 EPS result: -$0.757 vs $0.588 estimated.

- Q1 Fiscal 2026 Revenue result: $771.5 million vs $525.1 million estimated.

What we'll watch on the call

Management must address the revenue gap created by the exit of major PVH licenses. The primary focus will be on the growth trajectory of owned brands and their contribution to the top line.

Gross margin expansion remains a critical metric. Investors will look for commentary on how the company is managing promotional activity in a soft retail environment.

The effectiveness of the $25 million cost-savings initiative will be a key indicator of operating efficiency. Any updates on retail partner inventory levels will also provide insight into the upcoming back-to-school season.

- Performance of DKNY and Karl Lagerfeld brands in offsetting license losses.

- Updates on gross margin sustainability amid ongoing retail promotional pressure.

- Progress report on the $25 million cost-savings initiative.

- Inventory levels and ordering patterns from major department store partners.

- Management commentary on consumer discretionary spending trends.

Fintwit's AI verdict

The current market sentiment surrounding G-III Apparel Group reflects a wait-and-see approach. While the company maintains a solid cash position, the fundamental shift in its business model introduces significant execution risk that has yet to be fully priced in by the broader market.

Investors are balancing the potential for long-term margin improvement through owned brands against the immediate reality of declining earnings estimates. The upcoming report will serve as a definitive test of whether the current strategy can stabilize the bottom line before the back-to-school season begins.