Costco Wholesale Corp (COST) Q3 Earnings Preview: What to Watch

Costco faces a valuation stress test this week. We break down the consensus numbers, key operational metrics, and the risks to the membership flywheel.

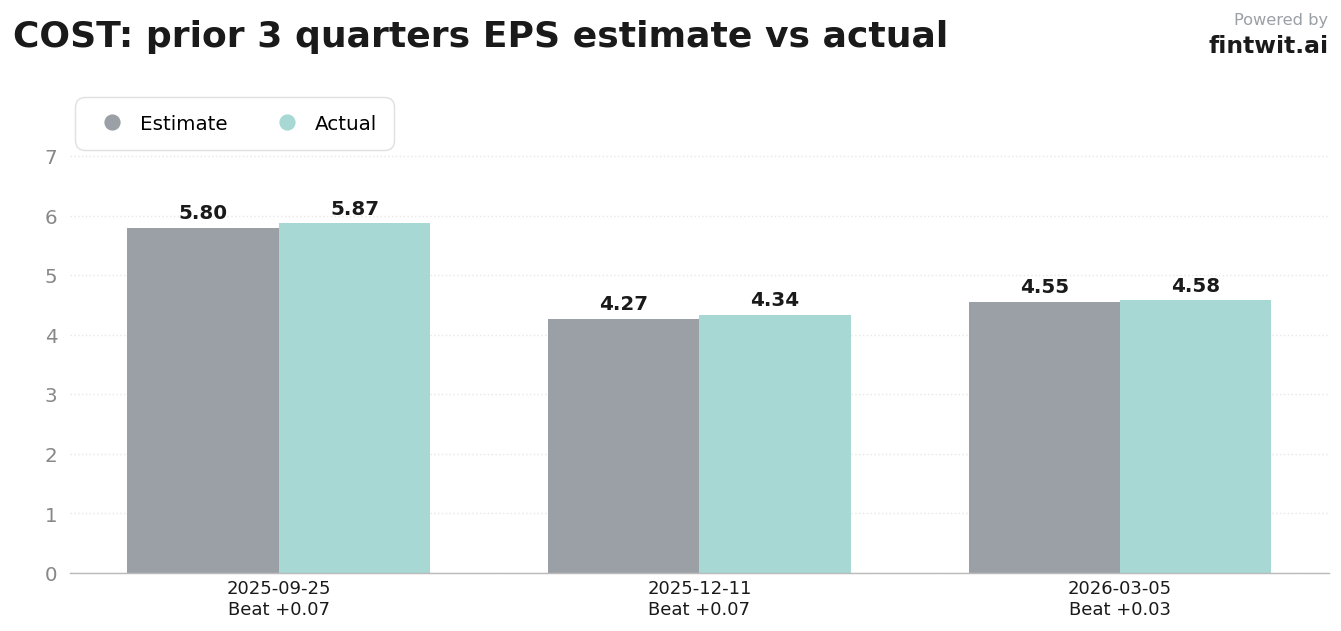

The setup

Costco continues to demonstrate operational resilience, characterized by consistent double-digit sales growth and high-margin membership income. However, the premium valuation has led to pre-earnings de-risking among institutional investors.

Management maintains a long-term focus on value-based pricing and global expansion. They continue to prioritize membership growth and operational efficiency over short-term margin maximization, despite acknowledging widespread retail competition.

- Michael Lasser of UBS maintains a bullish outlook with a $1275.00 price target.

- Rupesh Parikh of Oppenheimer holds an Outperform rating with a $1160.00 price target.

- Christopher Nardone of Bank of America maintains a Buy rating with a $1185.00 price target.

- Macro headwinds include ongoing inflation, tariff exposure, and geopolitical tensions impacting global supply chains.

Consensus numbers

Wall Street expects solid top-line performance for the third quarter, though the market is closely watching for any signs of margin compression. The company has a history of exceeding EPS expectations, as shown in the data below.

The following figures represent the current consensus estimates for the fiscal third quarter ending May 2026.

- EPS estimate: $4.98

- Revenue estimate: $69.61 billion

- E-commerce growth: 18.8% (April baseline)

- Membership renewal rate: Historically >89%

- Beat probability: 65%

- Miss probability: 25%

- Inline probability: 10%

What we'll watch on the call

Investors are looking for confirmation that the recent surge in digital sales is sustainable. The contribution of e-commerce to overall operating margins remains a critical point of debate.

Membership renewal rates serve as the primary indicator of the company's long-term health. Any deviation from the historical 89% threshold will be scrutinized as a signal of weakening consumer loyalty.

- Sustainability of the 18.8% e-commerce growth rate observed in April.

- Impact of high oil prices on fuel operations and warehouse foot traffic.

- Updates on potential capital return initiatives, including special dividends.

- Management commentary on merchandise margin pressure from potential tariff increases.

- New member acquisition trends in a softening economic environment.

Fintwit's AI verdict

The current market sentiment reflects a complex interplay between fundamental strength and valuation exhaustion. While the underlying business model remains one of the most consistent in the retail sector, the high P/E multiple leaves little room for error in the upcoming guidance.

Our proprietary analysis suggests that the market is currently pricing in a high degree of perfection. Investors should monitor the post-earnings reaction to determine if the stock can sustain its current momentum or if a consolidation period is imminent.