Campbell’s Co (CPB) Q3 Earnings Preview: What to Watch

Campbell’s Co (CPB) faces a challenging Q3 2026 with declining volumes and margin pressure. See our analysis of consensus estimates and key risks.

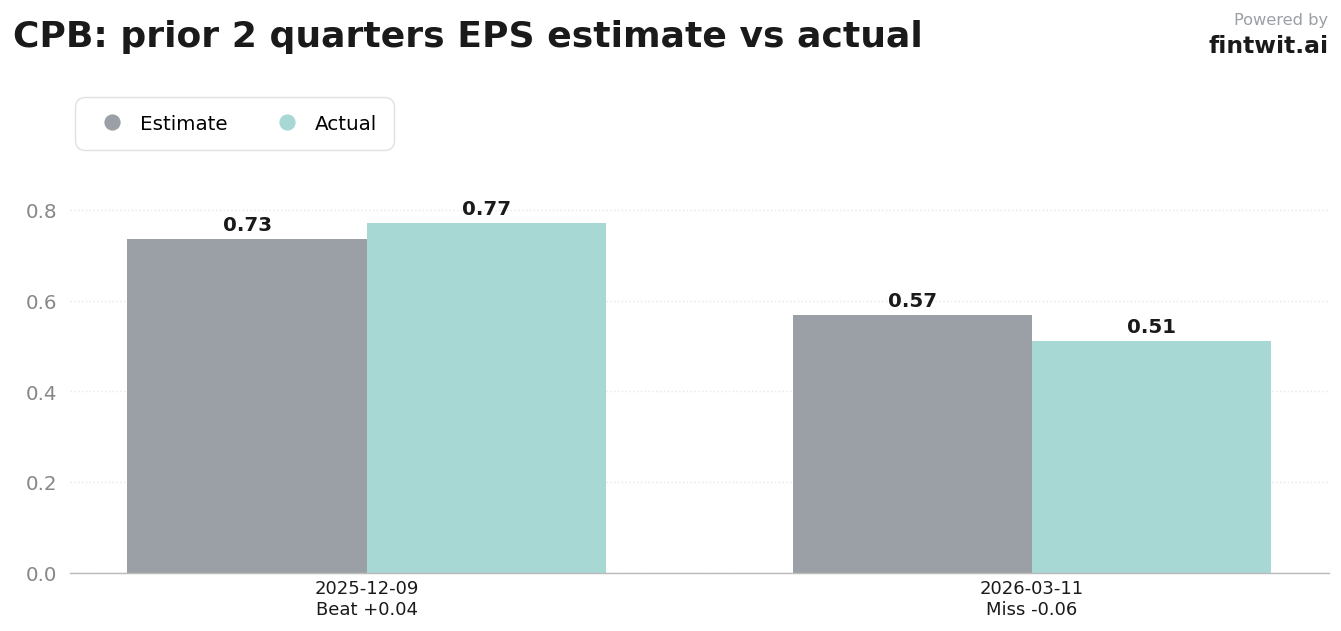

The setup

The company is navigating a difficult macroeconomic environment characterized by persistent inflationary pressures and elevated tariff-related costs for raw materials like steel and aluminum. Consumer behavior has shifted toward private-label alternatives, forcing Campbell’s to defend its market share in a price-sensitive environment.

Management has guided for fiscal year 2026 net sales to range from -2% to 0% compared to the prior year. This cautious outlook reflects ongoing performance headwinds and the difficulty of maintaining growth in a cooling consumer spending climate.

- RBC Capital analyst Nik Modi maintains a Sector Perform rating with a $23.00 price target.

- Alphastreet reports an 18.6% drop in consensus EPS estimates over the last 90 days, signaling potential guidance resets.

- Zacks highlights a lack of the necessary ingredients for an earnings beat, specifically citing margin headwinds.

Consensus numbers

Market expectations for the third quarter reflect significant contraction across key financial metrics. The consensus estimate for EPS stands at $0.48, representing a 34% decrease from the previous year.

Revenue estimates are pegged at $2.38 billion, an 11% decline year-over-year. These figures underscore the structural challenges facing the snacks and meals divisions.

- EPS Estimate: $0.48

- Revenue Estimate: $2.38 billion

- Snacks Segment: Facing severe volume and mix declines due to aggressive competition.

- Meals & Beverages: Monitoring for signs of deterioration in this core, historically resilient division.

- Fresh Bakery: Continued operational and distribution execution challenges remain a primary concern.

- Beat/Miss Probability: 25% chance of a beat, 55% chance of a miss, 20% chance of inline results.

What we'll watch on the call

Investors are focused on whether the company can stabilize its top-line growth through recent acquisitions like Rao's. The effectiveness of cost-saving initiatives in offsetting inflationary pressures will be a critical indicator of margin health.

Management's commentary on the leverage position is essential, particularly the path toward reducing debt below 4x. We are also looking for specific data on how promotional strategies are impacting profitability in the snacks category.

- What is the outlook for volume recovery in the Snacks segment given the ongoing competitive and consumer-trade-down pressures?

- How are management's cost-saving initiatives and promotional strategies impacting margins in the face of persistent inflationary and tariff-related costs?

- Can the company provide an update on the integration of recent acquisitions and their contribution to stabilizing top-line growth?

- What is the current assessment of the company's leverage position and its path toward deleveraging below 4x?

Fintwit's AI verdict

The data suggests that the headwinds facing the company are structural rather than transitory. With consensus estimates trending downward and competitive pressures intensifying, the margin for error in the upcoming report is razor-thin.

Investors should weigh the risks of further guidance revisions against the current valuation. The path forward remains clouded by macroeconomic volatility and shifting consumer preferences.