Deere & Company (DE) Q2 Earnings Preview: What to Watch

Deere & Company reports Q2 2026 earnings on May 21. Analysts watch for signs of a cyclical bottom as farmer spending remains constrained.

The setup

Deere & Company is currently managing a transition period characterized by weak farmer spending and low crop prices. Management has previously framed fiscal 2026 as the trough for large agricultural equipment demand.

The company is leveraging operational discipline and its 'smart industrial' strategy to offset cyclical headwinds. Investors are looking for evidence that these internal efficiencies can protect margins despite broader sector volatility.

- Fiscal 2026 net income guidance is set between $4.5 billion and $5.0 billion.

- Commodity price volatility in corn and soybeans continues to dampen capital expenditure appetite among farmers.

- Geopolitical tensions and 25% duties on imported steel and aluminum represent a $1.2 billion annual headwind.

Consensus numbers

Market expectations for the second quarter reflect a cautious outlook on the agricultural sector. Analysts are focused on whether the company can maintain its current margin profile while navigating high production costs.

The following figures represent the current consensus estimates and recent performance history for Deere & Company.

- EPS Estimate: $5.70 to $5.74.

- Revenue Estimate: $11.55 billion.

- Production & Precision Agriculture: Net sales projected to decline 5-10% for the full year.

- Construction & Forestry: Projected revenue growth of approximately 20% year-over-year.

- Small Agriculture & Turf: Expected to show double-digit revenue growth as a segment offset.

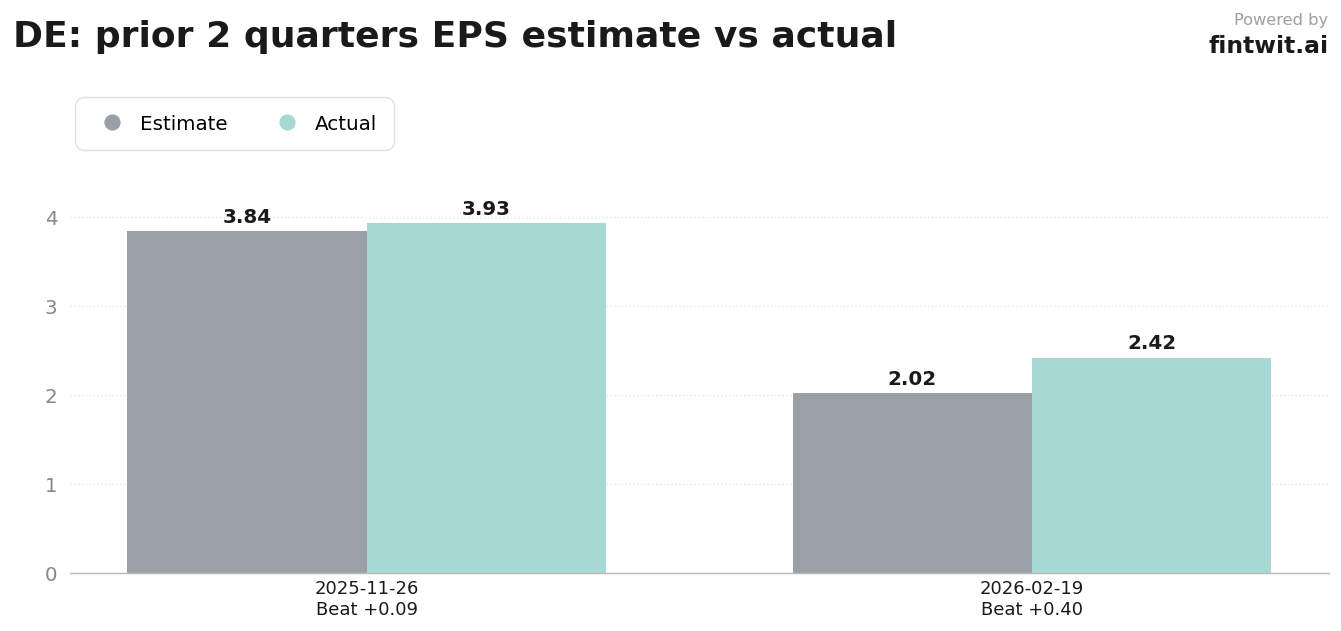

- Q1 2026 performance: EPS of $2.42 vs $2.02 estimate; Revenue of $9.61 billion vs $7.59 billion estimate.

- Q4 2025 performance: EPS of $3.93 vs $3.84 estimate; Revenue of $12.09 billion vs $9.83 billion estimate.

What we'll watch on the call

The earnings call will likely focus on the sustainability of demand for precision technology versus legacy equipment. Analysts are seeking clarity on how the company plans to mitigate the impact of ongoing tariff expenses.

Management's commentary on the used equipment market will be critical for assessing the health of new machine sales.

- Impact of elevated energy and input costs on operating margins.

- Updates on the $1.2 billion in projected annual tariff expenses.

- Sustainability of 'Precision Upgrade' demand compared to legacy sales.

- Current trends in the used equipment market and its effect on new machine inventory.

- Chris Ciolino of Bloomberg Intelligence notes that guidance suggests a more severe agricultural downturn than initially anticipated.

Fintwit's AI verdict

The market sentiment surrounding Deere & Company remains divided between near-term cyclical pressures and long-term technological potential. While the consensus rating sits at a Moderate Buy with a price target of $655.45, the immediate path forward depends on management's ability to navigate the trough of the current cycle.

Investors should monitor the upcoming earnings release for signs of margin stabilization. The balance between cost-cutting measures and the rollout of autonomous technology will determine the stock's trajectory in the coming months.