Walmart Inc. Common Stock (WMT) Q1 Earnings Preview: What to Watch

Walmart reports Q1 earnings on May 21. Analysts look for resilient grocery demand and e-commerce growth to offset record-low consumer confidence.

The setup

Wall Street views Walmart as a defensive powerhouse capable of capturing market share even as discretionary spending faces significant headwinds. The company's value proposition is currently attracting higher-income households, a trend analysts expect to continue through the first quarter.

Management previously set fiscal year 2027 guidance for EPS between $2.75 and $2.85. Investors are watching for any adjustments to this outlook given the persistent pressure from freight, fuel, and inflationary costs.

- Bank of America analyst Christopher Nardone maintains a Buy rating with a $150 price target, citing the resilience of the core customer base.

- UBS analyst Michael Lasser holds a Buy rating and a $147 price target, projecting U.S. comparable sales growth of approximately 4.5%.

- Bernstein analyst Zhihan Ma raised the price target to $145 from $134, highlighting potential benefits from legislative stimulus for higher-income shoppers.

Consensus numbers

Expectations for the quarter reflect a cautious but optimistic outlook on the retail giant's ability to manage margins. The consensus EPS estimate stands at $0.65, with revenue projected at $174.81 billion.

The company has a history of exceeding expectations, as seen in the previous two quarters where both EPS and revenue surpassed analyst estimates.

- EPS Estimate: $0.65

- Revenue Estimate: $174.81 billion

- U.S. Comparable Sales Expectation: 3.9% to 4.5%

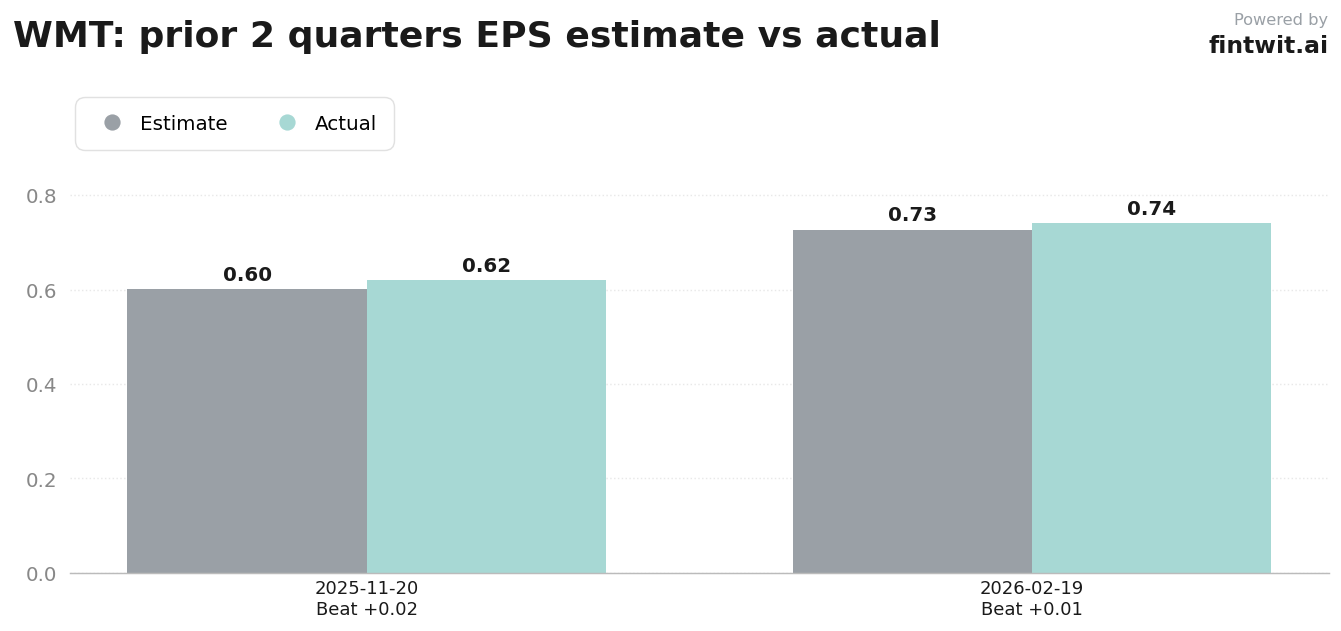

- Q3 FY2026 Actual EPS: $0.62 (vs $0.601 estimate)

- Q4 FY2026 Actual EPS: $0.74 (vs $0.727 estimate)

What we'll watch on the call

The primary focus remains on the company's ability to maintain traffic and volume in the U.S. segment. High-margin growth in advertising and membership services will be critical to offsetting potential retail margin compression.

Management's commentary on the second half of the year will be scrutinized for signs of shifting consumer behavior. The impact of rising fuel costs on operating expenses remains a key risk factor for the upcoming quarter.

- Performance of the Walmart Connect advertising business and its ability to sustain growth above 30%.

- Impact of GLP-1 generic pricing on the Health and Wellness segment margins.

- Management's assessment of how record-low consumer confidence is affecting discretionary category sales.

- Updates on supply chain efficiency and the mitigation of elevated logistics costs.

Fintwit's AI verdict

The data suggests that Walmart is positioned to navigate the current macro environment better than most peers. Analysts are increasingly confident in the company's ability to leverage its scale to maintain profitability despite inflationary pressures.

Investors should pay close attention to the commentary regarding the second half of the year. The current sentiment indicates that the market is pricing in a high probability of a positive surprise.