Mizuho Financial Group (MFG) Q4 Earnings Preview: What to Watch

Mizuho is expected to report Q4 2026 earnings of $0.07 per share. We analyze the impact of BoJ policy and U.S. deal flow on the bank's outlook.

The setup

Mizuho is currently benefiting from the Bank of Japan's monetary policy normalization, which provides a structural tailwind for net interest margins. The bank has demonstrated strong capital efficiency, with nine-month profit performance tracking above original internal forecasts.

Management has signaled confidence in its capital base, supported by active share buyback programs. Investors are closely watching whether the bank can sustain these ROE improvements amidst shifting global interest rate expectations.

- Report Date: May 15, 2026 (Before Market Open).

- Market Capitalization: $92.84 billion.

- Key Macro Factor: Bank of Japan policy normalization and its impact on domestic net interest margins.

- Key Macro Factor: Geopolitical tensions in the Middle East affecting global credit risk.

Consensus numbers

Market consensus from Visible Alpha and S&P Global projects record net income for the fiscal year ended March 31, 2026. Analysts expect continued earnings growth over the next two fiscal years as the bank optimizes its cost structure.

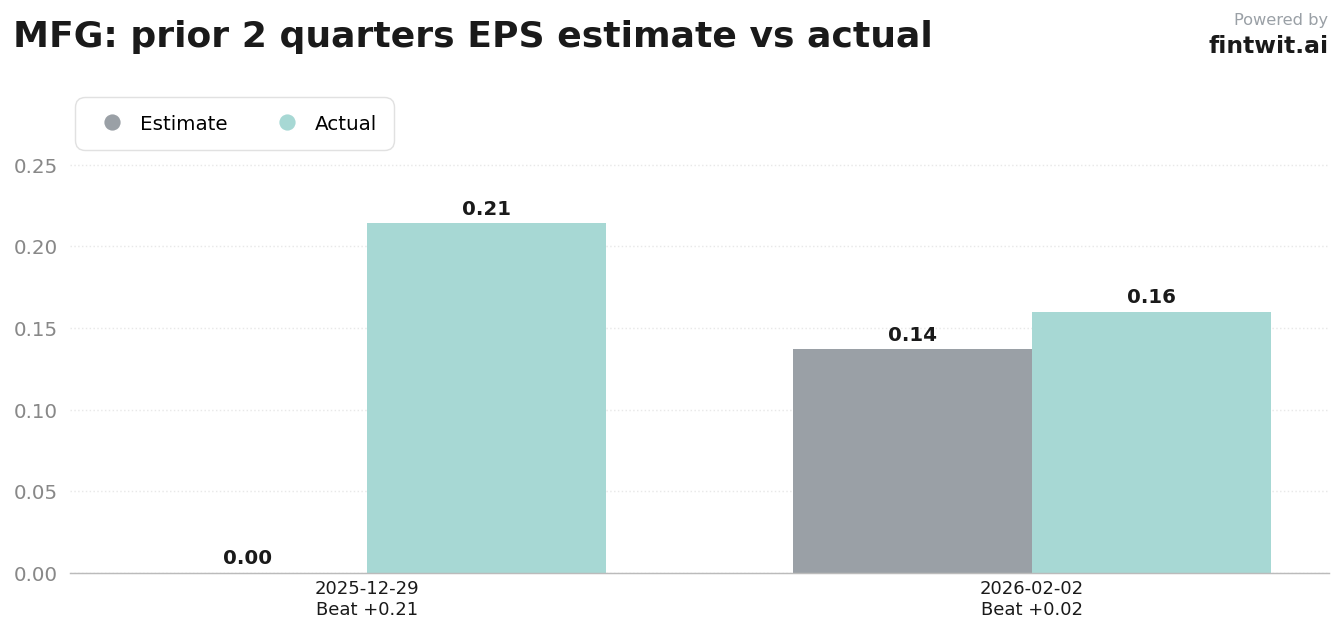

The bank has a history of exceeding expectations, as evidenced by the February 2026 report where actual EPS of $0.16 surpassed the $0.137 estimate.

- EPS Estimate: $0.07.

- Revenue Estimate: $5.43 billion.

- Beat Probability: 60%.

- Miss Probability: 20%.

- Inline Probability: 20%.

- Average Analyst Price Target: ¥7,628.

What we'll watch on the call

Analysts are prioritizing the sustainability of net interest income as JGB yields fluctuate. The integration of the Greenhill acquisition remains a focal point for assessing U.S. investment banking fee growth.

Credit quality is under scrutiny due to potential economic drag from geopolitical tensions. Management's commentary on AI-driven cost efficiencies will be critical for long-term margin expansion targets.

- How is the bank managing duration risk in its fixed-income portfolio amid rising JGB yields?

- What is the outlook for U.S. investment banking fee growth following the Greenhill integration?

- Are there plans to further increase shareholder returns through additional buybacks or dividend hikes?

- How are AI-driven cost savings impacting the long-term cost-to-income ratio?

- Will the bank increase loan loss provisions to account for heightened geopolitical uncertainty?

Fintwit's AI verdict

The quantitative outlook for Mizuho remains constructive, driven by the bank's ability to navigate the shifting Japanese interest rate environment. While global market volatility presents a challenge for investment banking segments, the firm's capital flexibility and commitment to shareholder returns provide a defensive buffer.

Investors should weigh the potential for margin expansion against the risks of increased credit costs. The upcoming earnings call will likely clarify if the bank can maintain its current momentum through the second half of the year.