Samsara Inc (IOT) Q1 Earnings Preview: What to Watch

Samsara (IOT) reports Q1 FY2027 earnings on June 4. We analyze the consensus estimates, key growth segments, and the AI-driven narrative.

The setup

Samsara continues to benefit from the digital transformation of physical operations across transportation, logistics, and construction sectors. Management has consistently demonstrated the ability to scale its AI-powered connected operations platform while moving toward sustained GAAP profitability.

The current macroeconomic environment remains a focal point for investors monitoring enterprise IT spending. Analysts are watching for any signs of lengthening sales cycles for large-scale deals that could impact revenue growth rates.

- TD Cowen maintains a Buy rating with a $45 price target.

- Goldman Sachs holds a Buy rating with a $41 price target.

- RBC Capital retains a Buy rating with a $41 price target.

- Management guidance for Q1 FY2027 revenue is set at $454 million to $456 million.

- Non-GAAP EPS guidance for the quarter is $0.12 to $0.13.

Consensus numbers

Wall Street expects Samsara to deliver revenue of $455.2 million for the first quarter of fiscal year 2027. The consensus EPS estimate stands at $0.13 per share.

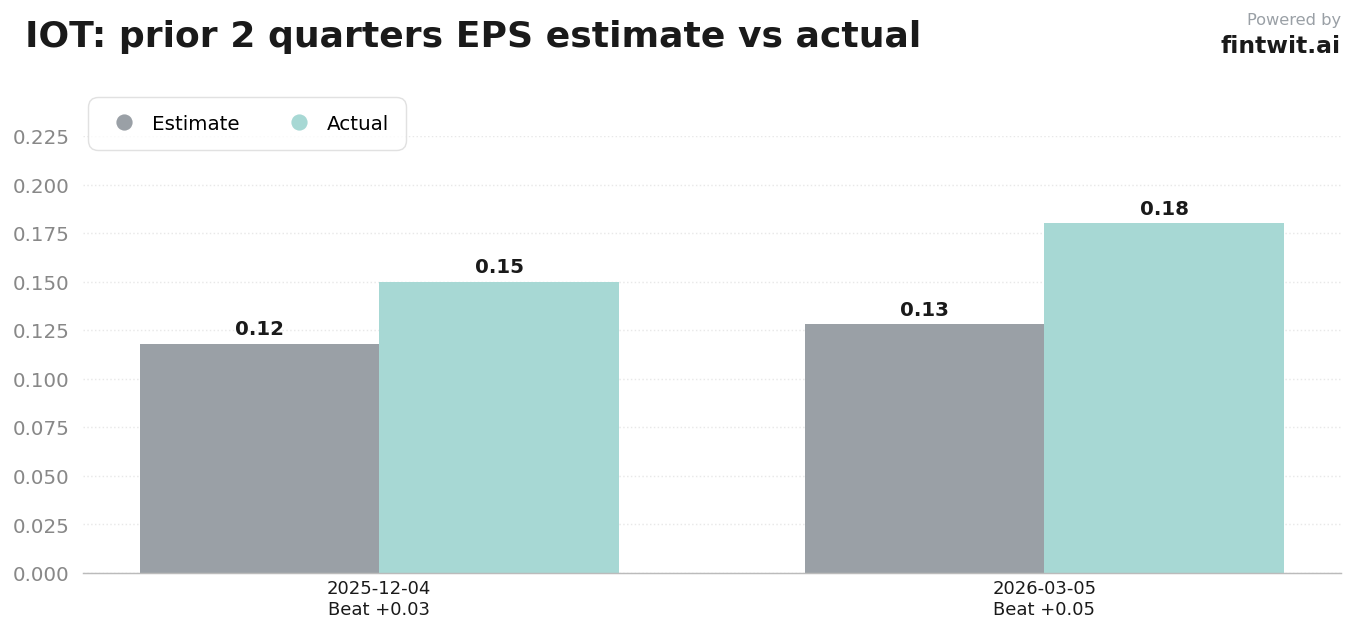

The company has a strong history of exceeding expectations, having outperformed revenue and EPS estimates in the previous two quarters. The following data reflects the recent trend of outperformance relative to analyst projections.

- Q1 FY2027 Revenue Estimate: $455.2 million.

- Q1 FY2027 EPS Estimate: $0.13.

- Q4 FY2026 Actual EPS: $0.18 (vs $0.128 estimate).

- Q4 FY2026 Actual Revenue: $444.3 million (vs $422.3 million estimate).

- Q3 FY2026 Actual EPS: $0.15 (vs $0.118 estimate).

- Q3 FY2026 Actual Revenue: $416.0 million (vs $399.3 million estimate).

What we'll watch on the call

The primary focus for investors will be the scalability of the AI platform and the company's ability to maintain high net retention rates. Management's commentary on enterprise customer expansion will be critical to validating the long-term growth thesis.

The performance of the newly launched Public Sector AI Suite will be a key indicator of market penetration in government agencies. Analysts will also look for evidence of successful cross-selling of video telematics and asset tracking solutions.

- Growth in ARR from customers contributing over $100k and $1M annually.

- Adoption rates for the Public Sector AI Suite in the current quarter.

- Trends in sales cycle length for large enterprise deals.

- Progress toward sustained GAAP profitability while maintaining AI innovation investment.

- Multi-product adoption rates among existing customers.

Fintwit's AI verdict

The quantitative models tracking Samsara's performance suggest a favorable outlook heading into the June 4 report. The combination of consistent earnings beats and the expansion of the enterprise customer base provides a compelling narrative for the stock.

Investors are weighing the potential for continued margin expansion against the competitive landscape in the IoT software market. The upcoming report will clarify whether the current valuation reflects the full potential of the company's AI-driven growth strategy.