Kroger Company (KR) Q1 Earnings Preview: What to Watch

Kroger faces a critical Q1 earnings report on June 18. We break down the consensus estimates, key segments, and the risks to the grocery giant's margins.

The setup

Kroger enters the Q1 earnings cycle with a complex narrative centered on balancing price investments with operational efficiency. Persistent inflationary pressures continue to drive consumer trade-down behavior, forcing the company to lean heavily on its private-label portfolio.

Market sentiment remains cautious as the grocery giant navigates an intensifying competitive landscape. Analysts are closely monitoring how the company manages labor costs and technology-driven operating expenses throughout the remainder of the fiscal year.

- Michal Montani of Evercore ISI maintains an Outperform rating with an $83 price target.

- Simeon Gutman at Morgan Stanley holds an Equal-Weight rating with a $73 price target.

- Thomas Palmer of JPMorgan maintains a Neutral rating and lowered his target to $70.

- The current consensus reflects a Moderate Buy outlook across the Street.

Consensus numbers

Wall Street expects Kroger to report earnings per share of $1.58 for the first quarter. Revenue is projected to hit approximately $45.44 billion as the company attempts to sustain volume growth.

The company has demonstrated a consistent ability to outperform expectations in recent quarters. Historical data shows a 65% probability of a beat based on current analyst revisions.

- Consensus EPS estimate: $1.58.

- Consensus revenue estimate: $45.44 billion.

- Digital/E-commerce growth: Analysts are looking for a repeat of the 20% growth seen in the prior quarter.

- Beat probability: 65% vs. 25% miss probability.

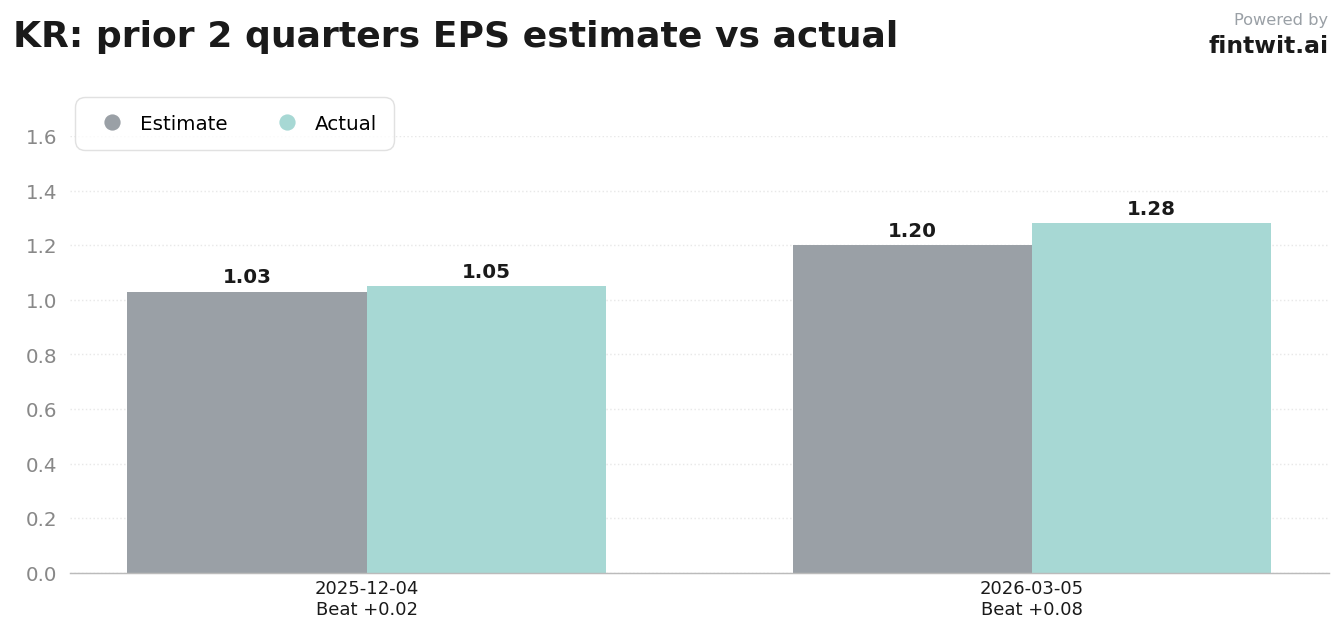

- Q4 2025 actual EPS: $1.05 vs. $1.03 estimate.

- Q1 2026 actual EPS: $1.28 vs. $1.20 estimate.

What we'll watch on the call

Management's commentary on identical sales, excluding fuel, will serve as the primary indicator of core grocery demand. Investors need clarity on whether price-cut initiatives are successfully capturing market share from competitors like Walmart.

The performance of the 'Our Brands' private-label segment is a critical margin-protective lever. Any deceleration in private-label penetration could signal that inflationary headwinds are outpacing the company's ability to retain price-sensitive shoppers.

- Impact of aggressive price-cut initiatives on gross margins.

- Trajectory of consumer traffic and average basket size.

- Timeline and financial impact of store closures for underperforming locations.

- Operating expense profile regarding labor and technology investments.

- Updated guidance on identical sales for the full fiscal year.

Fintwit's AI verdict

The quantitative model suggests that Kroger's recent history of earnings surprises, combined with its strategic focus on private-label growth, creates a compelling risk-reward profile. While competitive pricing pressures remain a significant headwind, the company's ability to maintain operational discipline appears undervalued by the current consensus.

Investors should weigh the potential for a positive surprise against the broader macro uncertainty currently impacting the consumer defensive sector. The upcoming report will likely determine if the stock can break out of its recent trading range.