FuelCell Energy Inc (FCEL) Q2 2026 Earnings Preview: What to Watch

FuelCell Energy (FCEL) reports Q2 2026 earnings on June 8. We analyze the data center pivot, gross margin challenges, and the 1.5 GW project pipeline.

The setup

FuelCell Energy is currently navigating a pivot toward AI-driven data center power solutions. The company aims to leverage its modular power blocks to address grid instability and the surging demand for mission-critical energy.

Despite this strategic shift, the firm continues to grapple with persistent gross losses and negative operating cash flow. Analysts remain skeptical of the transition until the company demonstrates a sustainable path to profitability through manufacturing scale.

The current macro environment presents both tailwinds and headwinds for the business. While grid constraints favor fuel cell adoption, the company's capital-intensive nature leaves it vulnerable to high financing costs.

- The 1.5 GW+ proposal pipeline is the primary focus for institutional investors.

- Management is targeting the Torrington manufacturing facility to reach a 350 MW capacity based on demand milestones.

- Andres Veurink of Seeking Alpha argues that revenue growth without gross margin improvement renders the current bullish thesis unsustainable.

- Henrik Alex of Seeking Alpha highlights persistent shareholder dilution as a major risk factor for long-term holders.

Consensus numbers

Wall Street expects a loss per share of $0.52 for the second quarter of 2026. Revenue is projected to reach $41.64 million.

The company has a mixed track record regarding earnings surprises. Recent history shows a significant variance between estimated and actual results, as seen in the Q1 2026 report where revenue fell short of the $43.33 million estimate.

Simply Wall St analysts maintain a cautious stance, placing a fair value estimate of $8.24 on the stock.

- Q2 2026 EPS Estimate: -$0.52.

- Q2 2026 Revenue Estimate: $41.64 million.

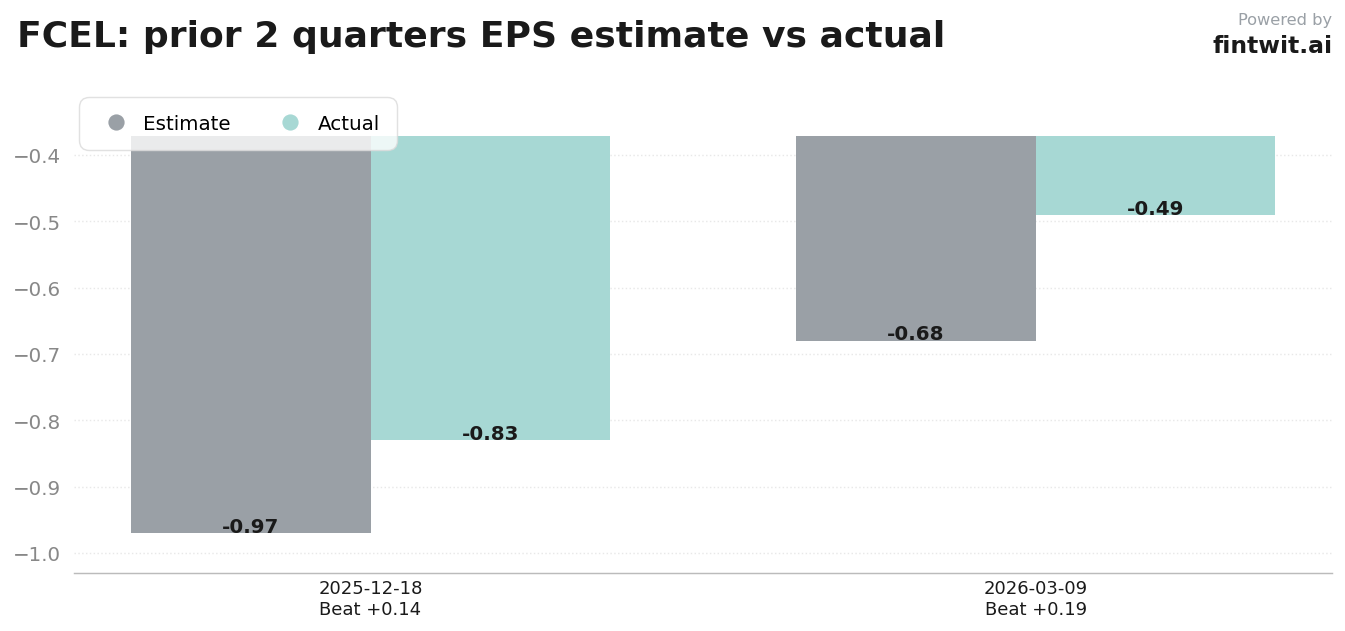

- Q1 2026 Actual EPS: -$0.491 vs -$0.68 estimate.

- Q1 2026 Actual Revenue: $30.53 million vs $43.33 million estimate.

- Q4 2025 Actual EPS: -$0.83 vs -$0.97 estimate.

- Q4 2025 Actual Revenue: $55.02 million vs $47.65 million estimate.

What we'll watch on the call

Management commentary regarding the conversion rate of the 1.5 GW data center pipeline will be the primary driver of post-earnings volatility. Investors need clarity on whether these proposals are moving toward signed, binding agreements.

The Generation segment remains a point of contention due to its inability to generate healthy margins. We are looking for specific updates on cost-cutting measures intended to reverse these gross losses.

Operational efficiency at the Torrington facility is critical for long-term viability. We expect updates on the timeline for reaching the 100 MW run-rate required for better manufacturing leverage.

- Status of the 1.5 GW data center pipeline conversion into binding contracts.

- Timeline for the Torrington facility to achieve 100 MW manufacturing run-rate.

- Specific strategies to address persistent gross losses in the Generation segment.

- Impact of South Korea project milestones on near-term revenue recognition.

- Availability of capital to fund ongoing operations given the current interest rate environment.

Fintwit's AI verdict

The market sentiment surrounding this name remains heavily polarized between those betting on an AI-driven energy renaissance and those focused on the company's history of dilution and cash burn. The upcoming report serves as a critical test for management's ability to execute on its pivot while maintaining a stable balance sheet.

Given the high probability of a miss and the ongoing margin pressures, the current setup suggests a cautious approach until concrete evidence of profitability emerges. Investors should weigh the potential for a breakthrough in data center contracts against the reality of the company's current financial trajectory.