Is Renaissancere Holdings Ltd (RNR) Undervalued? A Valuation Analysis

Renaissancere Holdings Ltd (RNR) trades at a 5.19x P/E ratio. We analyze the reinsurance giant's valuation, peer comparisons, and the bull versus bear case.

The headline number

Renaissancere Holdings Ltd (RNR) maintains a market capitalization of $12.66 billion. The current P/E ratio of 5.19x sits at a notable discount compared to the broader insurance sector.

Analyst sentiment remains split on the stock's fair value. Recent price targets suggest a range of outcomes for the reinsurance firm.

- Simply Wall St estimates a fair value of $328.07 per share.

- Cantor Fitzgerald maintains a neutral view with a $282.00 price target.

- Wells Fargo assigns an equal weight rating with a $281.00 price target.

- The dividend yield currently stands at 0.55%.

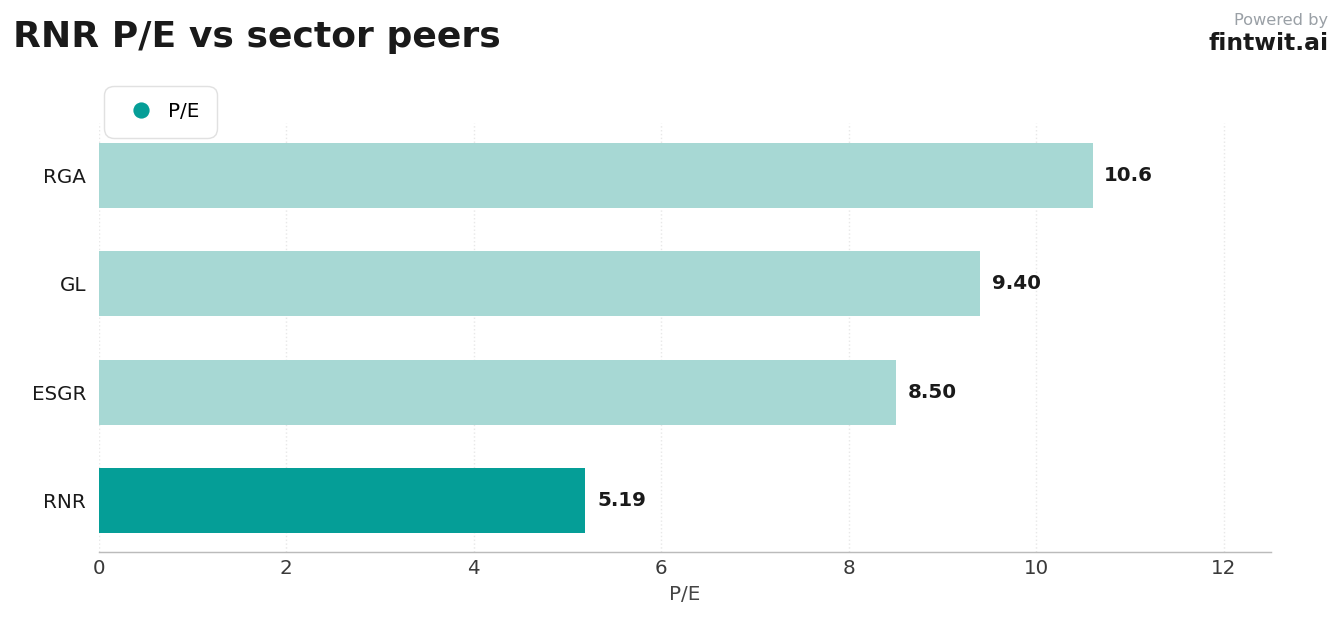

Peer comparison

Renaissancere's valuation multiple is compressed relative to its peers in the insurance and reinsurance space. This discount persists even as the company expands its fee-based income streams.

The following data illustrates the P/E valuation gap between RNR and its industry competitors.

- RNR trades at a 5.19x P/E ratio.

- Reinsurance Group of America (RGA) trades at a 10.6x P/E ratio.

- Enstar Group (ESGR) trades at an 8.5x P/E ratio.

- Globe Life (GL) trades at a 9.4x P/E ratio.

Bull vs bear

The bull case for RNR centers on its diversified business model and consistent capital return programs. Conversely, the bear case highlights potential headwinds in revenue growth and catastrophe exposure.

Investors must weigh the stability of fee income against the cyclical nature of underwriting risks.

- Bull: Diversification across property, casualty, and specialty lines reduces volatility.

- Bull: Strong capital management includes consistent share buybacks and dividend coverage.

- Bull: Growing fee and investment income streams provide long-term earnings support.

- Bear: Forecasts suggest a 6.6% annual revenue decline over the next three years.

- Bear: Projected 20.4% annual earnings decline over the next three years.

- Bear: High sensitivity to large catastrophe losses remains a primary risk factor.

- Bear: Increased competition from alternative capital providers pressures underwriting margins.

Fintwit's AI verdict

The quantitative assessment of RNR suggests that the market may be over-discounting the company's ability to navigate current industry challenges. While the earnings growth projections appear pessimistic, the underlying capital strength and strategic shift toward fee-based revenue provide a potential floor for the valuation.

Market participants are closely watching how the integration of recent acquisitions impacts future margins. The current price level relative to historical multiples suggests an opportunity for those who believe the company can successfully execute its transition strategy.