Credo Technology Group Holding Ltd (CRDO) Q4 Earnings Preview: What to Watch

Credo Technology Group (CRDO) reports fiscal Q4 2026 earnings on June 1. Analysts expect $1.03 EPS as investors weigh AI infrastructure growth against margins.

The setup

Credo Technology Group (CRDO) has established itself as a pivotal player in the AI infrastructure supply chain through its specialized connectivity solutions. The company's ability to scale its Active Electrical Cable (AEC) business has been the primary engine for recent share price appreciation.

Market participants are currently balancing the company's aggressive growth narrative against concerns regarding margin compression and high valuation multiples. The upcoming report will serve as a litmus test for whether the firm can maintain its competitive moat against larger semiconductor incumbents.

- Needham analyst N. Quinn Bolton maintains a bullish outlook with a $220.00 price target.

- Mizuho analyst Vijay Rakesh holds a positive view on connectivity demand with a $200.00 target.

- Goldman Sachs analyst James Schneider remains cautious, citing valuation concerns with a $170.00 target.

- Management previously guided for Q4 revenue in the range of $425 million to $435 million.

Consensus numbers

Wall Street consensus estimates for the fiscal fourth quarter reflect continued top-line expansion despite the anticipated pressure on gross margins. The company has demonstrated a consistent ability to outperform analyst expectations over the previous two quarters.

Investors are closely monitoring the delta between reported figures and the $431.8 million revenue estimate. Any deviation from the projected $1.03 EPS will likely trigger significant volatility given the stock's current premium valuation.

- Fiscal Q4 2026 EPS estimate: $1.03.

- Fiscal Q4 2026 revenue estimate: $431.79 million.

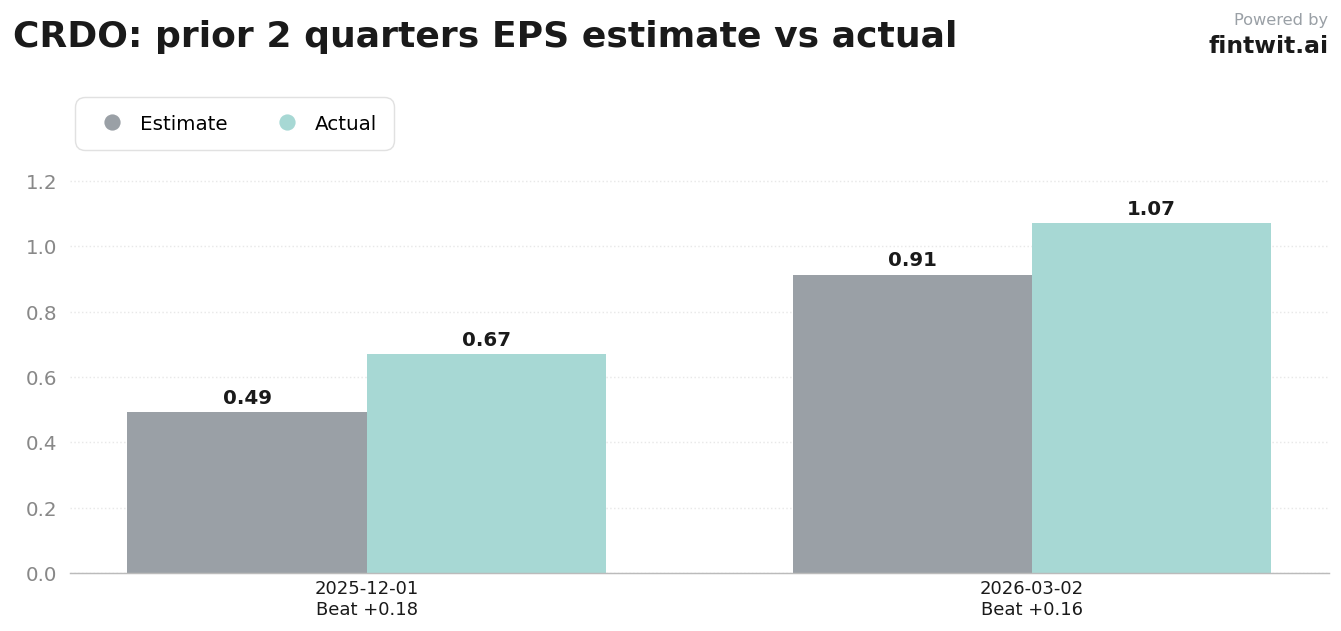

- Q3 2026 performance: $1.07 EPS vs $0.912 estimated; $407.01 million revenue vs $406.17 million estimated.

- Q2 2026 performance: $0.67 EPS vs $0.492 estimated; $268.03 million revenue vs $234.99 million estimated.

- Beat probability: 65% chance of an earnings beat, 15% chance of a miss, and 20% chance of inline results.

What we'll watch on the call

The primary focus for institutional investors will be the sustainability of gross margins. Management previously guided for compression to the 64-66% range, and the market needs clarity on whether this is a structural shift or a temporary product mix issue.

Operational updates regarding the two new hyperscale customers are essential for validating the fiscal 2026 growth trajectory. Any commentary suggesting a delay in these deployments could weigh heavily on the stock's near-term performance.

- Pricing dynamics in the AEC and optical DSP markets relative to competitors like Broadcom and Marvell.

- Progress on the ramp-up of two new hyperscale customers contributing in the second half of fiscal 2026.

- Gross margin outlook beyond Q4 and the impact of product scaling on profitability.

- Inventory level analysis to determine if current stockpiles represent strategic positioning or softening demand.

- Impact of potential cooling in hyperscaler capital expenditure on future growth guidance.

Fintwit's AI verdict

The quantitative model suggests that the market may be underestimating the long-term tailwinds provided by Credo's proprietary connectivity technology. While valuation remains a valid concern for some analysts, the underlying fundamental momentum in the data-center segment appears to remain intact.

Investors should prepare for potential price swings following the release, as the market digests the margin guidance against the backdrop of broader semiconductor cyclicality. The data points toward a specific outlook for the coming fiscal year.