Credo Technology Group Holding Ltd (CRDO) Q4 Earnings Preview: What to Watch

Credo Technology (CRDO) enters its fiscal Q4 2026 earnings report with strong momentum. We analyze the key metrics and risks ahead of the June 1 release.

The setup

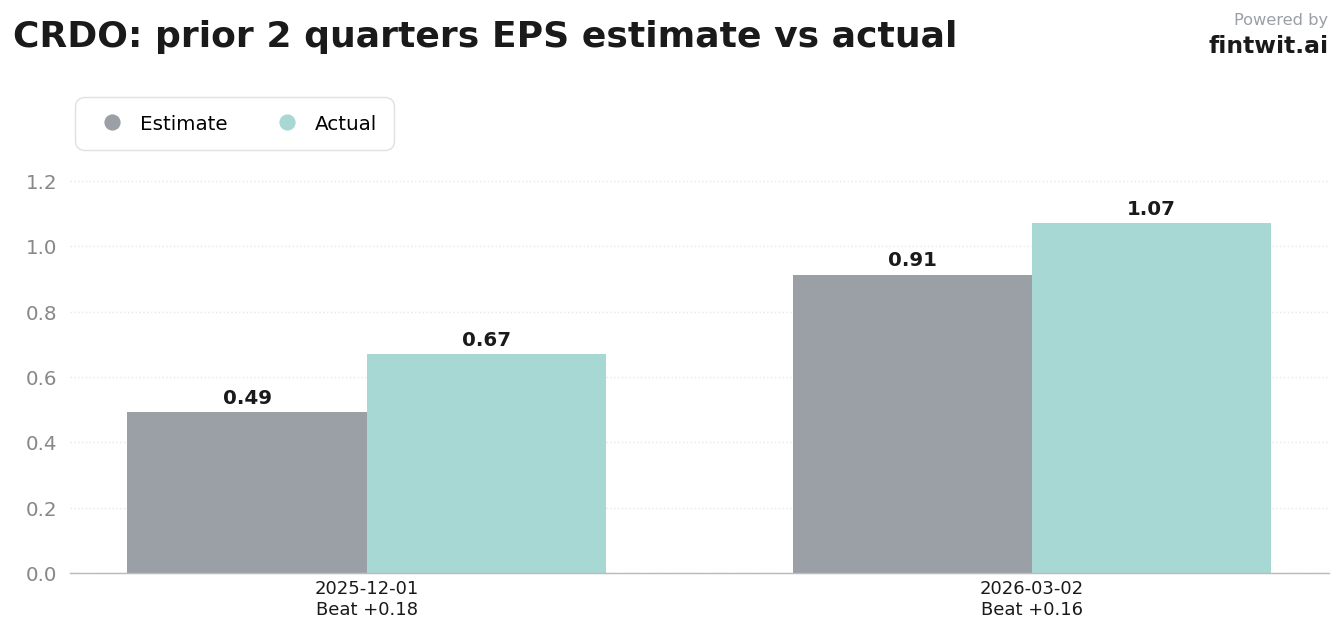

Credo Technology Group (CRDO) is scheduled to report its fiscal Q4 2026 financial results after the market closes on June 1. The company has established a reputation for consistent outperformance, having beaten revenue and earnings expectations in its two most recent quarters.

Investor sentiment remains bifurcated between the company's explosive growth potential in the AI super-cycle and concerns regarding its valuation. Market participants are closely monitoring how the company navigates its high customer concentration, particularly given its reliance on a single major hyperscaler.

- Needham analyst N. Quinn Bolton maintains a bullish stance with a $220.00 price target.

- Goldman Sachs analyst James Schneider holds a more conservative $170.00 price target.

- Jefferies analyst Blayne Curtis cites valuation and volatility risks, setting a $175.00 target.

- Management guided for Q4 revenue between $425 million and $435 million.

Consensus numbers

Wall Street consensus estimates for the fiscal fourth quarter reflect continued scaling of the company's high-speed connectivity solutions. The primary focus remains on whether the company can maintain its revenue trajectory while managing a shift in product mix.

The following figures summarize the market expectations and historical performance context for the upcoming report.

- EPS Estimate: $1.03 per share.

- Revenue Estimate: $431.79 million.

- Q3 2026 actuals: $407.01 million revenue vs $406.17 million estimate.

- Q2 2026 actuals: $268.03 million revenue vs $234.99 million estimate.

- Non-GAAP gross margin guidance: 64% to 66%.

What we'll watch on the call

The earnings call will likely center on the sustainability of gross margins, which management guided to 64-66% for Q4, down from 68.6% in the previous quarter. Investors need to determine if this compression is a temporary result of product mix or a permanent shift due to competitive pricing.

Furthermore, the performance of newer product lines will be scrutinized to assess their contribution to the revenue mix. Management's commentary on hyperscaler capital expenditure trends will be the primary indicator for future demand.

- Management strategy for mitigating customer concentration risk tied to a single hyperscaler.

- Clarity on whether gross margin compression stems from scaling effects or increased competitive pressure from peers like Broadcom and Marvell.

- Updates on the revenue contribution of ZeroFlap optics and OmniConnect product lines.

- Forward-looking commentary on hyperscaler capex cycles for the remainder of the 2026 calendar year.

- Impact of global trade conditions and semiconductor supply chain tariffs on operating costs.

Fintwit's AI verdict

The quantitative model suggests that the current market pricing for CRDO does not fully account for the company's strategic positioning within the AI data center ecosystem. While valuation remains a point of contention among analysts, the underlying growth metrics continue to support a positive outlook for the firm's long-term connectivity roadmap.

Investors should weigh the potential for volatility against the company's historical ability to exceed guidance. The upcoming earnings call will provide the necessary data to confirm if the current growth trajectory remains intact.