Dollar General Corporation (DG) Q1 Earnings Preview: What to Watch

Dollar General faces a critical Q1 earnings report on June 2. We analyze the margin headwinds and consumer trends shaping the outlook for the retailer.

The setup

Dollar General enters the Q1 2026 earnings cycle under the leadership of CEO Jerry 'JJ' Fleeman Jr. The company is currently executing a 'back-to-basics' operational strategy designed to stabilize store conditions and improve inventory management.

Wall Street remains divided on the efficacy of these operational shifts. While some analysts point to progressive improvements, others remain skeptical about the company's ability to offset structural cost headwinds in the near term.

- Management FY 2026 EPS guidance is set between $7.10 and $7.35.

- Net sales growth is projected at approximately 3.7% to 4.2% for the fiscal year.

- Same-store sales growth is expected to land between 2.2% and 2.7%.

- The company faces a higher effective tax rate following the expiration of the Work Opportunity Tax Credit.

Consensus numbers

Analysts have set a cautious bar for the upcoming quarter as the company balances inflationary pressures against its value-oriented business model. The market will be looking for evidence that the company can sustain the momentum seen in previous quarters.

The following figures represent the current consensus expectations for the Q1 2026 report.

- EPS Estimate: $1.89 per share.

- Revenue Estimate: $10.817 billion.

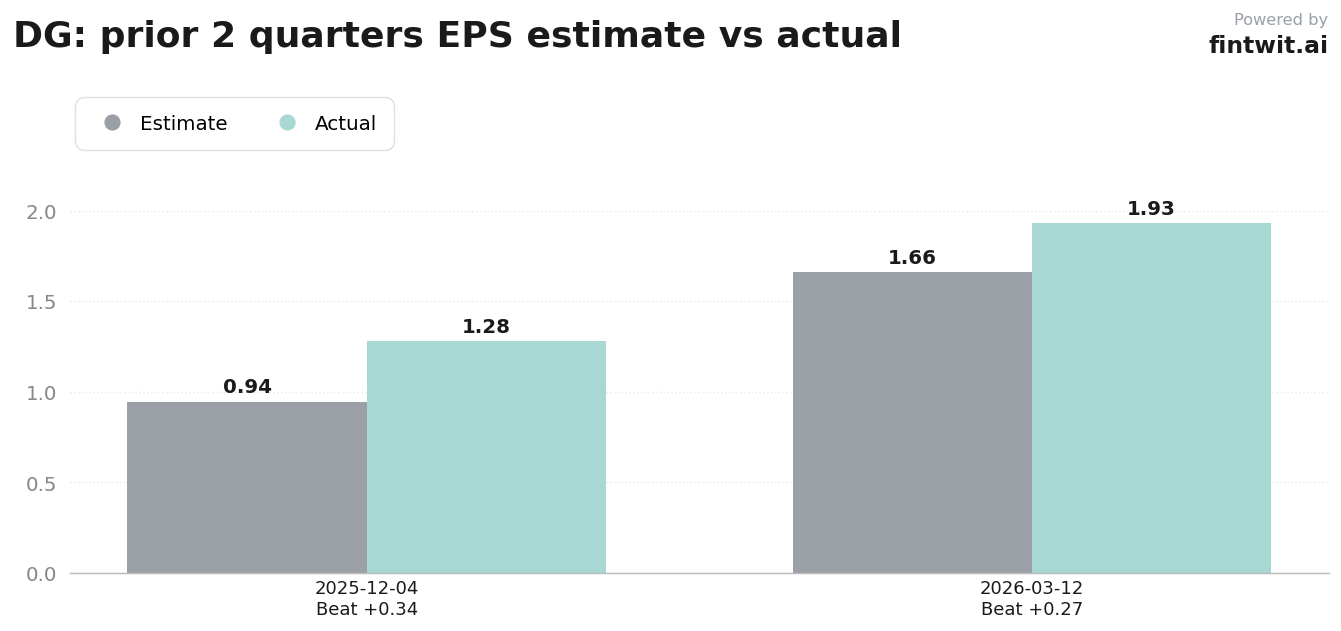

- Q4 2025 EPS beat: $1.28 actual vs $0.945 estimated.

- Q4 2025 Revenue: $10.649 billion vs $10.616 billion estimated.

- Q1 2026 EPS beat: $1.93 actual vs $1.66 estimated.

- Q1 2026 Revenue: $10.911 billion vs $10.811 billion estimated.

What we'll watch on the call

The primary focus for investors will be the performance of the consumables segment, which serves as the main driver of traffic. Analysts are looking to see if the company is successfully capturing trade-down shoppers who are increasingly sensitive to grocery inflation.

Additionally, the non-consumables segment, including home and apparel, will be monitored for signs of margin expansion. These higher-margin categories are essential for the company's long-term profitability goals.

Analyst sentiment remains varied across the street, reflecting the uncertainty surrounding the company's near-term margin recovery timeline.

- Michael Lasser (UBS): Buy rating, $168.00 price target.

- Joseph Feldman (Telsey Advisory Group): Market Perform rating, $140.00 price target.

- S. Hudson (Rothschild & Co Redburn): Sell rating, $90.00 price target.

- Shrink mitigation: Updates on how current efforts are impacting gross margin expansion.

- Consumer behavior: Impact of persistent grocery inflation on basket size and frequency.

- Tax headwinds: Clarity on the timeline for margin recovery given the expiration of the Work Opportunity Tax Credit.

Fintwit's AI verdict

The market is currently pricing in a high level of volatility for the upcoming release, with shares potentially swinging by 8.5% based on the results. Investors are weighing the potential for operational improvements against the reality of a constrained consumer base.

The upcoming report will serve as a definitive test of whether the current strategic pivot is sufficient to overcome the structural challenges facing the discount retail sector.