The Cheapest Large Caps Right Now: A P/E Screen

A deep dive into ten large-cap stocks with P/E ratios under 8, separating genuine value from structural decline.

How we screened

We filtered for large-cap equities with market capitalizations exceeding $10 billion and P/E ratios below 8.0. This screen highlights companies currently ignored or punished by the broader market.

The objective is to distinguish between 'unearned' discounts—where sentiment has pushed prices below intrinsic value—and 'earned' discounts, where deteriorating fundamentals justify the low multiple.

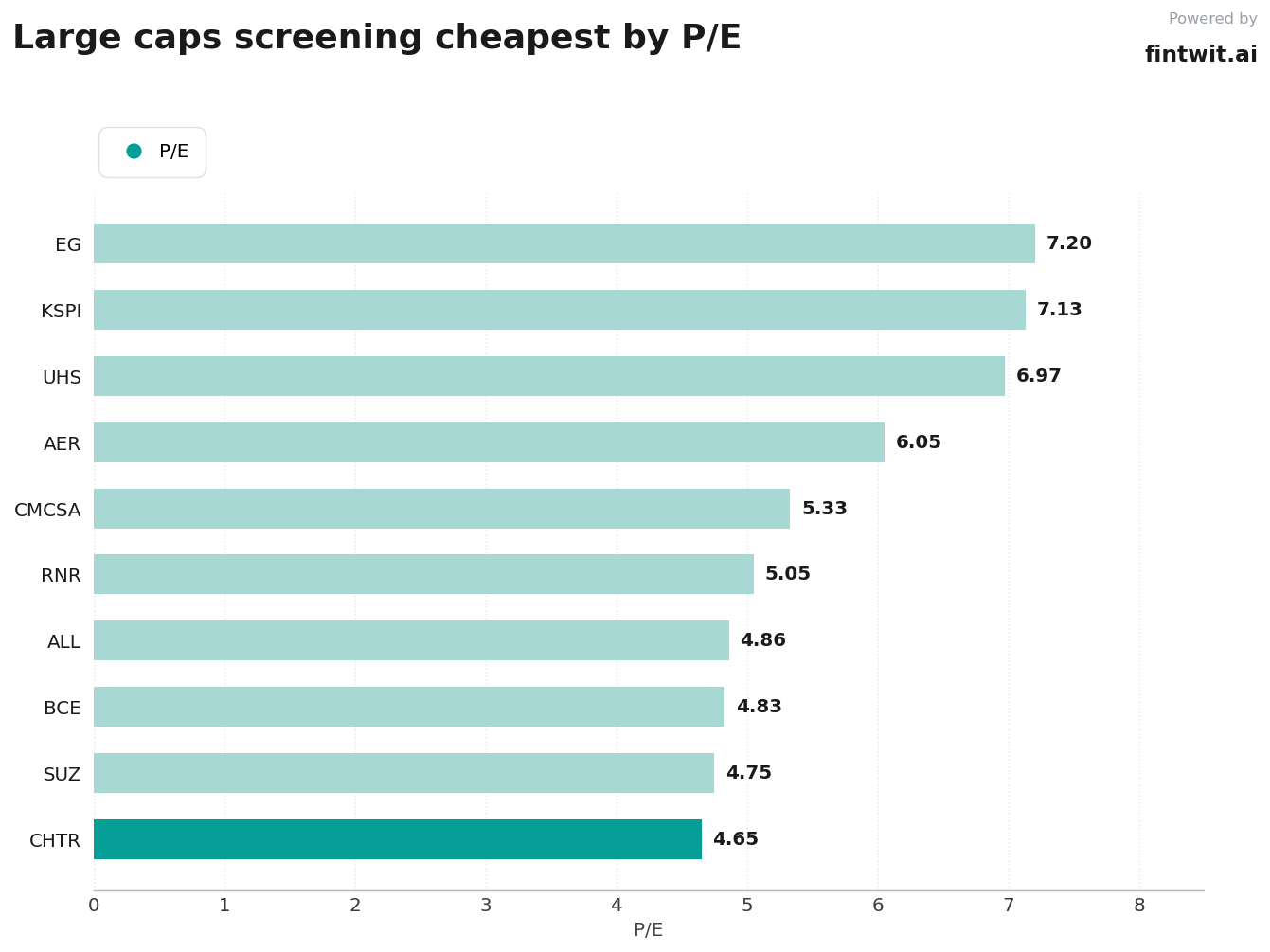

The list

The following tickers represent a cross-section of sectors currently trading at significant discounts to the broader market averages. Investors should note the wide variance in free cash flow yield across these names.

- CHTR (P/E 4.65): Value trap; BofA notes fiscal Q1 was pressured by broadband losses and high capex.

- SUZ (P/E 4.75): Potential opportunity; Seeking Alpha suggests the current price ignores a cyclical recovery in pulp prices.

- BCE (P/E 4.83): Mixed; Public.com highlights regulatory headwinds and high leverage as primary risks to the 9.64% dividend.

- ALL (P/E 4.86): Contrarian buy; StockTok suggests the market is overly pessimistic regarding underwriting margins.

- RNR (P/E 5.05): Value play; Public.com notes strong cash flow metrics despite soft pricing in reinsurance.

- CMCSA (P/E 5.33): Compelling; FAST Graphs argues the market is pricing in a worst-case scenario for legacy cable.

- AER (P/E 6.05): Strong buy; Insider Monkey identifies this as a misunderstood compounder in the aviation cycle.

- UHS (P/E 6.97): Attractive; TD Cowen notes the market reaction to labor cost inflation is overdone.

- KSPI (P/E 7.13): Hold; Seeking Alpha warns that geopolitical and regulatory risks in Kazakhstan justify the discount.

- EG (P/E 7.20): Wait-and-see; Seeking Alpha suggests the discount is justified until underwriting issues are resolved.

Caveats

Low P/E ratios are often a symptom of structural decline rather than a signal of an undervalued asset. Investors must verify if the earnings denominator is sustainable or inflated by one-time gains.

- High debt levels, as seen in CHTR and BCE, can rapidly erode equity value if interest rates remain elevated.

- Catastrophe exposure in insurance names like RNR and EG introduces earnings volatility that can make a low P/E misleading.

- Macroeconomic and regulatory risks, particularly for international firms like KSPI, often act as a permanent ceiling on valuation multiples.

- Free cash flow yield is a more reliable metric than P/E for capital-intensive industries like telecom and paper production.

How to use this screen

Use this list as a starting point for fundamental analysis, not as a buy list. Focus on the 'earned' versus 'unearned' distinction to filter out companies in terminal decline.

Prioritize companies with high free cash flow yields, such as RNR at 33.35% or ALL at 21.61%, which provide a margin of safety through capital return programs or debt reduction.

Monitor the specific catalysts mentioned for each sector to determine if the market's current pessimism is likely to reverse in the coming quarters.