FuelCell Energy Inc (FCEL) Q2 2026 Earnings Preview: What to Watch

FuelCell Energy faces a critical Q2 2026 earnings report as it attempts to pivot toward AI data center power demand amid persistent profitability concerns.

The setup

FuelCell Energy is shifting its strategic focus toward the AI-driven data center market. Management reports that over 80% of its current sales proposal pipeline is now dedicated to this sector.

The company continues to scale its Torrington manufacturing facility toward a 350 MW capacity. This expansion remains contingent on securing firm customer orders and maintaining liquidity.

Investors remain divided on the company's execution. While some analysts highlight the critical need for on-site power, others point to persistent shareholder dilution and weak generation segment margins.

- Andres Veurink of Seeking Alpha maintains a bearish stance due to ongoing common shareholder dilution.

- Henrik Alex of Seeking Alpha notes that revenue growth has failed to translate into necessary gross margin improvements.

- Dylan Jovine of Behind the Markets remains bullish, citing the company's potential role in the AI infrastructure supercycle.

- The company faces macro headwinds including tightening financing conditions for clean energy projects.

Consensus numbers

Wall Street expects a loss per share of $0.52 for the second quarter of 2026. Revenue estimates are set at $41.64 million.

The company has shown mixed results in recent quarters, with a significant revenue beat in Q1 2026 followed by a miss on EPS expectations in the same period.

The generation segment remains a primary area of concern for analysts, as recent performance showed gross losses that challenge the viability of current project economics.

- EPS Estimate: -$0.52

- Revenue Estimate: $41.64 million

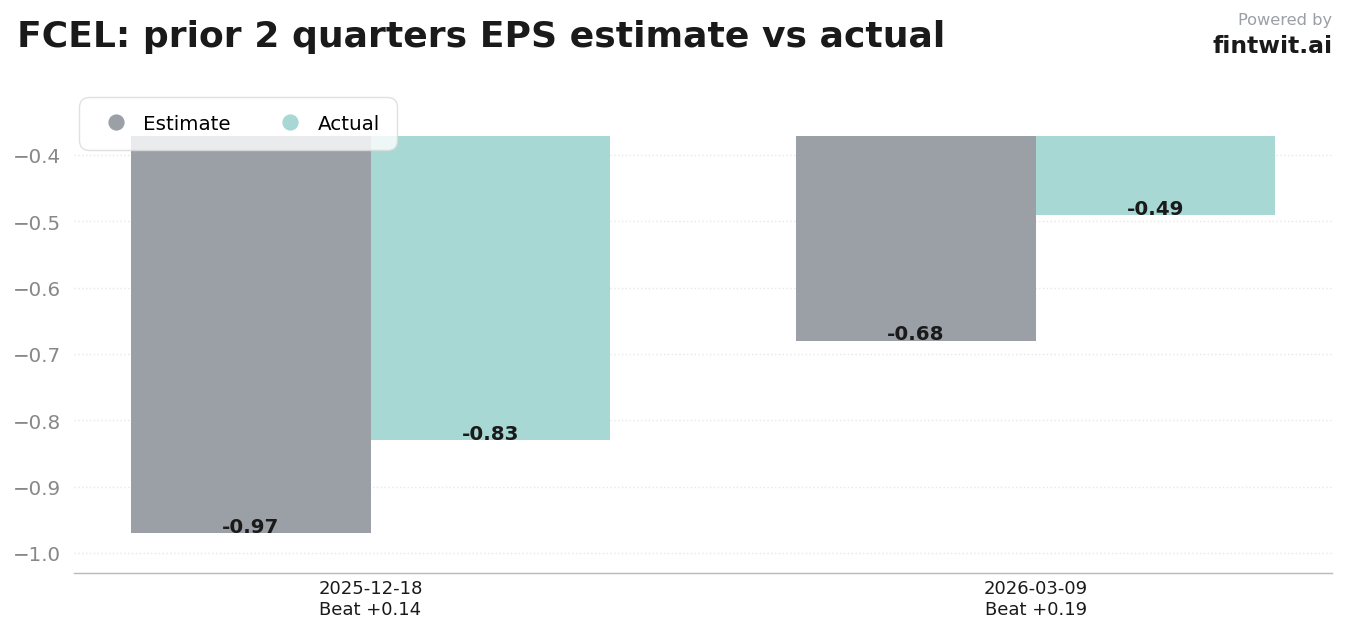

- Q1 2026 EPS: -$0.491 (Estimated: -$0.68)

- Q1 2026 Revenue: $30.53 million (Estimated: $43.33 million)

- Q4 2025 EPS: -$0.83 (Estimated: -$0.97)

- Q4 2025 Revenue: $55.02 million (Estimated: $47.65 million)

What we'll watch on the call

The primary focus for investors will be the conversion of the non-binding SDCL letter of intent into firm purchase commitments.

Management will need to provide a concrete timeline for achieving positive Adjusted EBITDA, especially given the current 40% manufacturing utilization rate.

Liquidity management remains a key theme, with analysts looking for details on how the company plans to fund its capital-intensive growth strategy without further diluting shareholders.

- Status of the SDCL letter of intent conversion.

- Timeline for achieving positive Adjusted EBITDA.

- Impact of current 40% manufacturing utilization on gross margins.

- Management strategy for minimizing equity dilution.

- Trends in project financing costs and their impact on the generation backlog.

Fintwit's AI verdict

The market sentiment surrounding this upcoming release reflects a cautious wait-and-see approach. While the potential for data center integration offers a compelling long-term narrative, the immediate financial metrics suggest significant execution risk remains.

Investors are looking for evidence that the company can move beyond its historical pattern of revenue volatility and margin compression. The upcoming disclosure will likely determine if the current valuation holds or faces further pressure from institutional skepticism.