Should You Buy Planet Labs (PL) Right Now?

Planet Labs (PL) shares dropped 10.31% as investors de-risk before earnings. We analyze the backlog, analyst sentiment, and the path forward.

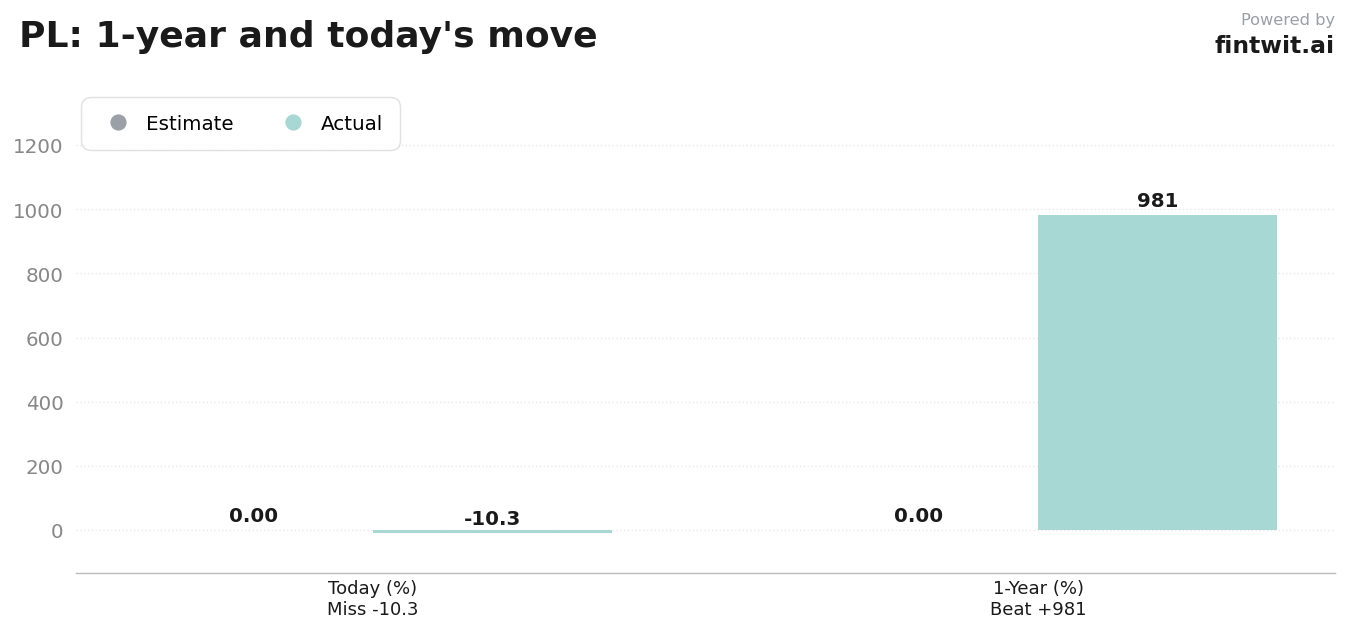

What just happened

The recent double-digit sell-off marks a significant pivot for a stock that has outperformed the broader market by a wide margin over the last year. Investors are currently de-risking their portfolios to avoid potential volatility surrounding the upcoming fiscal Q1 2027 earnings release.

Market participants are weighing the company's fundamental progress against a valuation that has expanded rapidly. This sensitivity to high multiples is common in the aerospace and defense sector when growth expectations become priced to perfection.

The chart below illustrates the dramatic 12-month trajectory and the sharp pullback observed during the most recent trading session.

Bull case

The bullish argument for Planet Labs centers on its ability to convert its massive backlog into recurring revenue. The company has successfully transitioned from a pure R&D play to a commercial entity with a clear path to scale.

Analysts remain optimistic about the firm's competitive moat in the high-resolution satellite imagery market. The following points highlight the core pillars of the bull case:

- The company maintains a record backlog of over $900 million, providing significant revenue visibility.

- Annual revenue grew 26% to $307.7 million in the most recent reporting period.

- Planet Labs achieved a maiden adjusted EBITDA profit of $15.5 million, signaling improved operational efficiency.

- Wedbush analyst Dan Ives maintains an Outperform rating with a $50 price target, citing the backlog as nearly three times annual revenue.

- The deployment of the second-generation Pelican satellite constellation is expected to enhance high-resolution data offerings.

Bear case

Skeptics point to the company's premium valuation and its reliance on third-party launch infrastructure as primary risks. The stock's massive 980.95% one-year return has left little room for error in quarterly execution.

Institutional analysts have expressed caution regarding the sustainability of current growth rates. Key concerns include:

- Goldman Sachs maintains a Neutral stance, citing valuation concerns and dependency on external launch providers.

- Morgan Stanley holds an Equal-Weight rating, questioning the pace of near-term growth acceleration.

- The company does not pay a dividend, making it less attractive to income-focused investors during market downturns.

- High sensitivity to U.S. defense budget allocations for ISR and GEOINT creates uncertainty for long-term contract growth.

- The stock is currently trading at a premium, which may lead to further volatility if earnings fail to exceed high market expectations.

Fintwit's AI verdict

The algorithmic assessment of Planet Labs weighs the company's record backlog and fundamental growth against the recent price volatility and valuation premiums. While the market is currently in a state of flux, the underlying data suggests a specific posture for those monitoring the space-data sector.

Investors should consider how the company's transition toward AI-driven product revenue might impact margins in the coming quarters. The following indicator provides the current model-driven perspective on the ticker.