Ciena Corp (CIEN) Q2 Earnings Preview: What to Watch

Ciena enters its fiscal Q2 2026 earnings report with significant momentum, driven by robust AI-related demand for high-speed optical networking.

The setup

Ciena is positioned as a primary beneficiary of the ongoing infrastructure build-out by hyperscalers and cloud providers. The company's role as a provider of high-speed optical networking and data center interconnect solutions has become central to the AI hardware narrative.

Management previously raised its full-year 2026 revenue guidance to a range of $5.9 billion to $6.3 billion. Investors are now looking for confirmation that this outlook remains intact despite broader macroeconomic volatility.

- Record $7 billion backlog provides significant revenue visibility for the remainder of fiscal 2026.

- Management previously guided for Q2 revenue of $1.5 billion, plus or minus $50 million.

- TD Cowen raised its price target to $675 from $425, citing the strong AI networking narrative.

- Citi increased its price target to $658 from $345, reflecting confidence in infrastructure spending.

- B. Riley maintains a neutral rating with a $531 price target, citing a cautious view on valuation.

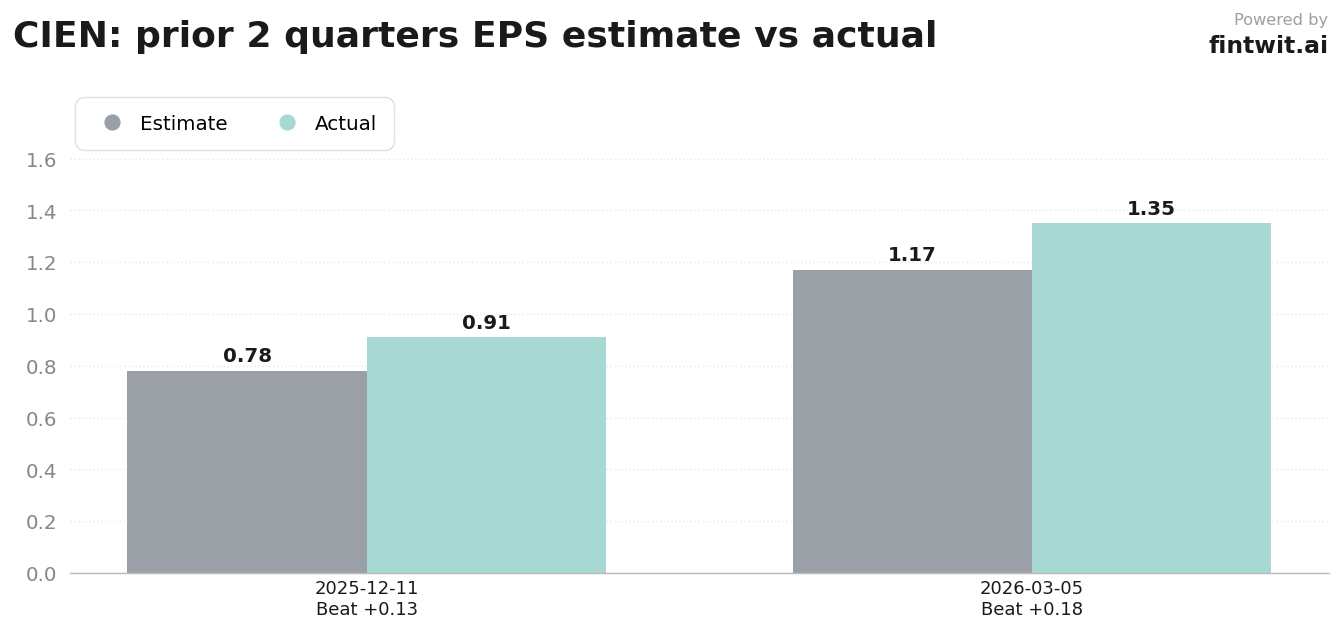

Consensus numbers

Wall Street analysts have set high expectations for the upcoming report, anticipating significant year-over-year growth across key financial metrics. The focus remains on the company's ability to scale production to meet the surge in demand for WaveLogic 6 and 800ZR pluggable optics.

Historical performance shows a trend of Ciena exceeding analyst expectations in recent quarters. The following figures represent the current consensus estimates for the fiscal Q2 period ending in April 2026.

- EPS estimate: $1.46 per share.

- Revenue estimate: $1.50 billion.

- Year-over-year revenue growth expectation: 33.6%.

- Year-over-year EPS growth expectation: 247%.

- Beat probability: 65%.

What we'll watch on the call

The primary concern for investors is the conversion rate of the $7 billion backlog into realized revenue. Supply chain constraints have been a recurring theme, and any commentary on component availability will be scrutinized for its impact on margins.

Management's perspective on hyperscaler spending patterns for the second half of 2026 and into 2027 will dictate the stock's reaction. Analysts are also monitoring the Networking Platforms segment, which accounts for approximately 80% of total revenue.

- Status of supply chain constraints and their impact on product delivery timelines.

- Gross margin trends amid product mix shifts toward newer, high-capacity optical platforms.

- Visibility into hyperscaler capital expenditure cycles for the remainder of the fiscal year.

- Performance of the Global Services segment as a driver for margin expansion.

- Updates on the adoption rate of WaveLogic 6 and RLS platforms among major service providers.

Fintwit's AI verdict

Market sentiment surrounding Ciena has shifted significantly as the company cements its status as a critical infrastructure provider for the AI era. The combination of a massive backlog and high-margin product cycles suggests that the company is well-positioned to navigate current industry headwinds.

Investors are weighing the potential for a positive surprise against the high valuation multiples currently assigned to the stock. The upcoming earnings call will likely serve as a catalyst for the next leg of price discovery.