Accenture plc (ACN) Q3 Earnings Preview: What to Watch

Accenture faces a critical test on June 18 as investors look for signs that AI-driven demand is finally offsetting sluggish discretionary IT spending.

The setup

Accenture management raised its fiscal year 2026 revenue growth guidance to 3% to 5% in local currency, up from the previous 2% to 5% range. This adjustment reflects a cautious optimism despite a broader macro environment characterized by geopolitical uncertainty and high interest rates.

The primary tension for investors remains the gap between AI hype and actual IT budget expansion. While the company has historically outperformed earnings expectations, the current market environment is testing the resilience of its consulting and managed services segments.

- Morgan Stanley analyst James Faucette downgraded ACN, noting that the expected AI budget inflection has not materialized.

- Industry surveys for calendar year 2026 indicate IT services budget growth is hovering at approximately 2% year-over-year.

- Geopolitical and economic volatility continue to impact global supply chains and client decision-making timelines.

Consensus numbers

Wall Street expects a modest year-over-year growth profile for the third quarter. The company has a consistent track record of beating estimates, though the margin of surprise has faced pressure from slowing discretionary spending.

The following figures represent the current consensus expectations for the upcoming report.

- EPS estimate: $3.71

- Revenue estimate: $18.78 billion

- Managed Services growth expectation: 8%

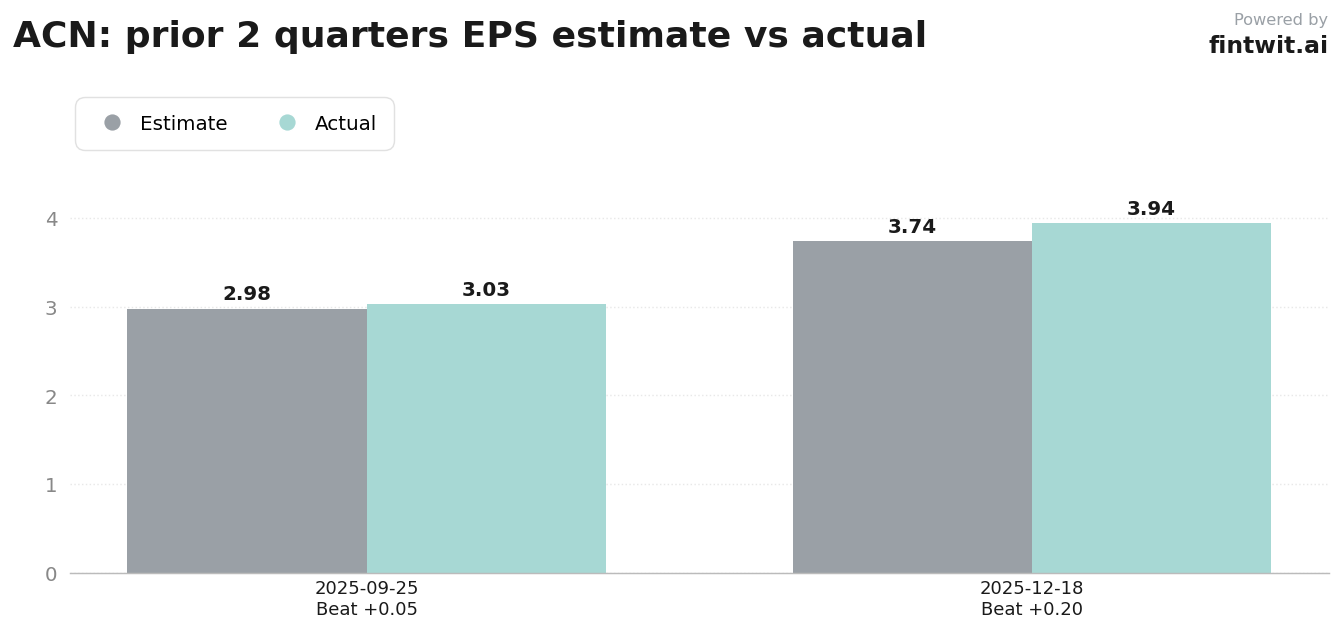

- Q1 2026 actual EPS: $3.03 (vs $2.98 est)

- Q2 2026 actual EPS: $3.94 (vs $3.74 est)

What we'll watch on the call

The earnings call will focus on whether the company can sustain its record-setting pace of large deal bookings. Management commentary on pricing power and the impact of wage inflation on operating margins will be critical for assessing profitability.

Investors are looking for evidence that AI-driven demand is additive rather than a replacement for existing consulting work. The distinction between these two outcomes will likely dictate the stock's reaction to the report.

- Has the expected AI-driven budget inflection materialized in the current quarter?

- Are AI-related projects cannibalizing traditional discretionary IT budgets?

- What is the current status of large deal bookings compared to previous quarters?

- How are pricing pressures and wage inflation impacting current operating margins?

- Do the fiscal year 2026 revenue targets of 3% to 5% remain firm?

Fintwit's AI verdict

The algorithmic sentiment surrounding Accenture remains focused on the company's ability to pivot its massive consulting workforce toward high-demand AI implementation. While the macro environment presents a significant headwind, the firm's scale often provides a buffer that smaller competitors lack.

The upcoming report will serve as a definitive data point for whether the current valuation reflects a realistic growth trajectory or an overly optimistic outlook on enterprise AI adoption.