Royal Bank of Canada (RY) Q2 Earnings Preview: What to Watch

Royal Bank of Canada (RY) reports Q2 2026 earnings on May 28. Analysts focus on HSBC Canada integration, credit quality, and capital markets performance.

The setup

Royal Bank of Canada (RY) enters the fiscal Q2 2026 reporting cycle with a market capitalization of $222.24 billion. Management, led by CEO Dave McKay, has shifted the firm's strategic focus toward aggressive growth following the successful closure of the HSBC Canada deal.

The bank's ability to maintain high valuations depends on management's conviction regarding the second half of 2026. Analysts at Jefferies, led by John Aiken, emphasize that the market is looking for clear signals on how the expanded franchise will drive profitability in a higher-for-longer interest rate environment.

- Management has prioritized strategic flexibility to support both inorganic growth and shareholder returns via dividends and buybacks.

- The bank is currently navigating a macro environment characterized by rising unemployment and household insolvency rates in Canada.

- Geopolitical uncertainty and trade tensions remain key external risks impacting the bank's diversified revenue streams.

Consensus numbers

Market consensus estimates for the quarter reflect a cautious optimism regarding the bank's operational efficiency and revenue growth. Analysts are closely monitoring whether the bank can sustain the momentum seen in previous quarters.

The following figures represent the current consensus expectations for the fiscal second quarter ending May 2026.

- EPS Estimate: $2.80

- Revenue Estimate: $12.74 billion

- Beat Probability: 65%

- Miss Probability: 15%

- Inline Probability: 20%

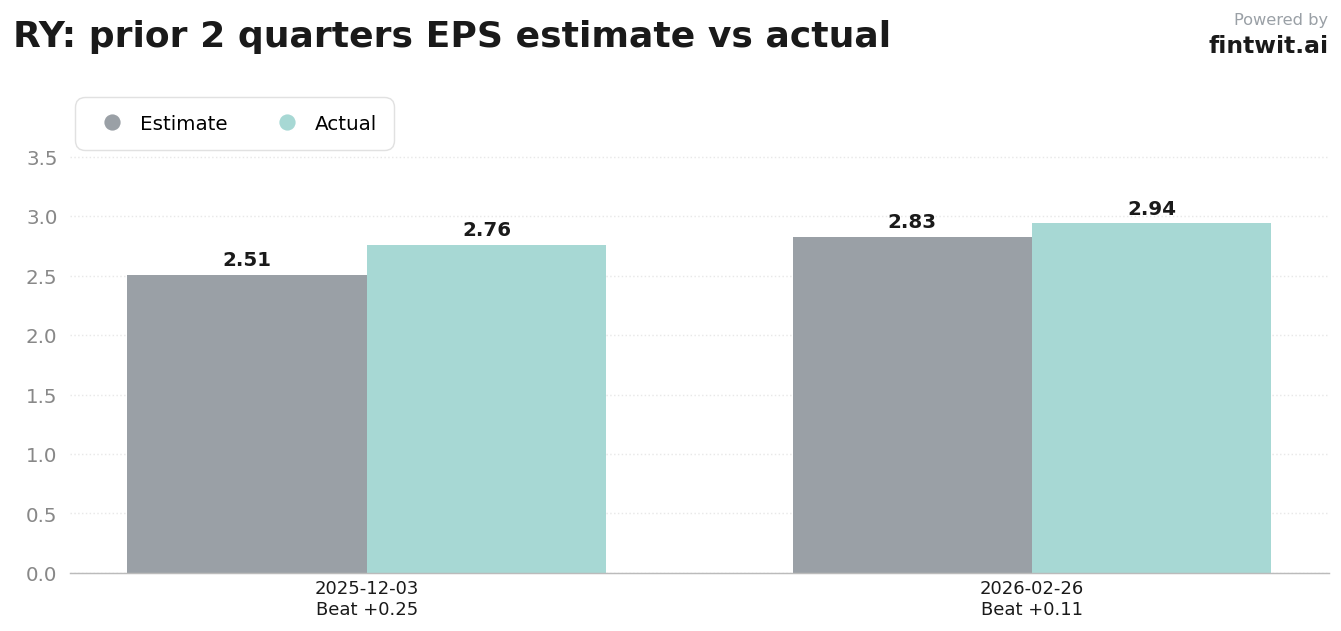

- Q1 2026 Actual EPS: $2.94 (vs $2.83 estimate)

- Q4 2025 Actual EPS: $2.76 (vs $2.51 estimate)

What we'll watch on the call

The earnings call will likely center on the bank's credit quality and the specific impact of rising interest rates on mortgage demand. Analysts are particularly interested in the trajectory of provisions for credit losses (PCLs).

Gabriel Dechaine of National Bank has noted that with margin expansion potentially stalling, the capital markets business must deliver strong results to offset domestic headwinds.

- Progress on the HSBC Canada acquisition integration and the realization of expected synergies.

- Management's outlook for loan growth resilience in the face of a subdued Canadian housing market.

- Sustainability of capital markets revenue given the potential for increased market volatility.

- Commentary on household debt stress and its correlation with rising unemployment rates.

- Updates on the bank's capital generation capacity and its implications for future buyback programs.

Fintwit's AI verdict

The quantitative outlook for Royal Bank of Canada remains constructive, driven by a history of consistent earnings surprises and a robust capital position. While macroeconomic headwinds in the Canadian consumer sector present a clear risk, the bank's diversified business model provides a significant buffer.

Investors should weigh the potential for margin compression against the long-term benefits of the HSBC Canada integration. The market's reaction to management's guidance on the second half of the year will likely determine the stock's short-term price action.