Palo Alto Networks (PANW) Q3 Earnings Preview: What to Watch

Palo Alto Networks reports Q3 FY2026 earnings on June 2. Analysts focus on CyberArk integration costs, platformization success, and enterprise IT spending.

The setup

Palo Alto Networks is navigating a complex transition as it integrates the $25 billion CyberArk acquisition. Management is balancing aggressive platform consolidation with the need to maintain margins amidst potential enterprise IT spending softness.

Market sentiment remains cautiously optimistic despite sector-wide volatility. Investors are looking for evidence that the company can continue to displace incumbent vendors through its AI-powered security suite.

- Benchmark analyst Yi Fu Lee maintains a Buy rating with a $270 price target, citing expected strength in free cash flow.

- Wedbush analyst Dan Ives holds a Buy rating and a $300 target, arguing that recent sector weakness is peer-specific rather than a systemic issue for PANW.

- Morgan Stanley analyst Hamza Fodderwala set a $253 target, focusing on whether RPO growth can exceed current guidance.

- Macroeconomic headwinds include softening enterprise IT budgets and potential contagion risks from cybersecurity peers like Zscaler.

Consensus numbers

Wall Street expects Palo Alto Networks to report revenue of approximately $2.94 billion for the third quarter of fiscal year 2026. This represents year-over-year growth of roughly 28% to 29%.

Non-GAAP earnings per share are projected at $0.81. The company previously guided for EPS in the range of $0.78 to $0.80.

- Revenue estimate: $2.94 billion.

- Non-GAAP EPS estimate: $0.81.

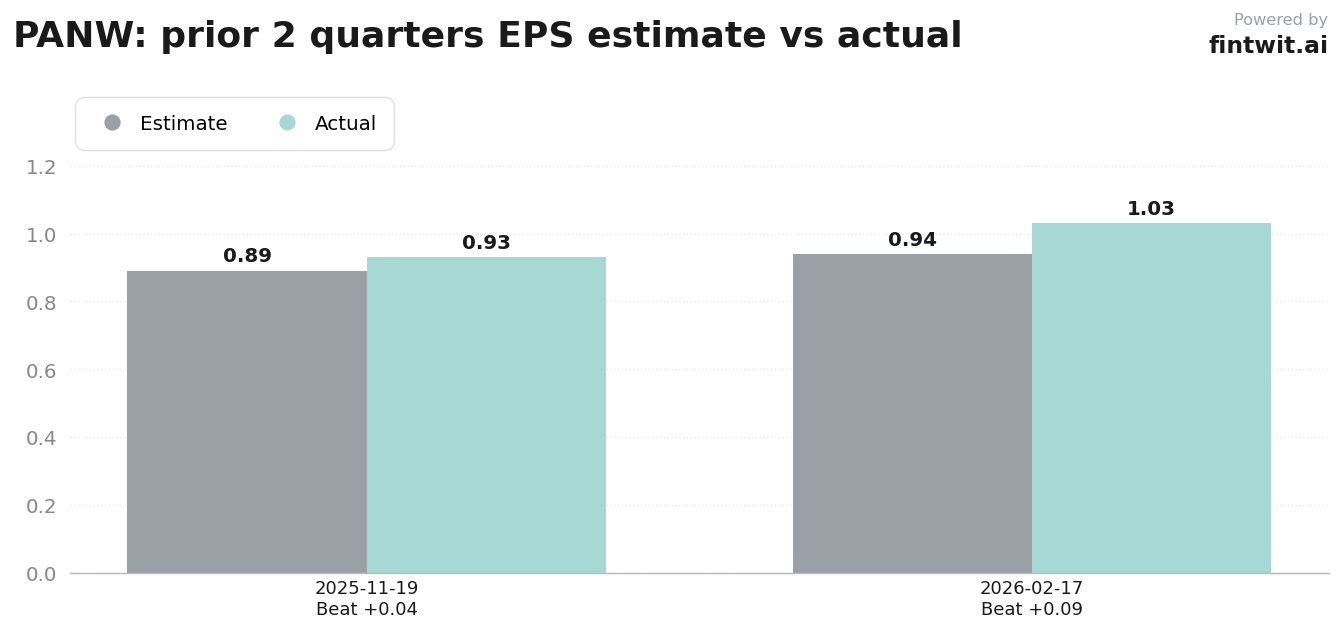

- Q1 FY2026 actual EPS: $0.93 (vs $0.891 estimate).

- Q2 FY2026 actual EPS: $1.03 (vs $0.939 estimate).

- Full-year FY2026 EPS guidance: $3.65 to $3.70.

What we'll watch on the call

The primary focus for analysts will be the financial impact of the CyberArk integration. Investors need clarity on whether synergy realization is tracking ahead of or behind the initial $25 billion deal model.

Management's commentary on sales force productivity is essential. Any signs of turnover or disruption following the M&A activity could signal near-term operational friction.

- Next-Generation Security (NGS) ARR: Tracking the acceleration of AI-driven platform adoption.

- Product Revenue: Monitoring for signs of a firewall refresh cycle or potential pull-forward activity.

- Remaining Performance Obligations (RPO): Assessing the health of long-term contract commitments.

- Customer Retention: Evaluating the effectiveness of the platformization strategy in displacing legacy point-solution competitors.

- Enterprise Spending: Identifying any shifts in IT budget allocation due to macroeconomic uncertainty.

Fintwit's AI verdict

The quantitative model suggests that the current valuation reflects a high degree of confidence in the company's long-term platform strategy. While integration risks from the CyberArk acquisition remain, the underlying demand for AI-enhanced security appears to provide a significant floor for the stock.

Investors should monitor the post-earnings price action relative to the $250 level, as this will likely dictate the technical trend for the remainder of the fiscal year. The combination of strong historical beat rates and regulatory tailwinds creates a unique setup for the upcoming print.