Palo Alto Networks Inc (PANW) Q3 2026 Earnings Preview: What to Watch

Palo Alto Networks enters Q3 2026 with strong momentum. We break down the consensus numbers, key metrics, and the AI-driven outlook.

The setup

Palo Alto Networks continues to lean into its platformization strategy to capture market share in the cybersecurity sector. Management has prioritized the integration of major acquisitions like CyberArk and Chronosphere to bolster its AI-driven security offerings.

The company faces a complex macro environment characterized by softening enterprise IT spending. Despite this, analysts remain bullish on the firm's ability to maintain high margins while scaling its Next-Generation Security (NGS) business.

- Benchmark analyst Yi Fu Lee raised his price target to $270, citing confidence in NGS ARR performance.

- Wedbush analyst Daniel Ives maintains an Outperform rating with a $300 price target, viewing recent sector volatility as peer-specific.

- Morgan Stanley analyst Hamza Fodderwala holds a positive outlook, highlighting the company's consistent market share gains.

- The White House directive on AI-enhanced cybersecurity serves as a potential tailwind for long-term government contract growth.

Consensus numbers

Wall Street expects Palo Alto Networks to deliver solid growth in its Q3 2026 results. The consensus estimates reflect a focus on top-line expansion and operational efficiency.

The company has a history of exceeding earnings expectations over the last two quarters, providing a baseline for investor optimism.

- Q3 2026 EPS estimate: $0.81.

- Q3 2026 revenue estimate: $2.944 billion.

- Management guidance range for revenue: $2.941 billion to $2.945 billion.

- Management guidance range for non-GAAP EPS: $0.78 to $0.80.

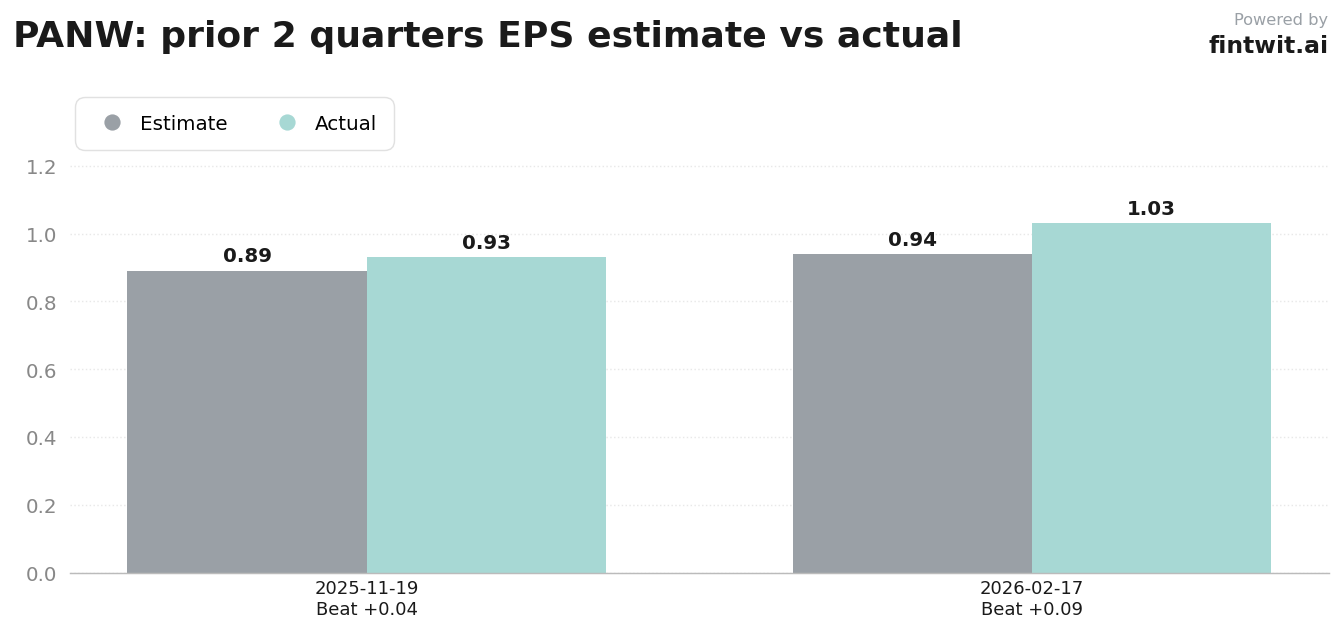

- Q1 2026 actual EPS: $0.93 (vs $0.891 estimate).

- Q2 2026 actual EPS: $1.03 (vs $0.939 estimate).

What we'll watch on the call

Investors are looking for clarity on how the company plans to sustain its 37% cash flow margin target. Integration costs from recent M&A activity remain a primary focus for analysts assessing near-term profitability.

The impact of the recent zero-day vulnerability, CVE-2026-0300, is a critical point of interest. Management's commentary on customer sentiment and operational response will likely dictate the tone of the Q&A session.

- Next-Generation Security (NGS) ARR growth as a proxy for platformization success.

- Product revenue stabilization trends in the hardware segment.

- Synergy realization timelines for the CyberArk and Chronosphere acquisitions.

- Evolution of the platformization strategy to defend against AI-security competitors.

- Operating income performance relative to high integration expenses.

Fintwit's AI verdict

The current market sentiment surrounding Palo Alto Networks is heavily influenced by its aggressive expansion and platform consolidation. While valuation multiples remain elevated, the underlying demand for integrated security solutions appears to be outpacing broader IT spending trends.

Investors are weighing the risks of share dilution against the long-term potential of the company's AI-driven product suite. The upcoming earnings call will be the primary indicator of whether the firm can maintain its current growth trajectory in a tightening spending environment.