NVIDIA Corporation (NVDA) Q1 FY2027 Earnings Preview: What to Watch

NVIDIA enters its Q1 FY2027 print with high expectations. We break down the consensus, key segments, and the critical questions facing the AI giant.

The setup

Wall Street enters the Q1 FY2027 print with high expectations for NVIDIA, focusing on the sustainability of AI infrastructure spending by major hyperscalers. The market is increasingly scrutinizing forward guidance for Q2 and beyond, specifically regarding the Blackwell architecture ramp.

Management is expected to provide Q2 FY2027 revenue guidance, with consensus clustering around $86 billion to $87 billion. Commentary on supply chain constraints and the impact of export restrictions on China will be the primary drivers of the post-earnings stock reaction.

- Wedbush analyst Matt Bryson expects Nvidia to exceed estimates and guide above Street projections, citing healthy 2026 AI infrastructure spend.

- Goldman Sachs analyst James Schneider forecasts a beat of roughly $2 billion above consensus, with Q2 estimates sitting 6% above average Wall Street projections.

- Cantor Fitzgerald analyst David Siffringer maintains a Buy rating with a $350 price target, citing demand that exceeds available supply through 2026 and 2027.

Consensus numbers

The consensus revenue estimate for the quarter stands at $78.42 billion, with non-GAAP EPS projected at $1.76. Investors are scrutinizing gross margins, which are expected to hover near 75%, for signs of pricing power durability.

The 'whisper' number for revenue is frequently cited between $79 billion and $80 billion. Historical performance shows a consistent trend of beating both top and bottom-line estimates.

- Q1 FY2027 Revenue Estimate: $78.42 billion.

- Q1 FY2027 EPS Estimate: $1.76.

- Data Center Segment Revenue Expectation: ~$73 billion.

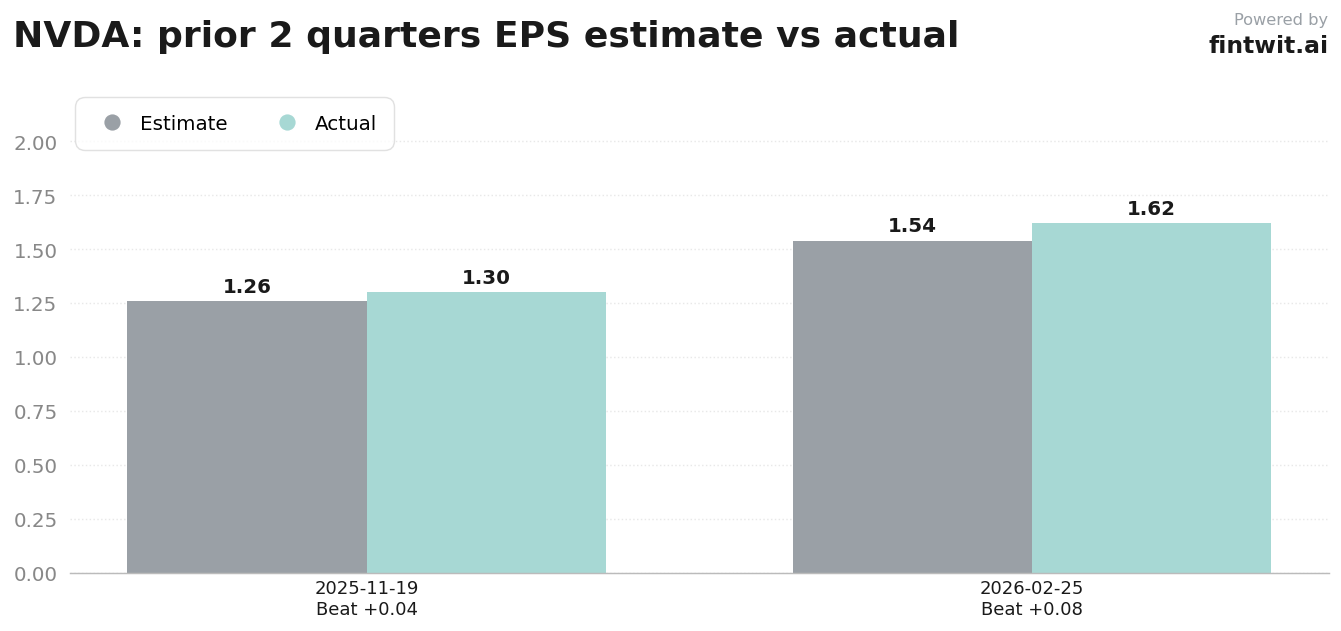

- Q3 FY2026 Actual EPS: $1.30 vs $1.26 estimate.

- Q4 FY2026 Actual EPS: $1.62 vs $1.54 estimate.

What we'll watch on the call

The transition from Hopper to Blackwell architecture remains the most critical variable for near-term margins and shipment cadence. Analysts are looking for confirmation that hyperscalers' increased capex budgets are translating directly into sustained demand for these new GPU platforms.

Networking revenue will serve as a proxy for the complexity of data center deployments. Furthermore, management's update on China-related revenue in light of recent export policy developments will be essential for assessing long-term geographic risk.

- How is the Blackwell-to-Rubin architecture transition impacting near-term margins and shipment cadence?

- Are hyperscalers' increased capex budgets translating directly into sustained demand for Nvidia's latest GPU platforms?

- What is the current status of China-related revenue given recent export policy developments?

- Is there any evidence of competitive pressure from custom silicon or alternative AI chip providers eroding pricing power?

Fintwit's AI verdict

The market sentiment surrounding this print is characterized by a high burden of perfection. While the fundamental demand for compute remains elevated, the stock's valuation requires consistent execution to justify current price levels.

Investors should weigh the potential for a beat against the risk of guidance failing to exceed the most aggressive buy-side expectations. The upcoming report will likely set the tone for the broader semiconductor sector for the remainder of the fiscal year.