Hewlett Packard Enterprise Co (HPE) Q2 2026 Earnings Preview: What to Watch

HPE faces a critical test in Q2 2026 as it balances AI server demand with the integration of Juniper Networks. Here is what to watch.

The setup

HPE is navigating a complex transition as it integrates Juniper Networks to bolster its networking segment. This strategic move is designed to provide a high-margin offset to the inherent volatility of the hardware server market.

Management has set clear expectations for the fiscal year, targeting non-GAAP diluted net EPS between $2.30 and $2.50. Investors are closely monitoring whether the company can maintain this guidance while managing the capital-intensive nature of large-scale AI deployments.

- Truist Financial maintains a buy rating, citing confidence in the company's strategic pivot toward AI.

- Morgan Stanley recently increased its price target, signaling optimism regarding HPE's execution in the infrastructure landscape.

- Citigroup also raised its price target, aligning with broader analyst sentiment that HPE's transformation is gaining traction.

- Power grid capacity constraints remain a physical ceiling for large-scale AI cluster deployments.

- Rising Treasury yields and macroeconomic volatility continue to pressure enterprise capital expenditure budgets.

Consensus numbers

The market consensus for the second quarter of 2026 centers on a revenue figure of $9.78 billion. Analysts expect an EPS of $0.54, which falls within the company's internal guidance range of $0.51 to $0.55.

Historical data shows that HPE has demonstrated a tendency to outperform EPS estimates, though revenue results have been more mixed relative to expectations.

- Q2 2026 EPS estimate: $0.54.

- Q2 2026 revenue estimate: $9.78 billion.

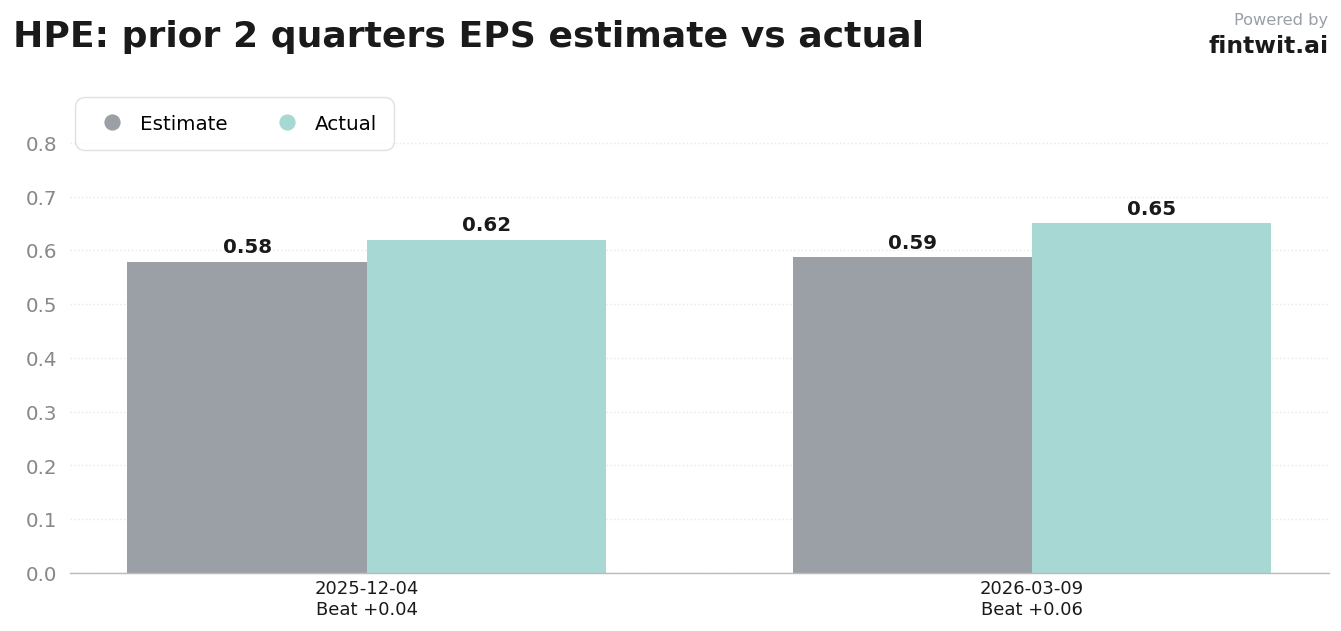

- Q1 2026 actual EPS: $0.65 vs $0.587 estimated.

- Q1 2026 actual revenue: $9.30 billion vs $9.35 billion estimated.

- Q4 2025 actual EPS: $0.62 vs $0.579 estimated.

- Q4 2025 actual revenue: $9.69 billion vs $9.90 billion estimated.

What we'll watch on the call

The primary focus for analysts will be the profitability of the AI server segment. Investors need to see if HPE can scale margins despite the high costs associated with building out large-scale AI infrastructure.

Networking performance is the second critical pillar. The integration of Juniper Networks must prove it can deliver the expected synergies and defend its high-margin profile.

- Can the Networking segment maintain its high-margin profile while scaling Juniper integration?

- How is HPE managing the power grid capacity bottleneck for its AI server customers?

- Are there signs of cooling demand in enterprise AI spending due to elevated energy costs?

- What is the current status and conversion rate of the AI infrastructure backlog?

- How are elevated energy prices impacting the operational costs of AI infrastructure for clients?

Fintwit's AI verdict

The sentiment surrounding HPE has shifted as the company leans into its AI-driven transformation. While hardware cycles remain a concern, the potential for margin expansion through networking software is creating a compelling narrative for institutional investors.

Market participants are weighing the risks of macroeconomic headwinds against the clear demand for AI-ready infrastructure. The upcoming earnings call will likely serve as a definitive data point for the stock's trajectory through the remainder of the year.