QXO Inc. (QXO) Q1 Earnings: The Breakdown

QXO missed Q1 expectations as it integrates major acquisitions. We analyze the building products distributor's path to $50 billion in revenue.

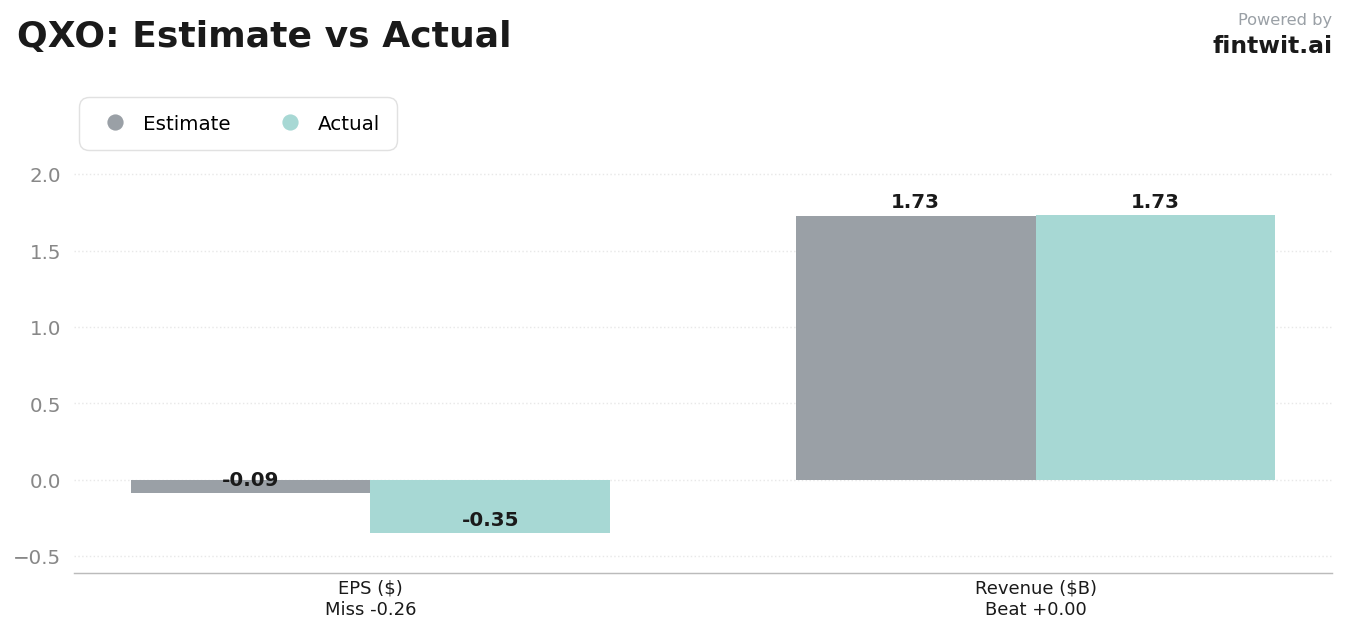

The numbers

The company reported a top-line figure that fell short of Wall Street expectations during the first quarter of 2026.

Operational results were pressured by integration costs and broader industry softness in the building products sector.

- Revenue: $1.73 billion reported vs. $1.76 billion consensus estimate.

- Adjusted diluted EPS: -$0.12 reported vs. -$0.09 consensus estimate.

- Residential roofing products: 46.2% of total sales.

- Non-residential roofing products: 26.8% of total sales.

- Complementary building products: 26.2% of total sales.

What drove the quarter

QXO is executing an aggressive M&A strategy to consolidate the $800 billion building products distribution market.

The recent $2.25 billion acquisition of Kodiak Building Partners serves as the primary engine for current scale.

Management is now focused on the pending $17 billion acquisition of TopBuild Corp., which is slated to close in Q3 2026.

- Integration risks remain a primary concern for shareholders as the company scales.

- Operational costs are currently outpacing gross profit growth.

- Macroeconomic sensitivity to interest rate changes continues to impact construction demand.

- CEO Brad Jacobs remains the central figure in the firm's operational execution.

Forward guidance

Management reiterated its long-term strategic objective to reach $50 billion in annual revenue within the next decade.

Wall Street analysts remain largely constructive on the stock despite the recent quarterly miss, citing the long-term consolidation potential.

- Citigroup: Buy rating with a $30.00 price target.

- Oppenheimer: $32.00 price target.

- Keybanc: $32.00 price target.

- RBC Capital: $28.00 price target.

Fintwit's AI verdict

The quantitative model evaluates QXO through the lens of its aggressive acquisition pipeline and its positioning within the fragmented building materials supply chain. While the current earnings report highlights short-term margin compression, the underlying growth thesis relies on the successful integration of massive scale-building assets.

Our proprietary analysis identifies specific tailwinds related to aging housing stock and infrastructure spending that may provide a floor for future performance. Investors should monitor the integration milestones of the TopBuild acquisition as a primary indicator of operational health.