Oracle Corporation (ORCL) Q4 Earnings Preview: What to Watch

Oracle (ORCL) enters its fiscal Q4 2026 report with high expectations for AI infrastructure. We break down the key numbers and risks for the print.

The setup

Oracle has pivoted its business model to prioritize AI infrastructure and cloud services, making the fiscal Q4 print a litmus test for its long-term strategy. The market is currently focused on whether the company can maintain its rapid growth trajectory while managing massive capital expenditure requirements.

Management has set an ambitious tone for the coming fiscal years, including a revenue target of $90 billion by FY2027. Investors are looking for concrete evidence that these targets remain achievable despite macroeconomic headwinds and rising costs for data center expansion.

- Analysts at Barclays maintain an Overweight rating with a $240 price target, citing confidence in AI-related growth.

- Guggenheim analysts reiterate a Buy rating with a $400 target, noting the expected ramp in CapEx to $75 billion in FY2027.

- Scotiabank maintains a bullish rating and raised its price target to $290 ahead of the earnings release.

- Persistent high interest rates increase the cost of financing the company's debt-funded AI infrastructure expansion.

Consensus numbers

Wall Street expects Oracle to deliver solid top and bottom-line growth for the quarter ending May 2026. The consensus revenue estimate stands at $19.10 billion, marking a 20% increase from the prior year.

The company has a track record of beating earnings estimates, though the margin of surprise has fluctuated in recent quarters. Investors are watching for any deviation from these targets as a signal of potential cooling in enterprise cloud demand.

- EPS Estimate: $1.96.

- Revenue Estimate: $19.10 billion.

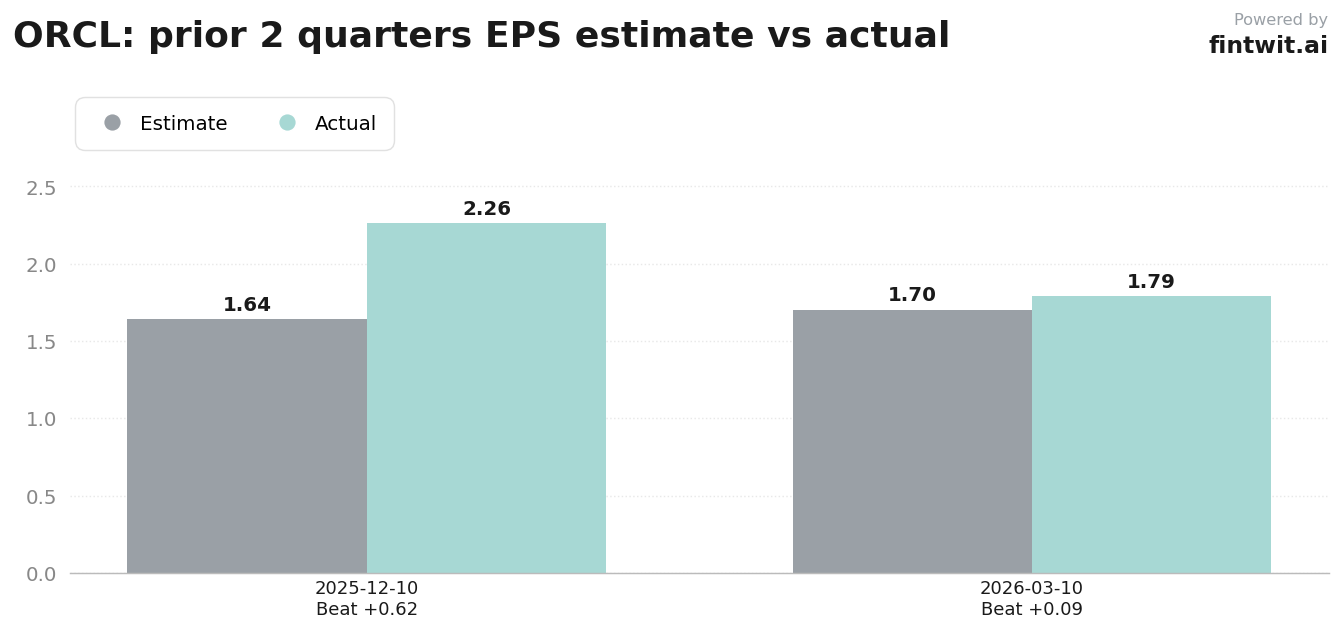

- Q3 2026 Actual EPS: $1.79 (Estimate: $1.70).

- Q2 2026 Actual EPS: $2.26 (Estimate: $1.64).

- Beat Probability: 45% beat, 25% miss, 30% inline.

What we'll watch on the call

The primary focus for analysts will be the conversion rate of the $553 billion Remaining Performance Obligations (RPO) backlog. Any slowdown in turning this backlog into recognized revenue could trigger concerns regarding customer demand or operational bottlenecks.

Management's commentary on capital allocation is equally critical. Investors need to understand how the company plans to balance its $80 billion-plus infrastructure investment plan with the goal of achieving positive free cash flow by 2029.

- OCI Growth: Can Oracle sustain its high growth rates, previously recorded at 84% year-over-year?

- SaaS Maturity: Are new AI-integrated applications driving cross-selling success within the NetSuite segment?

- Supply Constraints: Are there signs of GPU shortages or data center capacity limits hindering workload delivery?

- Concentration Risk: How does the company manage reliance on key hyperscale customers like OpenAI?

Fintwit's AI verdict

The sentiment surrounding Oracle remains heavily influenced by its aggressive transition into the AI infrastructure space. While the capital expenditure requirements are significant, the market appears to be pricing in a sustained period of high-margin growth for the company's cloud segment.

Investors are weighing the potential for near-term volatility against the long-term prospects of the company's cloud-first strategy. The upcoming earnings call will likely provide the clarity needed to determine if the current valuation accurately reflects the firm's competitive position in the AI ecosystem.