Mitsubishi UFJ Financial Group Inc ADR (MUFG) Q Earnings Preview: What to Watch

MUFG reports fiscal year results on May 15. We break down the consensus, key segments, and the impact of BoJ policy on the bank's bottom line.

The setup

MUFG is positioned to report record net income for the fiscal year ended March 31, 2026. This performance is largely attributed to the normalization of Bank of Japan monetary policy and expanding net interest margins.

Management has consistently reaffirmed a profit target of approximately 2.1 trillion yen. The bank remains committed to a 12% return on equity and a 40% dividend payout ratio.

- Bank of Japan policy normalization and a potential June rate hike remain the primary macro tailwinds.

- Geopolitical instability in the Middle East poses a risk to credit costs and global energy prices.

- FX volatility continues to impact international earnings and capital ratios.

Consensus numbers

Market expectations for the upcoming report are anchored by strong performance in customer segments and international growth. Analysts are closely watching the trajectory of net interest margins as domestic rates rise.

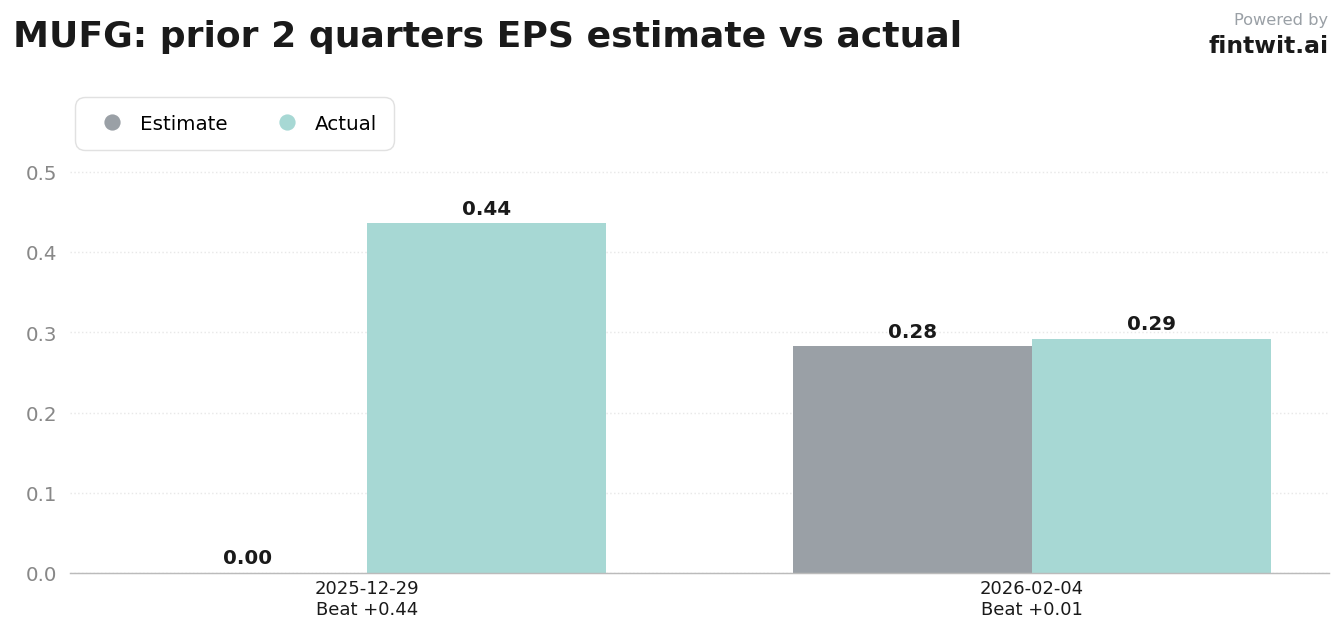

Historical performance shows a 60% probability of an earnings beat based on recent trends.

- EPS Estimate: 0.245

- Revenue Estimate: 8.07 billion

- Target Profit: 2.1 trillion yen

- UBS Price Target: 18.40

- Weiss Ratings Price Target: 18.40

What we'll watch on the call

Management's commentary on the 'capital triangle' will be a focal point for institutional investors. This involves balancing shareholder returns, capital adequacy, and strategic investments.

Credit risk exposure remains a critical line item due to global geopolitical tensions.

- Outlook for net interest margin expansion following the expected June BoJ rate hike.

- Specific updates on equity-method earnings from the Morgan Stanley partnership.

- Assessment of credit risk exposure related to Middle East geopolitical instability.

- Plans for flexible share repurchases in the coming fiscal year.

Fintwit's AI verdict

The quantitative model suggests that the current valuation does not fully account for the sustained margin expansion expected from the Bank of Japan's shift toward higher interest rates. While credit costs are a valid concern, the bank's international diversification provides a buffer that many domestic peers lack.

Investors should monitor the upcoming report for any deviation from the 2.1 trillion yen profit target, as this would signal a shift in the bank's core profitability trajectory. The combination of a strong dividend yield and potential for capital appreciation makes this a compelling case for those looking to gain exposure to the Japanese financial sector.