Mizuho Financial Group Inc. (MFG) Q4 Earnings Preview: What to Watch

Mizuho Financial Group (MFG) reports Q4 earnings on May 15. Analysts watch for net interest margin expansion and U.S. investment banking growth.

The setup

Mizuho Financial Group enters its fiscal Q4 2026 earnings release with significant tailwinds from the Bank of Japan's monetary policy normalization. The shift away from ultra-loose policy is expected to support net interest margins, a critical driver for the bank's profitability.

Investors are balancing these macro tailwinds against potential increases in credit costs. Geopolitical instability remains a persistent risk factor that could weigh on global market appetite and loan performance.

- Management has set a full-year profit target of JPY 1.13 trillion.

- The bank is aiming for an ROE at the higher end of 10%.

- Tsuyoshi Ueno of NLI Research Institute notes that megabanks benefit from rate hikes despite potential credit cost pressures.

- Visible Alpha analysts expect record net income for the fiscal year ended March 31, 2026.

Consensus numbers

Market expectations for the quarter remain focused on revenue stability and the successful execution of strategic growth initiatives. The bank has demonstrated a history of beating EPS estimates in recent quarters.

Analysts are closely tracking the contribution of the U.S. investment banking segment following the Greenhill acquisition. Progress in this area is essential for meeting long-term fee income growth targets.

- Consensus EPS estimate: $0.07.

- Consensus revenue estimate: $5.43 billion.

- Beat probability: 60% for a beat, 25% for a miss, and 15% for inline results.

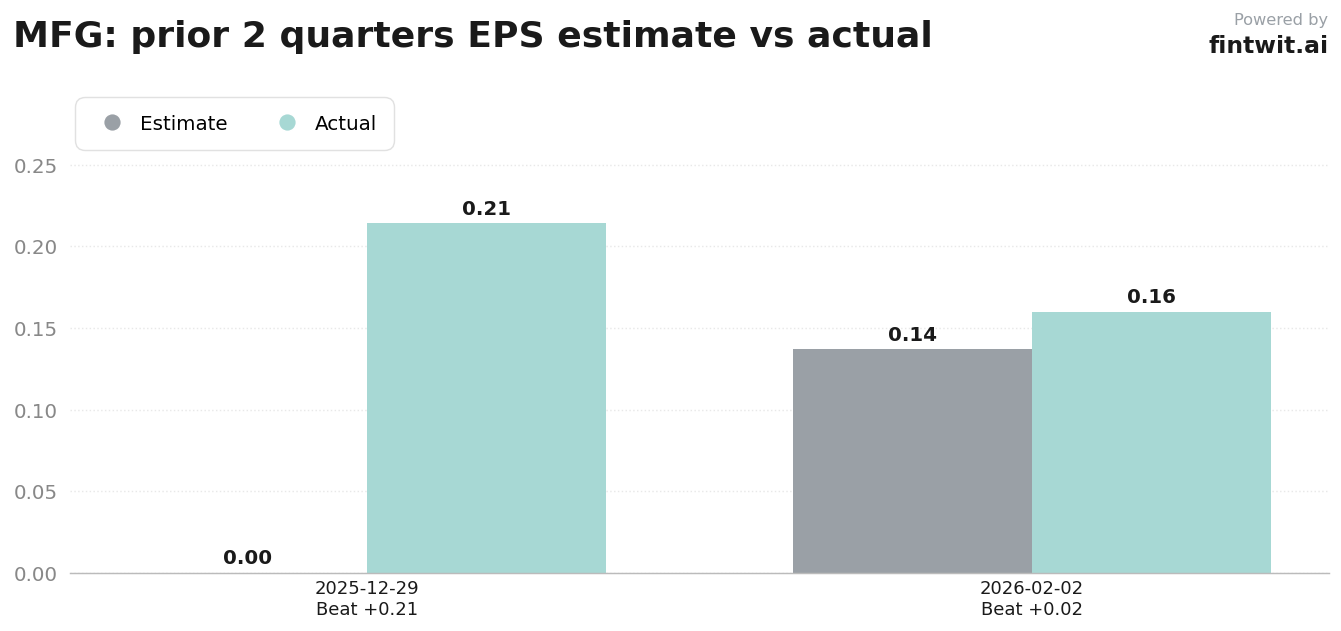

- Q3 2026 EPS result: $0.16 versus an estimate of $0.137.

- Q3 2026 revenue result: $14.24 billion versus an estimate of $5.26 billion.

What we'll watch on the call

Management's commentary on the JGB portfolio will be a focal point for institutional investors. The duration risk associated with rising interest rates remains a key area of scrutiny.

The bank's progress toward its top-ten U.S. investment banking fee income goal will be evaluated against the current macroeconomic backdrop. Analysts will also look for updates on NISA account growth within the wealth management division.

- Management strategy for mitigating unrealized losses in the fixed-income portfolio.

- Updated outlook for credit costs in light of potential private credit defaults.

- Integration milestones for recent acquisitions in the Americas.

- Impact of U.S. economic resilience on overseas corporate banking revenue.

Fintwit's AI verdict

The quantitative models suggest a favorable setup for Mizuho as the firm leverages the ongoing normalization of Japanese monetary policy. While geopolitical headwinds are acknowledged, the bank's valuation and strategic focus on fee-based income streams provide a compelling narrative for long-term holders.

Market participants are weighing the potential for record net income against the risks of credit provisioning. The upcoming earnings call will serve as a litmus test for whether the bank can sustain its current momentum in a higher-rate environment.