RBC Bearings Incorporated (RBC) Q4 Earnings Preview: What to Watch

RBC Bearings (RBC) reports fiscal Q4 2026 earnings on May 15. Analysts expect $3.31 EPS as the firm navigates aerospace demand and debt reduction targets.

The setup

RBC Bearings is positioned to benefit from sustained demand in the aerospace and defense sectors. Management has guided for revenue between $495 million and $505 million, reflecting a year-over-year growth rate of 13.1% to 15.4%.

The company continues to prioritize deleveraging, with a clear roadmap to retire its remaining term loan by November 2026. This focus on balance sheet health remains a central theme for institutional investors monitoring the firm's capital allocation strategy.

- KeyBanc analyst Steve Barger maintains a $535 price target, citing potential 100 bps margin expansion from normalized Boeing production schedules.

- Zacks Research upgraded the stock to a Strong Buy in February 2026, pointing to a positive Earnings ESP of +5.80%.

- Seeking Alpha contributors remain cautious, citing premium valuation multiples despite strong operational execution.

Consensus numbers

Wall Street consensus estimates for fiscal Q4 2026 center on $3.31 EPS and $505.9 million in revenue. Analysts have raised EPS estimates by 2.2% over the last 90 days, signaling increased confidence in the company's pricing power.

The wide range of EPS estimates, spanning from $2.83 to $3.50, indicates significant divergence regarding the firm's ability to absorb input costs while scaling revenue.

- Consensus EPS Estimate: $3.31

- Consensus Revenue Estimate: $505.9 million

- Management Revenue Guidance: $495 million - $505 million

- Adjusted Gross Margin Guidance: 45% - 45.25%

- SG&A Expense Guidance: 16% - 16.25% of sales

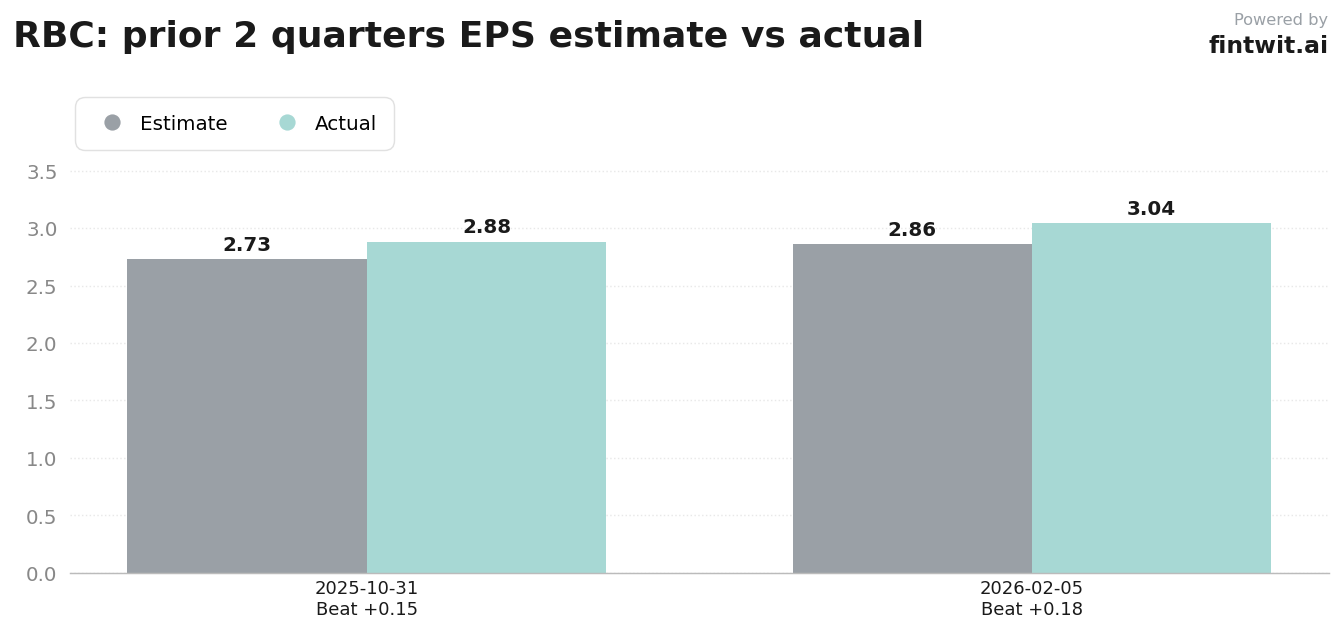

- Q3 2026 EPS: $3.04 (Beat estimate of $2.86)

- Q2 2026 EPS: $2.88 (Beat estimate of $2.73)

What we'll watch on the call

Investors are looking for clarity on the integration of the VACCO acquisition and its contribution to margin accretion. The performance of the aerospace and defense segment remains the primary driver of the company's growth narrative.

Management's commentary on industrial segment demand will serve as a bellwether for broader manufacturing trends. Any signs of destocking in the industrial channel could weigh on sentiment despite strength in the aerospace vertical.

- Can the company maintain or expand net margins despite persistent input cost pressures?

- What is the latest outlook for aerospace production rates and defense program timing?

- How is the integration of the VACCO acquisition progressing regarding margin accretion?

- Are there any signs of destocking or softening demand in the industrial segment?

- What is the status of the remaining term loan repayment schedule ahead of the November 2026 deadline?

Fintwit's AI verdict

The quantitative model suggests that the current market pricing reflects a high degree of confidence in the company's operational efficiency. With a consistent track record of beating earnings estimates, the upcoming report will test whether the firm can sustain its current momentum against a backdrop of shifting interest rates.

Investors should weigh the potential for a positive surprise against the risks associated with premium valuation multiples. The upcoming release will provide the necessary data to determine if the current growth trajectory justifies the market's optimism.