NVIDIA Corporation (NVDA) Q1 Earnings Preview: What to Watch

NVIDIA reports Q1 FY2027 earnings on May 20. Analysts expect $78.4B in revenue as the market monitors Blackwell demand and hyperscaler AI infrastructure spending.

The setup

Wall Street enters this print with high expectations for the AI infrastructure supercycle. Analysts are looking for confirmation that hyperscaler capital expenditure remains in an acceleration phase rather than a plateau.

The primary focus is the transition from Hopper to the Blackwell architecture. Investors need to see that shipment cadence is meeting the aggressive demand signals seen throughout the first quarter of 2026.

- Goldman Sachs analyst James Schneider forecasts a revenue beat of roughly $2 billion above consensus.

- Wedbush analyst Matt Bryson expects guidance to exceed Street projections, citing healthy 2026 infrastructure spend.

- Bank of America maintains a bullish stance with a $320 price target, highlighting data center growth potential.

- Macro headwinds include Federal Reserve interest rate policy and ongoing US-China semiconductor trade restrictions.

Consensus numbers

The market has priced in significant growth, with consensus revenue estimates sitting at $78.42 billion. Non-GAAP EPS expectations are anchored at $1.76 per share.

Previous earnings history shows a consistent pattern of outperformance. NVIDIA has successfully navigated supply chain constraints to beat revenue estimates in consecutive quarters.

- Q1 FY2027 Revenue Estimate: $78.42 billion.

- Q1 FY2027 EPS Estimate: $1.76.

- Data Center Segment Revenue Estimate: ~$73 billion.

- Q2 Revenue Guidance Expectation: $85 billion to $90 billion.

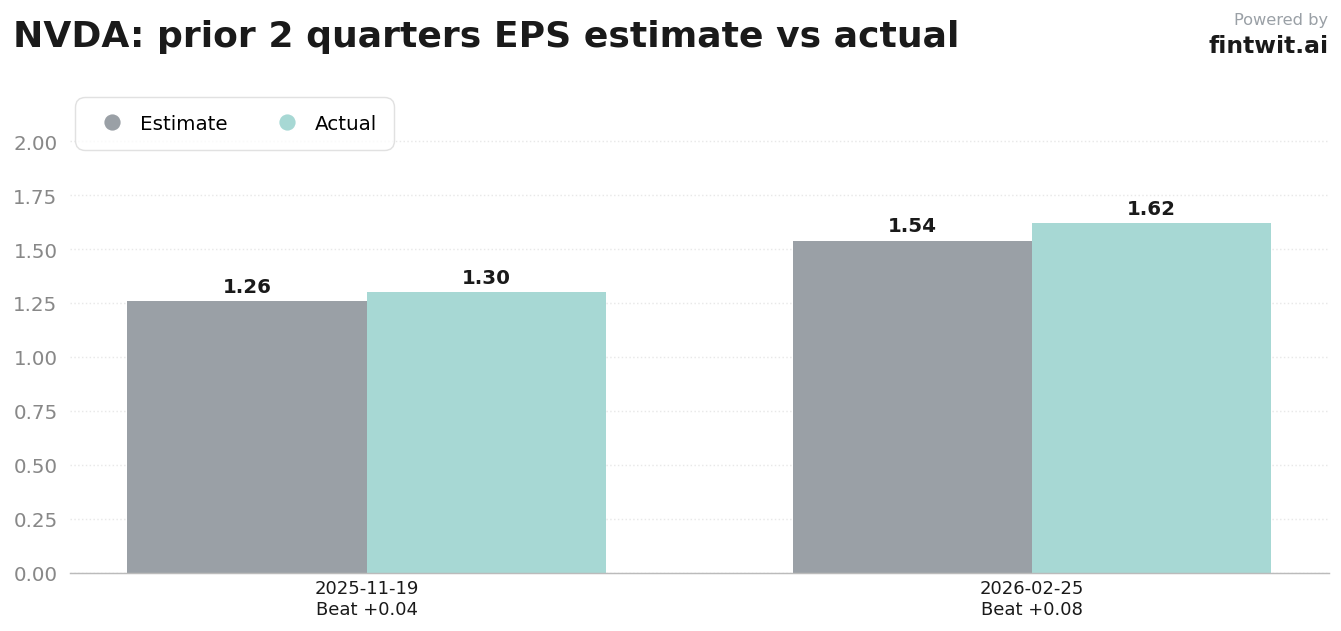

- November 2025 Actual EPS: $1.30 vs $1.26 estimate.

- February 2026 Actual EPS: $1.62 vs $1.54 estimate.

What we'll watch on the call

Management's commentary on the Blackwell-to-Rubin transition will be the most critical data point for margin analysis. Any indication of gross margin compression due to ramp-up costs will be scrutinized by institutional investors.

The shift in demand mix from capital-markets-driven flows to genuine usage-based infrastructure build-out remains a key narrative. Analysts will press for clarity on whether hyperscaler spending is sustainable through the end of the calendar year.

- Blackwell GPU shipment cadence and its impact on gross margins.

- Sustainability of the $700 billion-plus AI capital expenditure cycle.

- Updates on China export policy and potential revenue impact.

- Networking segment performance as a proxy for high-performance computing cluster health.

- Guidance for Q2 revenue to confirm acceleration phase.

Fintwit's AI verdict

The current market positioning suggests that NVIDIA remains the primary beneficiary of the global AI infrastructure build-out. While valuation multiples are elevated, the company's ability to consistently exceed revenue targets provides a floor for institutional support.

Investors are weighing the risks of supply chain bottlenecks against the sheer scale of hyperscaler demand. The upcoming report will serve as a definitive test of whether the current growth trajectory can be sustained into the second half of the year.