Oracle Corporation (ORCL) Q4 Earnings Preview: What To Watch

Oracle (ORCL) reports fiscal Q4 2026 earnings on June 10. Analysts focus on OCI growth and the conversion of a record $553 billion RPO backlog into revenue.

The setup

Oracle has positioned itself as a critical player in the AI infrastructure race, evidenced by its massive $553 billion Remaining Performance Obligations (RPO) backlog. Investors are closely watching whether this backlog can be converted into recognized revenue at the pace required to justify current valuation multiples.

Management has set an ambitious tone for fiscal year 2027, targeting $90 billion in revenue. This target depends heavily on the sustained growth of Oracle Cloud Infrastructure (OCI) and the successful integration of AI services across the company's SaaS portfolio.

- Capital expenditure reached $39.2 billion in the first nine months of fiscal 2026.

- Total cloud revenue growth is projected at 46% to 50% in USD for Q4.

- Barclays analyst Raimo Lenschow maintains an Overweight rating with a $240 price target.

- Guggenheim analysts reiterate a Buy rating with a $400 price target.

- UBS analysts maintain a bullish stance with a $285 price target.

Consensus numbers

The market expects Oracle to deliver solid results as it navigates the high-intensity capital environment required for AI dominance. Analysts are particularly sensitive to any signs of margin compression resulting from these heavy investments.

Historical performance shows Oracle has frequently outperformed bottom-line estimates over the past two quarters. The following data points outline the current consensus expectations for the upcoming June 10 release.

- EPS Estimate: $1.96

- Revenue Estimate: $19.10 billion

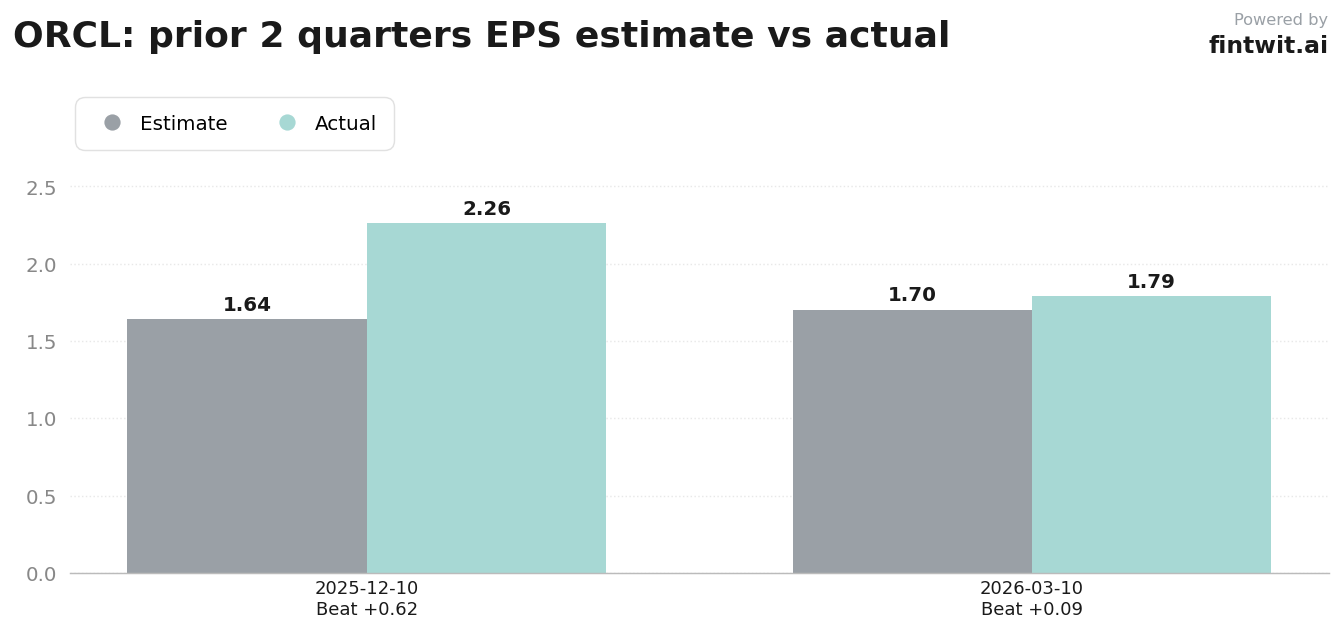

- Q3 2026 EPS: $1.79 (Beat estimate of $1.70)

- Q3 2026 Revenue: $17.19 billion (Beat estimate of $16.93 billion)

- Q2 2026 EPS: $2.26 (Beat estimate of $1.64)

- Q2 2026 Revenue: $16.06 billion (Missed estimate of $16.19 billion)

What we'll watch on the call

The primary narrative for the Q4 call centers on the sustainability of OCI growth rates, which previously hit 84% year-over-year. Investors need confirmation that supply-level constraints are not hindering the deployment of new AI-focused data center capacity.

Management's commentary on free cash flow will be scrutinized against their aggressive capital expenditure plans. The balance between maintaining liquidity and funding long-term infrastructure remains a key risk factor for the stock.

- Can Oracle convert its record $553 billion RPO backlog into recognized revenue at scale?

- Is OCI capacity being built fast enough to meet surging AI demand without compromising margins?

- How will management balance aggressive AI-related capital expenditures with the need to maintain free cash flow?

- Are there any signs of deceleration in cloud infrastructure growth or supply-level constraints?

- Are AI-integrated SaaS offerings, including NetSuite, successfully driving cross-selling and pipeline growth?

Fintwit's AI verdict

The sentiment surrounding Oracle's upcoming report reflects a blend of caution regarding capital intensity and optimism regarding cloud demand. While broader tech sector volatility has impacted valuation multiples, the underlying growth metrics for OCI continue to command significant attention from institutional desks.

The data suggests that the market is pricing in a high probability of a positive surprise, provided the company can demonstrate efficient capital deployment. Investors are weighing the long-term AI narrative against the immediate pressure of high interest rates and sector-wide software valuation adjustments.