Adobe Systems Incorporated (ADBE) Q2 2026 Earnings Preview: What to Watch

Adobe reports Q2 2026 earnings on June 11. Investors are looking for proof of AI monetization and ARR stability amid a 30% year-to-date stock decline.

The setup

Adobe is navigating a difficult transition period where market sentiment has shifted from valuing user engagement to demanding tangible financial results from AI integration. The company has historically outperformed earnings expectations, but the current valuation reflects skepticism regarding competitive pressures from startups and prosumer-focused rivals like Canva.

Management previously provided guidance for Q2 revenue between $6.43 billion and $6.48 billion, with non-GAAP EPS projected at $5.80 to $5.85. Investors are specifically watching for updates to the full-year ARR growth target, which currently sits at 10.2% for fiscal 2026.

- Stifel analyst J. Parker Lane expects an organic revenue beat of approximately 1.5% and modest ARR upside.

- RBC Capital analyst Matthew Swanson remains bullish, citing potential for stabilized quarter-over-quarter ARR.

- Citi analyst Tyler Radke maintains a cautious stance, citing broader market skepticism regarding AI commercialization.

- Macro headwinds include software sector rotation and potential tightening of enterprise software spending budgets.

Consensus numbers

Wall Street consensus estimates for the second quarter of 2026 center on $5.83 in non-GAAP EPS and $6.45 billion in revenue. Adobe has demonstrated a consistent ability to exceed these figures in recent quarters, as shown in the historical performance data.

The market is looking for a clear signal that the Digital Media segment is successfully monetizing its AI-powered toolset. Failure to meet these consensus benchmarks could exacerbate the year-to-date selloff.

- EPS Estimate: $5.83

- Revenue Estimate: $6.45 billion

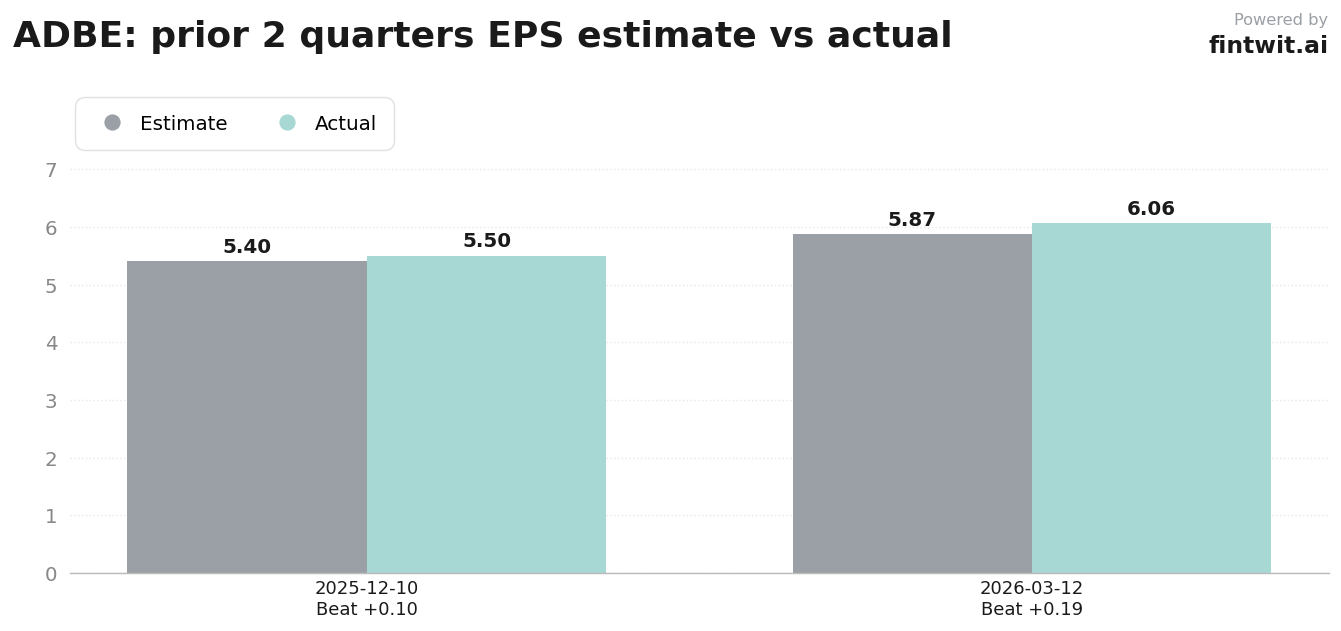

- Q4 2025 Actual EPS: $5.50 (vs $5.40 estimate)

- Q1 2026 Actual EPS: $6.06 (vs $5.87 estimate)

- Q1 2026 Actual Revenue: $6.398 billion (vs $6.276 billion estimate)

What we'll watch on the call

The primary focus for analysts will be the conversion rate of generative AI features into high-margin revenue. Management must clarify whether these tools are driving net-new subscriptions or simply increasing penetration within the existing user base.

The Digital Experience segment remains a critical secondary indicator of enterprise health. Investors need to see if marketing and analytics demand remains resilient against a backdrop of macroeconomic uncertainty.

- Evidence of Firefly and GenStudio driving sustainable, high-margin revenue growth.

- Competitive positioning in the prosumer and SMB segments against rivals like Canva.

- Contribution of the Semrush acquisition to overall ARR and strategic brand visibility.

- Management's plan to balance aggressive AI R&D investment with operating efficiency and margin expansion.

Fintwit's AI verdict

Market participants are currently weighing the company's valuation against the long-term potential of its creative software moat. While the stock has faced significant pressure, the underlying fundamentals of the Creative Cloud franchise remain a point of interest for institutional buyers.

The upcoming report will serve as a litmus test for whether the current price levels represent an entry point or a value trap. The data suggests a high probability of an earnings beat, though the market reaction will depend heavily on forward-looking guidance.