The Cheapest Large Caps Right Now: A P/E Screen

A deep dive into ten large-cap stocks with low P/E ratios, evaluating whether their current valuations represent value or fundamental decline.

How we screened

We filtered the universe of large-cap equities to identify companies trading at a P/E ratio below 8.0. This screen prioritizes stocks with significant earnings power relative to their current market capitalization.

The selection process focuses on identifying whether low multiples are driven by temporary sentiment shifts or structural deterioration. We categorized each pick based on whether the discount is earned through fundamental weakness or unearned due to market overreaction.

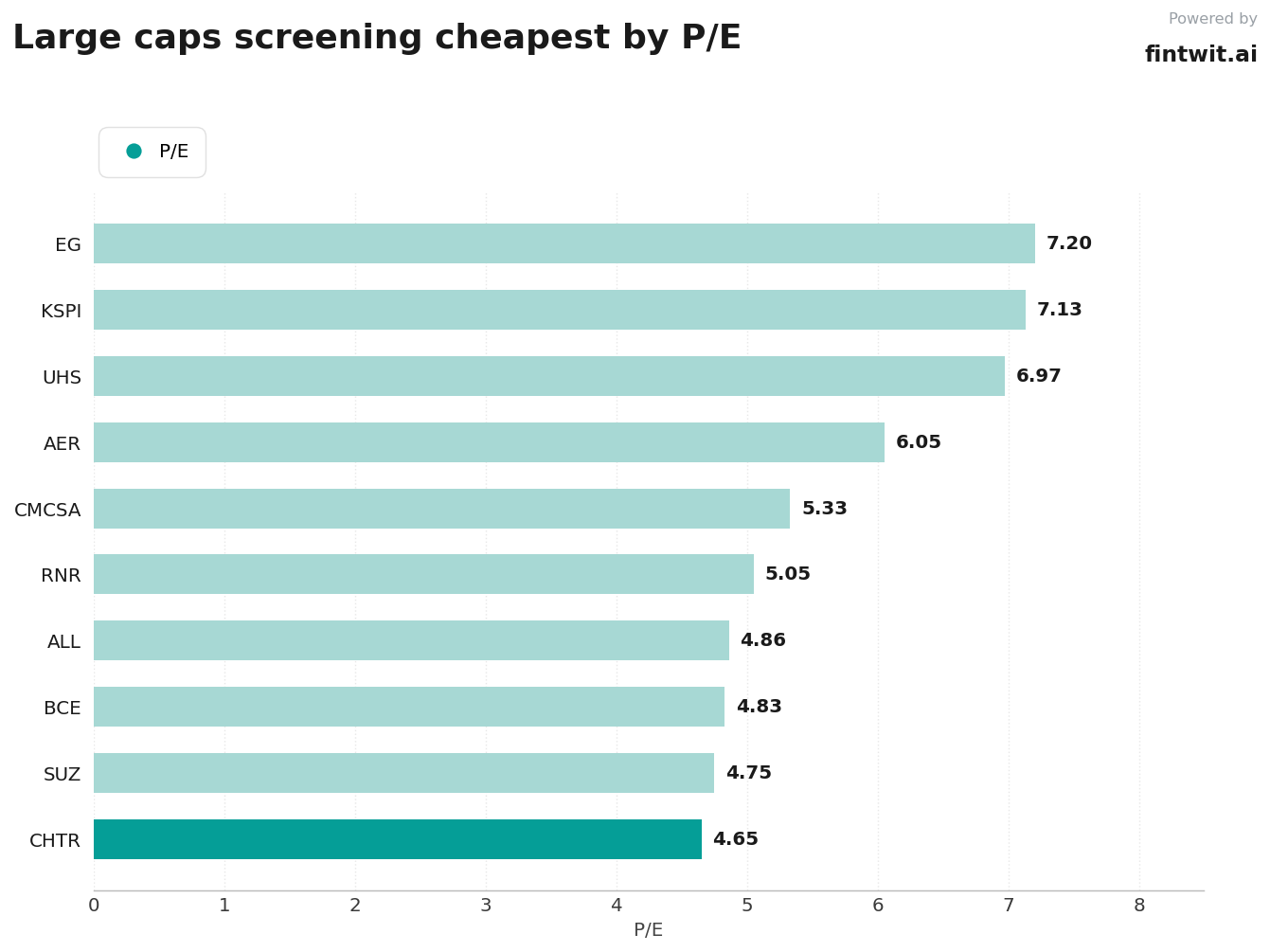

The list

The following companies represent a cross-section of industries currently trading at depressed multiples. Investors should distinguish between companies facing secular decline and those experiencing temporary cyclical headwinds.

- CHTR: P/E 4.65. Why: Broadband losses and high debt. Analyst: Declining EBITDA and increasing debt is not a combination that merits a high valuation multiple.

- SUZ: P/E 4.75. Why: Commodity price volatility. Analyst: Market sentiment often overlooks the long-term cash generation potential of commodity producers during cyclical troughs.

- BCE: P/E 4.83. Why: High debt and sector growth limits. Analyst: Even though BCE looks very cheap, it may not be timely yet, so it's one to watch.

- ALL: P/E 4.86. Why: Underwriting losses in auto insurance. Analyst: The investment thesis for ALL is about future earnings power as rate hikes outpace loss-cost trends.

- RNR: P/E 5.05. Why: Catastrophe loss volatility. Analyst: Insider sentiment is Negative, driven by significant open-market selling from key executives.

- CMCSA: P/E 5.33. Why: Structural broadband losses. Analyst: The core business is in decline as subscribers move to fiber competitors.

- AER: P/E 6.05. Why: Sector rotation away from industrials. Analyst: Pressures stem from investor sentiment and aircraft value concerns, not fundamental weakness.

- UHS: P/E 6.97. Why: Fading ACA subsidies. Analyst: Exchange-related pressures continue to weigh on the stock despite earnings beating estimates.

- KSPI: P/E 7.13. Why: Governance and regulatory risk. Analyst: The low multiple is not a mistake; it prices in regulation and capital allocation uncertainty.

- EG: P/E 7.20. Why: Reinsurance sector slowdown. Analyst: Everest Group sits in the upper tier of global P/C re/insurers, combining robust profitability with conservative leverage.

Caveats

Low P/E ratios are frequently associated with value traps where the underlying business model is permanently impaired. Investors must verify that the earnings supporting these multiples are sustainable rather than one-time accounting gains.

Debt levels play a critical role in valuation. A company with a low P/E but high leverage may face insolvency risks if interest rates remain elevated for an extended period.

- High debt-to-equity ratios can mask the true cost of capital for companies like CHTR and BCE.

- Cyclical commodity producers like SUZ are highly sensitive to global GDP growth and currency fluctuations.

- Regulatory risks in emerging markets like KSPI can lead to permanent capital impairment regardless of the P/E ratio.

- Insurance companies like RNR and ALL are subject to unpredictable catastrophe losses that can wipe out quarterly earnings.

How to use this screen

Use this list as a starting point for fundamental analysis rather than a buy list. Focus on the free cash flow yield to confirm if the reported P/E reflects actual cash generation.

Compare the current P/E against the company's five-year historical average to determine if the discount is an anomaly. If the P/E is low because earnings are expected to collapse, the stock is likely a value trap.