Is Kinross Gold Corporation (KGC) Undervalued?

Kinross Gold (KGC) trades at a 13.6x P/E. We evaluate if the gold miner is undervalued relative to peers and its own growth pipeline.

The headline number

Kinross Gold Corporation currently commands a market capitalization of $32.02 billion. The stock trades at a price of $31.27 with a dividend yield of 0.49%.

Valuation metrics suggest a divergence in market sentiment. Independent analyst firms provide a wide range of fair value estimates for the stock.

- Seeking Alpha Contributor: Strong Buy rating with a fair value estimate of $31.39.

- Simply Wall St: Undervalued status with a calculated fair value of $47.31.

- Alpha Spread: Overvalued status with a fair value estimate of $24.50.

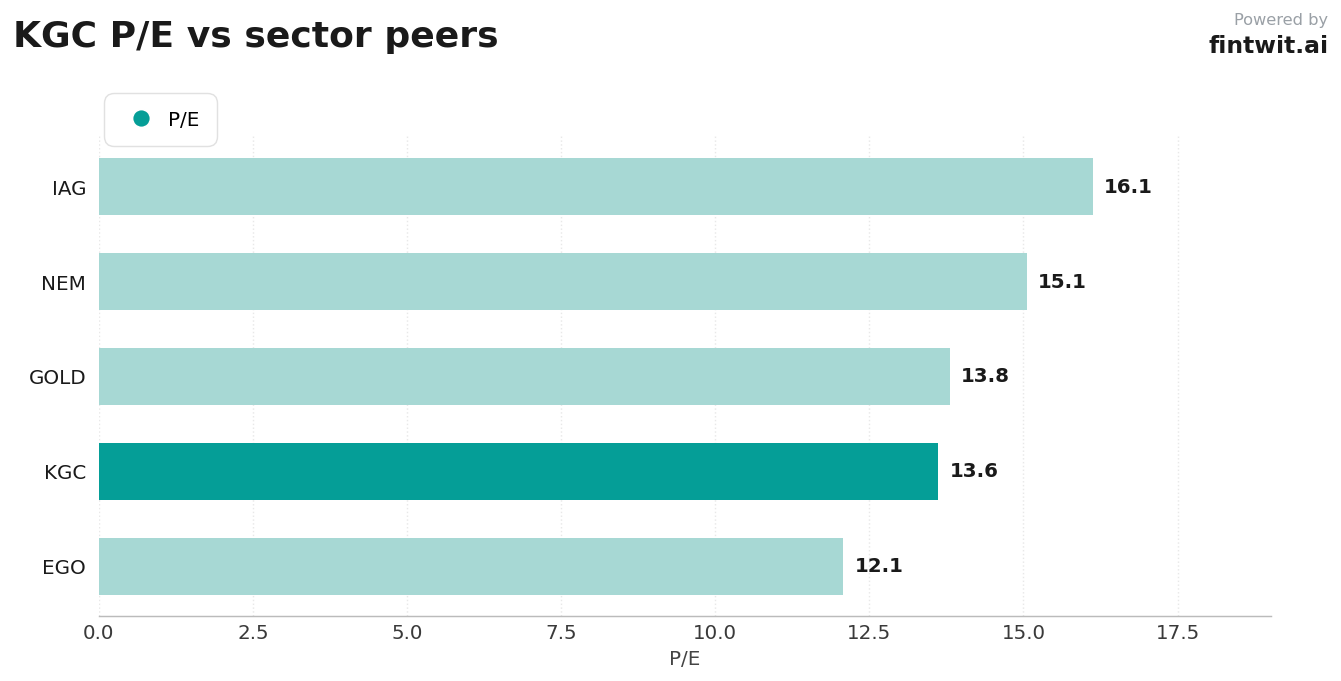

Peer comparison

Kinross Gold operates within a competitive landscape of major gold producers. Its P/E ratio of 13.61 sits in the middle of the peer group, suggesting neither extreme premium nor extreme discount relative to sector leaders.

Investors often use these multiples to gauge relative value. The following data highlights how KGC compares to its primary industry peers.

- Newmont Corp (NEM): Trades at a 15.05 P/E ratio, reflecting a premium for its larger market capitalization.

- Iamgold Corp (IAG): Trades at a 16.12 P/E ratio, indicating a higher valuation multiple than KGC.

- Eldorado Gold Corp (EGO): Trades at a 12.07 P/E ratio, representing a lower valuation multiple than KGC.

- Barrick Gold Corporation (GOLD): Trades at a 13.8 P/E ratio, showing a valuation closely aligned with KGC.

Bull vs bear

The investment thesis for Kinross hinges on its ability to convert gold production into shareholder returns. The company plans to allocate 40% of free cash flow toward dividends and buybacks by 2026.

Conversely, risks remain tied to commodity price sensitivity and operational execution. Management must navigate rising costs to maintain margins.

- Bull Case: Strong free cash flow generation of $2.47 billion projected for 2025 supports aggressive capital returns.

- Bull Case: High-return organic growth projects like Great Bear and Lobo-Marte provide long-term production visibility.

- Bull Case: Net cash position of approximately $1.4 billion provides a buffer against gold price volatility.

- Bear Case: Rising all-in sustaining costs (AISC) threaten to compress margins if gold prices soften.

- Bear Case: Significant capital expenditure requirements for growth projects may limit near-term cash distributions.

- Bear Case: Geopolitical risks in West Africa, specifically at the Tasiast mine, remain a persistent threat to production stability.

Fintwit's AI verdict

The quantitative model highlights a favorable alignment between current operational performance and the company's long-term production targets. By maintaining stable output through 2028, the firm provides a predictable baseline for cash flow modeling.

Market participants appear to be weighing the benefits of the current net cash position against the potential for cost inflation in the mining sector. The balance of these factors suggests that the current valuation provides an attractive entry point for those seeking exposure to gold producers.